As the ECB has increasingly turned to alternative measures, we have outlined how confidence amongst borrowers and lenders and credit activity have responded. The key takeout has been that, while confidence amongst households has improved materially leading to stronger consumer spending, the impact on non-financial corporates had been much more modest, particularly with respect to their appetite for credit. Following the ECB’s April meeting and the release of the latest ECB bank lending survey, now is an opportune time to reassess progress on each of these fronts.

Starting with the consumer, although confidence in the economy and family finances remains above average, recent months have seen late-2015’s exuberance give way. The consumer sentiment detail suggests much of this loss of momentum has been due to weaker expectations surrounding the economy and labour market. To the extent that this survey also continues to point to a need for households to dissave to fund consumption, it is unsurprising that such a quick reversal in confidence could take hold.

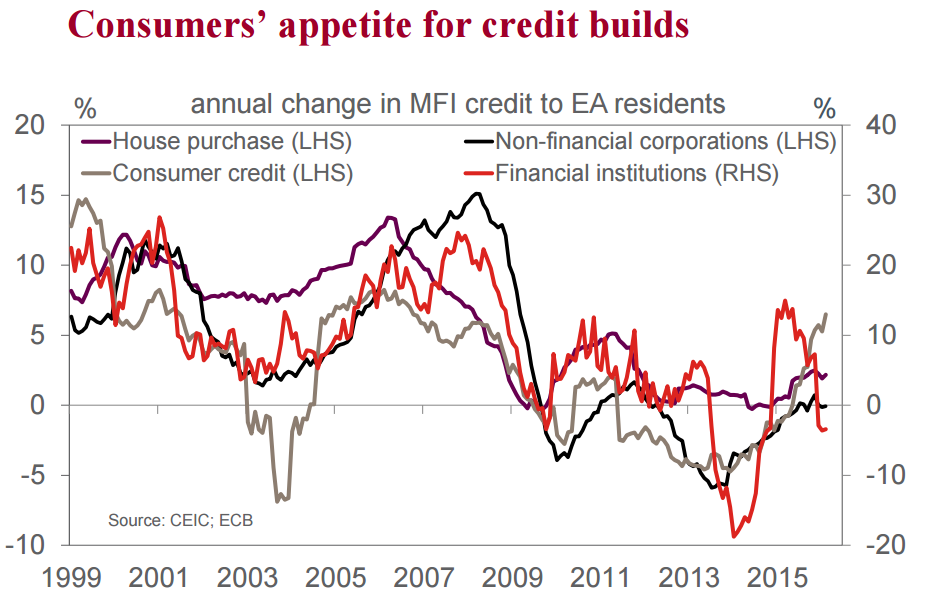

From the ECB’s credit data, we see that weaker confidence has impacted mortgage demand, but (as yet) not consumer credit. This is to be expected given the ECB’s alternative policy measures have been focused on consumer credit not mortgages.

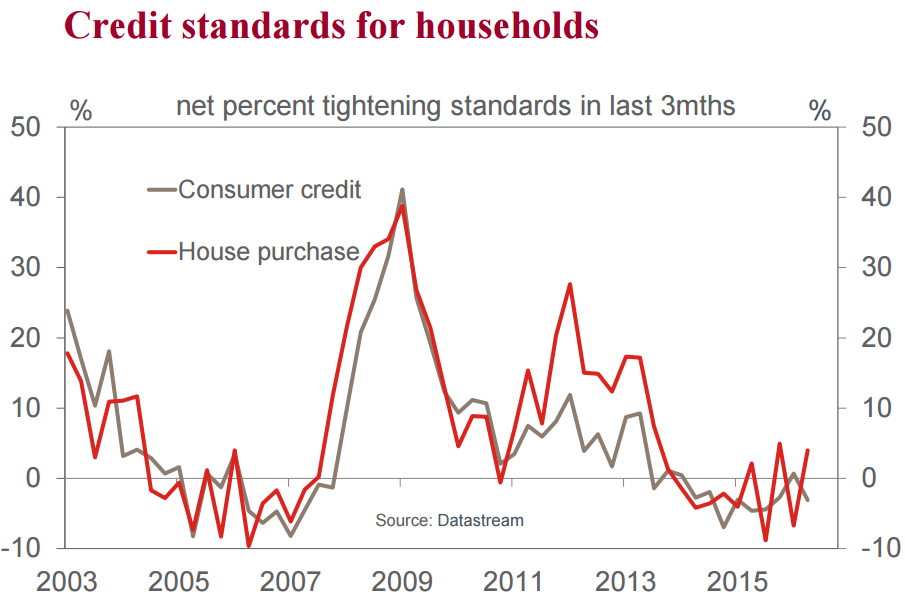

While the ECB’s actions have reduced the cost of consumer credit materially, from the ECB’s own bank lending survey it is clear they have done little for the terms and conditions of those loans, which have only improved at the margin. For mortgages, credit standards have actually been tightened in the current quarter and, at best, can only be regarded as little changed over the past year. With respect to the tighter mortgage terms, loan-to-valuation ratios and a loan’s duration look to be the current focus of European banks.

