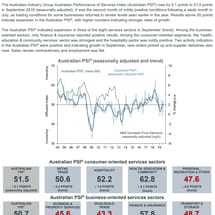

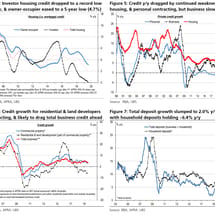

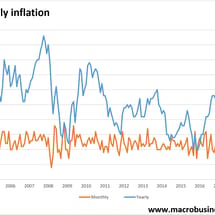

UBS: Business credit sucked down by apartment bust

Via UBS’s excellent George Theranou: Business credit is clearly slowing now (0.2% m/m, 3.4% y/y, lowest since Jun-18), amid ongoing tight credit to small business. Meanwhile, personal credit continues to contract sharply (-0.2% & -3.4% y/y), the ~worst since the GFC, and a negative signal for retail sales.