The Australian dollar caught bid against most DMs:

And EMs:

Gold took off:

Advertisement

Oil was hit:

Metals too:

Big miners were crushed:

Advertisement

EM stocks broke:

Junk shook:

Treasuries were popular:

Advertisement

The bund curve was plastered:

Aussie bonds boomed:

And stocks choked:

Advertisement

Wrap from Westpac:

Event Wrap

US House Speaker Pelosi is reportedly set to announce a formal impeachment inquiry of President Trump, according to some House officials, after revelations that Trump pressured the Ukraine government to investigate Joe Biden, currently a Democratic presidential contender for the 2020 election. Pelosi is set to make an announcement at 5:00pm, following a meeting with House Democrats, although there are conflicting reports about exactly what she will announce.

A weaker than expected US Conference Board consumer confidence survey saw the headline level pulled back from the strength seen in recent months to 125.1 (est. 133.0, prior revised to 134.2, post crisis high in 2018 of 137.90), with the present situation dipping to 169.0 (from post crisis high of 176.0 in August), and expectations at 95.8 (prior 106.4). Although the pullbacks were disappointing, the levels remain at relatively high post-crisis levels. US Richmond Fed Sept. manufacturing survey also disappointed at -9 (est. unch. at +1), pulling back towards July’s surprise low at -12.

Germany’s IFO survey was mixed. Although the current assessment managed to lift to 98.5 (est. 96.9, prior 97.4), expectations slipped to a new post crisis low of 90.8 (est. 92.0, prior 91.3), while the headline measure rose from 94.3 to 94.6 (est 94.5).

The UK Supreme Court ruled unanimously that the Johnson government’s suspension of Parliament was unlawful and that it should be quashed. Parliament will now return to Westminster for normal business at 11:30 on Wednesday. Opposition leader Corbyn announced that PM Johnson should be removed and that a general election should be called, as soon as the risk of no deal Brexit is eliminated.

RBA Governor Lowe said Australia’s economy is at a “gentle turning point” and reiterated he’s prepared to cut interest rates if needed to support the recovery, but he did not signal an imminent move which some in the market had been hoping for.

Event Outlook

Having got ahead of the curve in August with a 50bp cut, the RBNZ is expected to be on hold at today’s OCR Review. Another 25bp cut is however expected in Nov. The Aug trade balance is also due.

In the US, FOMC members Evans, George and Kaplan will speak. New home sales are set for a small rebound in Aug after July’s fall.

