Like most boys, my three-year old loves see-saws. From his perspective, it has two steady states. ‘Down’ when he sits on it – and ‘Up’ when daddy sits at the other end. The transition between the two states is all too swift. And unfortunately, every time we end up in an equilibrium, it’s pretty hard to shift – at least until he’s eaten a lot more broccoli (or so I tell him).

The situation in markets is not dissimilar – albeit rather more joyless. Faced with disinflation, lower growth prospects, record high levels of indebtedness, low profit growth, and structural policy paralysis there is a fundamental equilibrium which is distinctly ‘down’. Yet the tightening in financial conditions and the hysteresis effects such an outcome would bring are the last things policymakers already faced with the breakdown of faith in the centre-driven – or call it ‘establishment’ – politics want to contemplate here and now. And so central banks are weighing more heavily on markets than ever, keeping valuations on most assets firmly ‘up’. Past attempts at getting off have led to precipitous descents in those valuations every time. So there we hang.

What’s new about the current situation is that the question has morphed from previous concerns about one central bank or another being about to bail, to one of whether they really have enough mass to offset the weight of negative fundamental impulses.

Faced with €400-500mn of ECB buying per day, the immediate answer in credit in the aftermath of ‘Brexit’ was a resounding ‘yes, they do’. But some other asset classes seem to be drawing a different conclusion.

…the two things that worry us at the moment are falling yields and European banks – and, indeed, their interaction. The negative signal that falling yields and inflation expectations send for credit is something that we’ve flagged repeatedly over the last month.

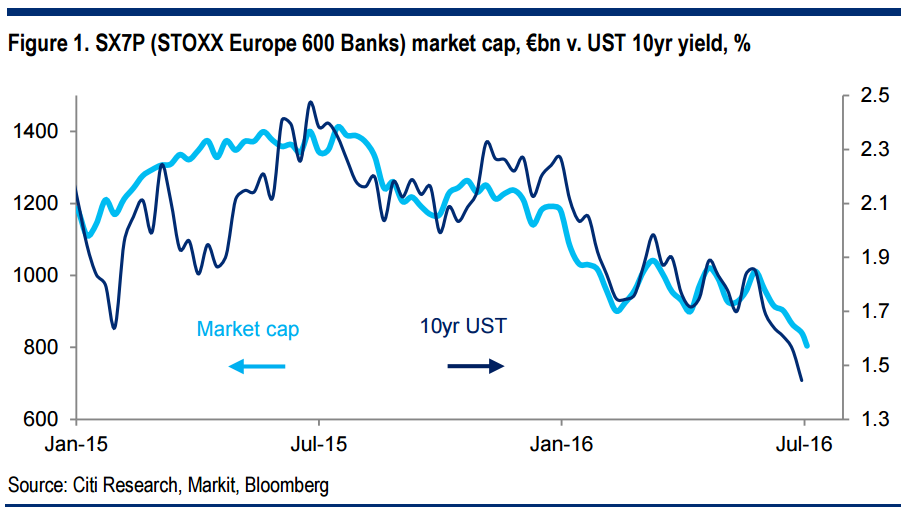

But this week we want to focus on the ongoing de-rating of European bank equities, which for a growing number of banks is greatly inhibiting the ability to raise new capital. Over the last year, the market cap of the SX7P (banks in STOXX Europe 600) is down by more than 40%, in what has become an almost perfectly correlated move with falling yields (Figure 1). Within that, of the 48 banks in the index, 25 have seen their market cap more than halve.

Granted, valuations remain considerably better than at the depths of the GFC and the sovereign crisis in aggregate (Figure 2). However, that masks considerable divergence. Nearly half the banks in the index have a market cap that is at or below the level from June 2012 – just before Draghi promised the ECB would ‘do whatever it takes’. Indeed, on a price-to-book basis the whole index is now right back to the GFC and sovereign crisis lows.

…the lower the equity valuation, the greater the proportion of any capital shortfall that will have to be filled by means other than the equity market. And that surely raises the probability that policymakers, willingly or having run out of other options, end up writing down or converting the debt. Although this might be more of an issue for mid-tier banks than the larger banks that make up the bulk of the indices, the precedent it would set should surely be reflected in risk premia.

But there is a much broader point, which surely impinges on non-financial credit too. Capital-constrained banks just don’t lend very much. The ECB can inject all the liquidity it wants, but if the cost of equity is higher than the return on equity then it is more efficient for banks to reduce balance sheet than to provide new lending.

