DXY remains the only game in town as EUR hit new lows and CNY is not far behind:

The Australian dollar was hammered versus USD, fell against other DMs:

Advertisement

And EMs:

Gold was hosed:

Oil too:

Advertisement

Metals did better:

And miners:

EM stocks held on:

Advertisement

Junk fell:

All bonds as well:

Stocks recovered some:

Advertisement

Trump did his best to lift the Aussie dollar, at Reuters

U.S. President Donald Trump said on Wednesday that a deal to end a nearly 15-month trade war with China could happen sooner than people think and that the Chinese were making big agricultural purchases from the United States, including of beef and pork.

“They want to make a deal very badly… It could happen sooner than you think,” Trump told reporters in New York.

Trump said later after trade discussions with Japanese Prime Minister Shinzo Abe there was a good chance of reaching a trade deal with China.

Trump also released his Ukraine transcript which markets have decided showed no smoking gun for impeachment, via FT:

Advertisement

Donald Trump asked his Ukrainian counterpart to investigate former vice-president Joe Biden and his son, according to a White House record of a call between the leaders that was released one day after the House opened an impeachment inquiry.

The transcript — a non-verbatim memo of the July 25 call by White House note takers — was hailed by Mr Trump’s supporters as evidence that he had not tried to pressure Ukrainian president Volodymyr Zelensky to investigate the Bidens by threatening to withhold $391m in military aid.

The memo did show that Mr Trump responded to Mr Zelensky’s offer to buy more US Javelin missiles by asking him to “do us a favour” related to the “whole situation with Ukraine”, and later asked the Ukrainian president to talk to William Barr, his attorney-general, and Rudy Giuliani, his personal lawyer, about Hunter Biden and his father.

It looks pretty murky. Politico has line by line analysis. These kinds of things do not unravel all at once so the market’s confidence may be premature. That said, Ukraine backed Trump:

“I don’t want to be involved in the democratic elections of the U.S.A.”

Ukrainian President Zelenskiy responded to allegations of coercion, while Trump said there was “no pressure” on him to investigate Biden #UNGApic.twitter.com/3WYyIpyyzK

For now, none of can help the battler. It was mowed down by a rampant US dollar which enjoyed surging housing data:

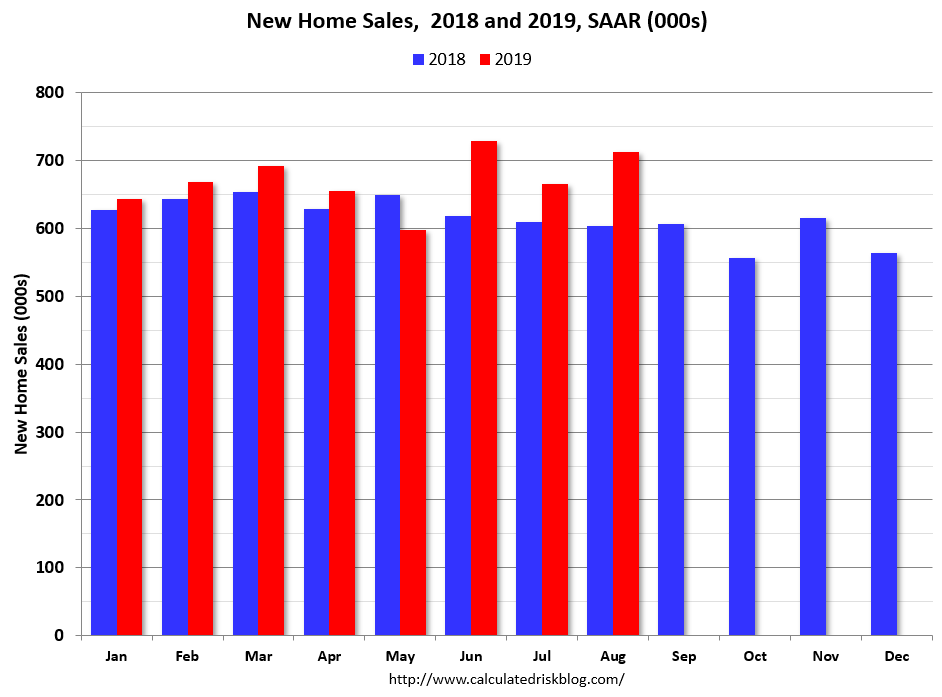

“Sales of new single‐family houses in August 2019 were at a seasonally adjusted annual rate of 713,000, according to estimates released jointly today by the U.S. Census Bureau and the Department of Housing and Urban Development. This is 7.1 percent above the revised July rate of 666,000 and is 18.0 percent above the August 2018 estimate of 604,000. ”

Advertisement

There is no way that that is an economy heading for recession. Not yet, at least. The bond panic has already materially lifted the outlook for activity.