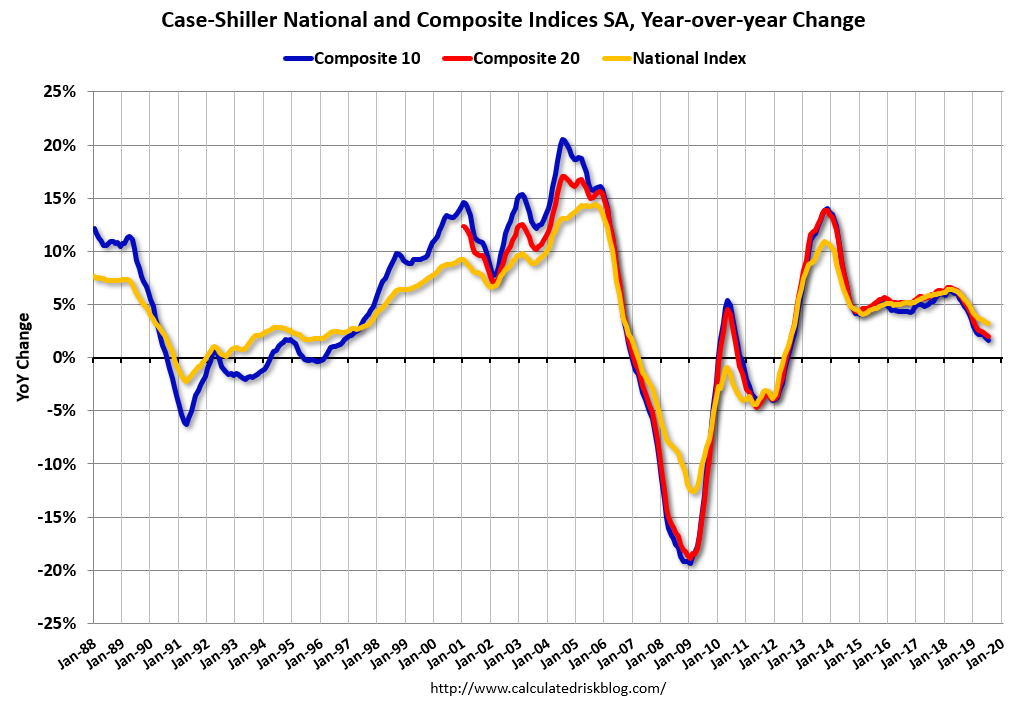

The economic news was mixed with US property prices showing early signs of price stabilisation:

The S&P CoreLogic Case-Shiller U.S. National Home Price NSA Index, covering all nine U.S. census divisions, reported a 3.2% annual gain in July, remaining the same from the previous month. The 10 City Composite annual increase came in at 1.6%, down from 1.9% in the previous month. The 20-City Composite posted a 2.0% year-over-year gain, down from 2.2% in the previous month.

Phoenix, Las Vegas and Charlotte reported the highest year-over-year gains among the 20 cities. In July, Phoenix led the way with a 5.8% year-over-year price increase, followed by Las Vegas with a 4.7% increase, and Charlotte with a 4.6% increase. Seven of the 20 cities reported greater price increases in the year ending July 2019 versus the year ending June 2019.

…Before seasonal adjustment, the National Index posted a month-over-month increase of 0.4% in July. The 10-City Composite remained flat and the 20-City Composite reported a 0.1% increase for the month. After seasonal adjustment, the National Index recorded a 0.1% month-over-month increase in July. The 10-City Composite posted a 0.1% decrease and the 20-City Composite did not report any gains. In July, 15 of 20 cities reported increases both before and after seasonal adjustment.

Advertisement

The Richmond Fed was soft at -9 and consumer confidence fell at the Conference Board:

The Conference Board Consumer Confidence Index® decreased in September, following a slight decline in August. The Index now stands at 125.1 (1985=100), down from 134.2 in August. The Present Situation Index – based on consumers’ assessment of current business and labor market conditions – decreased from 176.0 to 169.0. The Expectations Index – based on consumers’ short-term outlook for income, business and labor market conditions – declined from 106.4 last month to 95.8 this month.

“Consumer confidence declined in September, following a moderate decrease in August,” said Lynn Franco, Senior Director of Economic Indicators at The Conference Board. “Consumers were less positive in their assessment of current conditions and their expectations regarding the short-term outlook also weakened. The escalation in trade and tariff tensions in late August appears to have rattled consumers. However, this pattern of uncertainty and volatility has persisted for much of the year and it appears confidence is plateauing. While confidence could continue hovering around current levels for months to come, at some point this continued uncertainty will begin to diminish consumers’ confidence in the expansion.”

What mattered more was political risk as Dems finally plunged into impeachment proceedings:

Advertisement

Breaking: House Speaker Pelosi to announce formal impeachment inquiry of Trump after resisting for months https://t.co/8HjXyr1pi5

At issue is another Russian conspiracy in which Trump is accused of inciting a foreign power to damage a politcal rival in Joe Biden. I have no idea how this will run but Trump immediately released transcripts:

I am currently at the United Nations representing our Country, but have authorized the release tomorrow of the complete, fully declassified and unredacted transcript of my phone conversation with President Zelensky of Ukraine….

….You will see it was a very friendly and totally appropriate call. No pressure and, unlike Joe Biden and his son, NO quid pro quo! This is nothing more than a continuation of the Greatest and most Destructive Witch Hunt of all time!

It’s usually a very bad idea to impeach “hard men” leaders unless you have very strong evidence to do so. Throwing mud at them only makes them look stronger. This does not appear to be an overly strong case.

I have no special insight whether this is so but while we find out it is going to add a headwind to the USD bid, and lift the AUD commensurately.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.