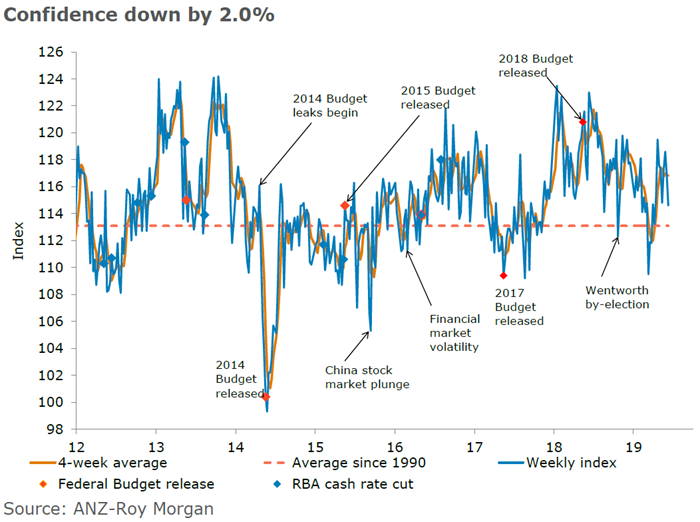

Weak Q1 GDP and the soft retail figure for April have seen consumer confidence move lower over the past week, despite the rate cut from the RBA. Looking back to the rate cuts in 2015 and 2016, there was no tendency for confidence to rise immediately following the move lower in rates. So it’s not particularly surprising that there has been no immediate boost from the rate cut. Inflation expectations readings below 4% seem to have become the norm in the past couple of month, which is unique in the history of this survey and something the RBA will be taking note of.”

And Westpac:

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.