On perhaps the most important metric – inflation – we are almost back to where we started, with core near last year’s low of 0.6 percent. Looking through the lens of the inflation mandate, sequential (month-over-month) inflation needs to triple from its pace over the past year for the ECB to meet its already low forecast for core of 1.3 percent in 2016 (Exhibit 1). Put another way, our European economics team forecasts core at just 0.9 percent this year. There is therefore little doubt in our minds that the ECB is missing its mandate and – given the miss on core – that this is not just a story about lower oil prices. Instead, the Phillips curve in the Euro zone may have shifted down, which would explain why core has failed to pick up even as the unemployment gap has closed (Exhibit 2). The fact that this downshift originates in southern Europe, as we have shown, suggests that structural reforms are pushing wages and prices lower, giving a deflationary bias to the periphery, such that Euro zone inflation is now lower ceteris paribus. If this is true, low inflation is a more serious problem than the ECB believes and requires forceful action. In this FX Views, we lay out scenarios for EUR/$ for different outcomes on Thursday. Above all, after a year of mixed messages, the ECB needs to signal that it is serious about pursuing its inflation mandate, including via a stepped up pace of monthly QE purchases.

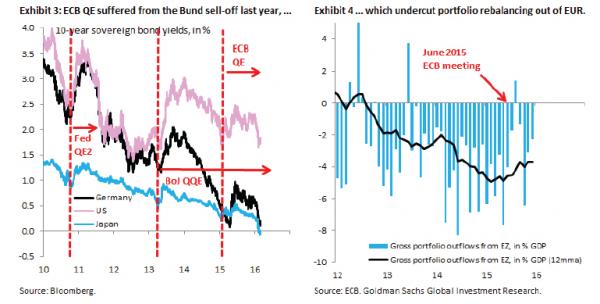

There is little doubt in our minds that the ECB wants to surprise this week, not just because of the inflation picture, but also because it disappointed in December, inadvertently tightening financial conditions materially. The question is whether it will choose to do that on the deposit rate and/or sovereign bond buying. From the perspective of EUR/$, we think it is helpful to go back to first principles. The main goal of any QE program is to encourage a portfolio shift from the safe haven asset – Bunds in the Euro zone – to risky assets, including foreign currencies. The sharp Bund sell-off a year ago, not to mention the volatility since then (Exhibit 3), have impaired the functioning of ECB QE, as can be seen from the pull-back in residents’ portfolio outflows following President Draghi’s comment that “markets should get used to periods of higher volatility” at the June press conference (Exhibit 4). Our first preference is therefore for the ECB to simply stabilize Bund yields at a relatively low level, similar to what the BoJ has done since the start of QQE. This is the most powerful option for Euro down and would require the Bundesbank to adjust the maturity of its Bund purchases to market conditions. A shift from Bunds to more periphery debt, for example by relaxing the capital key, is next up in our list of preferred measures,where our rule of thumb is that an EUR 100 bn surprise is worth one big figure downside in EUR/$. Another cut in the deposit rate is our least preferred option, because we see the effect from negative interest rates as relatively limited. We think a 10 bps surprise is worth two big figures downside in EUR/$. Given how much is priced and the negative perception of tiering, this is the least powerful option.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.