Herein then is evidence of the ECB’s short-to-medium term liquidity operations being insufficient to stoke greater risk appetite amongst banks toward households. This is particularly true with respect to long-term obligations.

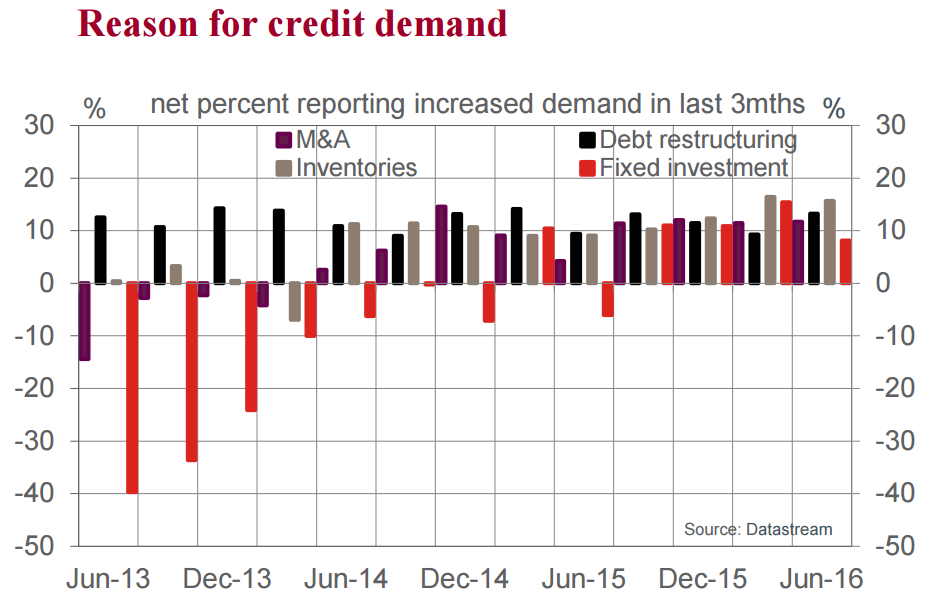

Turning to non-financial corporates, a similar theme is apparent. According to the ECB’s survey: we have seen a material increase in the demand for credit from this sector; and pricing for an ‘average’ loan has improved markedly (note, for riskier loans, there has been little change). But the purpose of borrowing continues to veer towards short-term use (i.e. inventories); the rolling over of existing debt facilities; and M&A activity. Indeed, after a prolonged drought, marginal borrowing to fund fixed investment looks to already be loosing momentum (after just four successive gains).

Ad hoc questions asked by the ECB as part of the lending survey emphasise that, despite having experienced a material (and continuing) improvement in market conditions and liquidity, there is little appetite to meaningfully expand total assets.

In the six months since April, the net percentage of banks who have increased their total assets has fallen from 10% to 5%. The coming six months is also expected to show little improvement (+7%). Further, asked about their use of the liquidity afforded by the Asset Purchase Program (APP), more than 80% of responding banks reported that the additional liquidity had “basically no impact” on granting loans. The full breakdown includes: nonfinancial corporates (80%); households for house purchase (85%); and households for consumer purchase (87%). Similar outcomes were reported for the impact of APP liquidity on credit standards as well as terms and conditions: almost 100% reported no change in standards; around 90% said the same for loan terms.

Evinced by the lending survey, it is clear that profitability is a major concern for the region’s banks. Negative interest rates and the APP are both reported to have had an adverse impact on profitability, reducing net interest margins and available capital gains. Combined with the risk posed by lingering uncertainties, deteriorating expected return on any increase in net exposure is a good reason to not expand total assets.

Given this environment, it is difficult to see the ECB’s policies acting as a catalyst for stronger aggregate growth and inflation as they intend. Instead, absent an exogenous shock to demand (fiscal and/ or international) we are likely to see continued disappointment on both fronts. Such an outturn would give cause for further intervention by the ECB – although its effectiveness would also be doubtful. Globally, alternative measures have proven effective at stabilising markets and real activity (stopping things from getting worse); but by themselves they have little capacity to spur end demand in a leveraged, low income growth world.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.