Australian dollar bid as virus fixed!

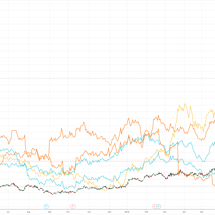

The Australian dollar is bid this afternoon as market damage winds back a little: Bond gains have softened at all-time low yeilds: XJO is still down solidly and has set up a massive double top: Iron ore is down a little: Big Iron is down more, execpt FMG, the most leveraged to price.