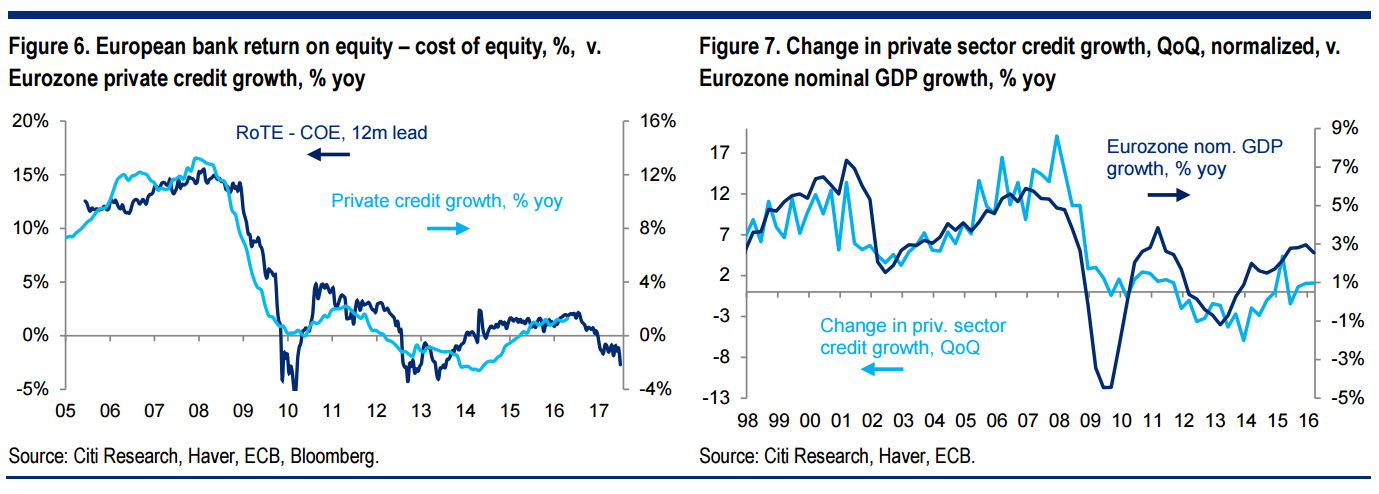

Figure 6 shows very clearly how strong the link is between the excess return on equity and private sector credit growth in the Eurozone with a lead of one year. Currently, the high cost of equity suggests credit growth will turn negative over the coming months. Private credit growth, or rather the incremental change in it, has a very strong link with broader economic growth (Figure 7).

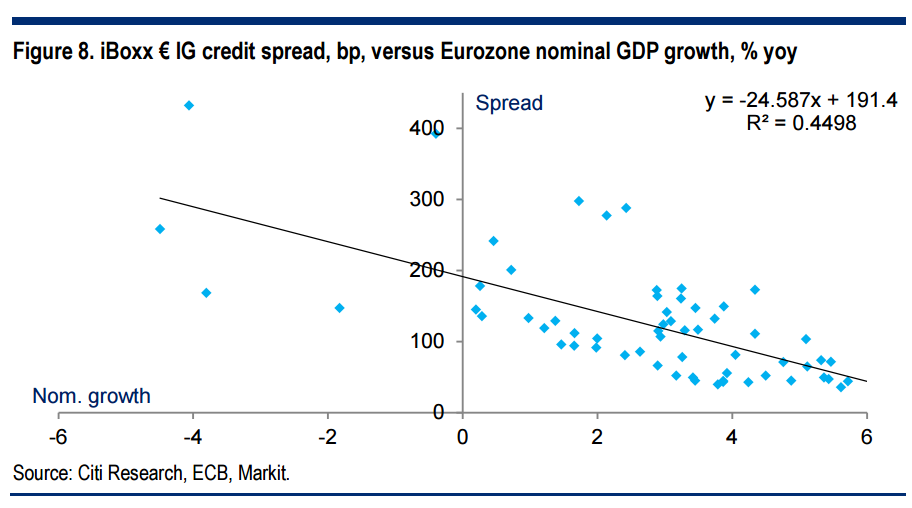

And to complete the loop back to credit, spreads in € IG are normally very well correlated with nominal GDP growth in the Eurozone (Figure 8).

So basically, when the market doesn’t believe in the ability of banks to deliver adequate returns it has a direct economic impact over time. That, in turn, should impact credit spreads down the road.

As long as the ECB is sitting so firmly on credit, you could choose to ignore that. But as we have pointed out previously, the experience last year from covered bonds strongly suggests that if the broader backdrop becomes negative, then it can outweigh ECB purchases and lead to wider spreads.

What’s apparent to us is that the tension between the technical created by the CSPP and the bearish undertones is increasing. The exact tipping point on the seesaw is extremely difficult to identify ex ante, because as much as anything it is a function of market psychology. We may never reach it, or we may already have crossed it. The balance of probabilities is probably with the ECB, but factoring the asymmetry in up- versus downside, risk/reward feels very finely poised here. Hence, as we outlined last week, our preference remains to emphasise relative value over direction.

And in case you are wondering, yes, we think the European bank sector will need a whole lot more broccoli, before we are prepared to recommend it from a credit perspective again.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.