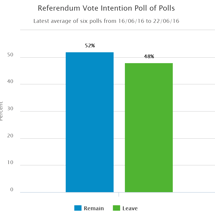

Soros: Europe will now “disintegrate”

From George Soros at Project Syndicate: Britain, I believe, had the best of all possible deals with the European Union, being a member of the common market without belonging to the euro and having secured a number of other opt-outs from EU rules.