There are still warning signs that the jobs market is slowing:

Advertisement

As industry is under pressure:

But it all looks rather “soft landing” at this point and the Fed would be quite happy to see the labour market ease given core inflation is rising.

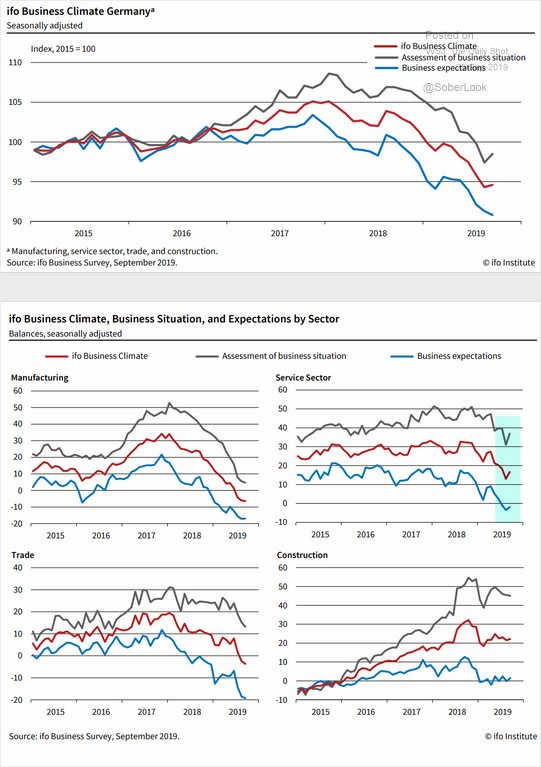

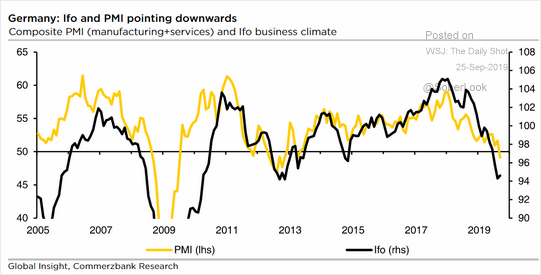

This contrasts with Europe where it is still getting worse. The German IFO was crapola again:

Advertisement

There’s worse to come:

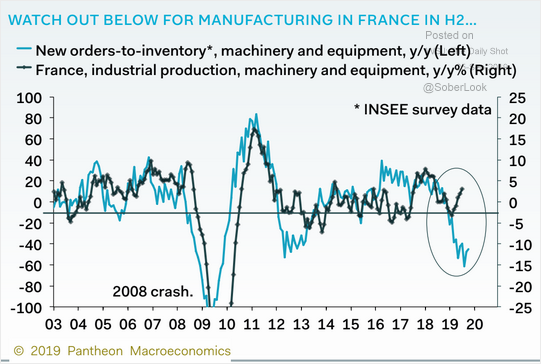

France is about to drawn in:

Advertisement

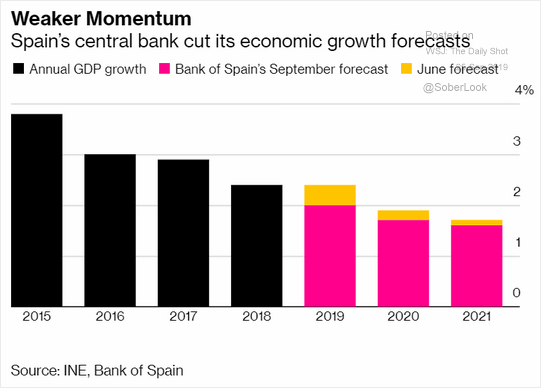

And it is seeping into the red hot periphery as well:

Owing to its fiscal paralysis there is only the ECB to lift activity and it’s shooting with blanks other than a falling EUR. Meanwhile, a slowing China and Brexit keep hitting it with external shock.

Advertisement

There remains only one bet in town, the USD and DXY, as America First delivers itself growth and inflation ahead of everywhere else. This, in turn, squashes activity in most exporters to the US, makes their funding costs higher as well, and kills off commodity prices owing to both.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.