DXY eased last night as EUR firmed and CNY fell:

The Australian dollar continues to fall versus DMs:

Mixed against EMs:

Gold firmed:

Oil too:

Metals were mixed:

Miners fell:

EM stocks eased:

Junk firmed:

Treasuries rose:

Bunds too:

And Aussie bonds:

Stocks firmed:

More US housing data last night indicating that the bond rally, which pegs US fixed mortgage rates, has already lifted activity. Existing home sales were strong:

Existing-home sales inched up in August, marking two consecutive months of growth, according to the National Association of Realtors®. Three of the four major regions reported a rise in sales, while the West recorded a decline last month.

Total existing-home sales, completed transactions that include single-family homes, townhomes, condominiums and co-ops, rose 1.3% from July to a seasonally adjusted annual rate of 5.49 million in August. Overall sales are up 2.6% from a year ago (5.35 million in August 2018).

…Total housing inventory at the end of August decreased to 1.86 million, down from 1.90 million existing-homes available for sale in July, and marking a 2.6% decrease from 1.91 million one year ago. Unsold inventory is at a 4.1-month supply at the current sales pace, down from 4.2 months in July and from the 4.3-month figure recorded in August 2018.

A few more charts from WSJ’s Daily Shot make the point. Mortgage activity has lifted:

And construction is following:

Given US housing is the key leading indicator for any recession, its rebound catches the US dollar bears on the hop and is real support for a stable Federal Reserve.

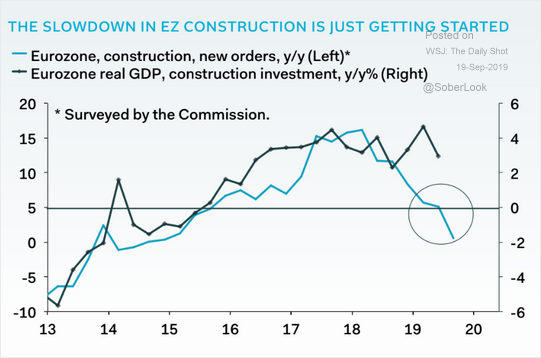

The ECB has acted with more easing but transmission into European property markets is much more patchy and unpredictable. Germany has seen prices rise:

But it’s not clear that it will translate into construction:

Economically, the US remains the developed market out-performer and the USD is still sought after. I would be surprised if this is not reflected in an even higher DXY in the short to medium term.

Weighing, of course, on the Australian dollar.