DXY was strong last night with EUR and CNY fading:

The Australian dollar was universally sold:

Gold took a hit and looks vulnerable for more:

Advertisement

Oil retraced further:

As did metals:

And miners:

Advertisement

Plus EM stocks:

Junk did better:

Treasuries and bunds sold:

Advertisement

Aussie bonds were bid:

Stocks fell moderately:

The culprit was the Fed:

Advertisement

Information received since the Federal Open Market Committee met in July indicates that the labor market remains strong and that economic activity has been rising at a moderate rate. Job gains have been solid, on average, in recent months, and the unemployment rate has remained low. Although household spending has been rising at a strong pace, business fixed investment and exports have weakened. On a 12-month basis, overall inflation and inflation for items other than food and energy are running below 2 percent. Market-based measures of inflation compensation remain low; survey-based measures of longer-term inflation expectations are little changed.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. In light of the implications of global developments for the economic outlook as well as muted inflation pressures, the Committee decided to lower the target range for the federal funds rate to 1-3/4 to 2 percent. This action supports the Committee’s view that sustained expansion of economic activity, strong labor market conditions, and inflation near the Committee’s symmetric 2 percent objective are the most likely outcomes, but uncertainties about this outlook remain. As the Committee contemplates the future path of the target range for the federal funds rate, it will continue to monitor the implications of incoming information for the economic outlook and will act as appropriate to sustain the expansion, with a strong labor market and inflation near its symmetric 2 percent objective.

In determining the timing and size of future adjustments to the target range for the federal funds rate, the Committee will assess realized and expected economic conditions relative to its maximum employment objective and its symmetric 2 percent inflation objective. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments.

Voting for the monetary policy action were Jerome H. Powell, Chair, John C. Williams, Vice Chair; Michelle W. Bowman; Lael Brainard; Richard H. Clarida; Charles L. Evans; and Randal K. Quarles. Voting against the action were James Bullard, who preferred at this meeting to lower the target range for the federal funds rate to 1-1/2 to 1-3/4 percent; and Esther L. George and Eric S. Rosengren, who preferred to maintain the target range at 2 percent to 2-1/4 percent.

Not many doves there. And the dots were confident:

No more rate cuts forecast.

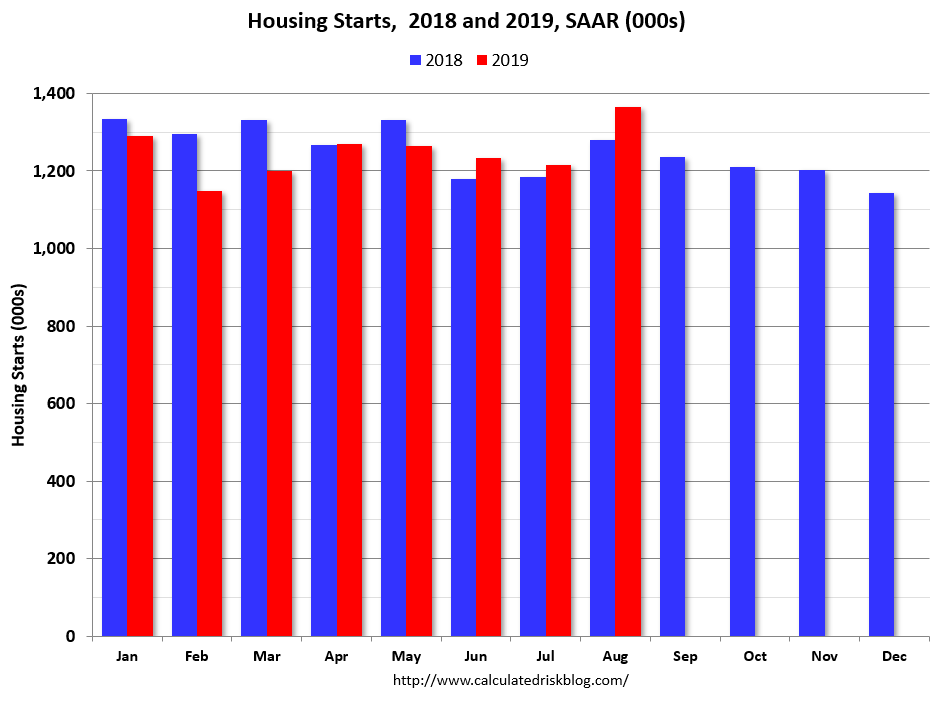

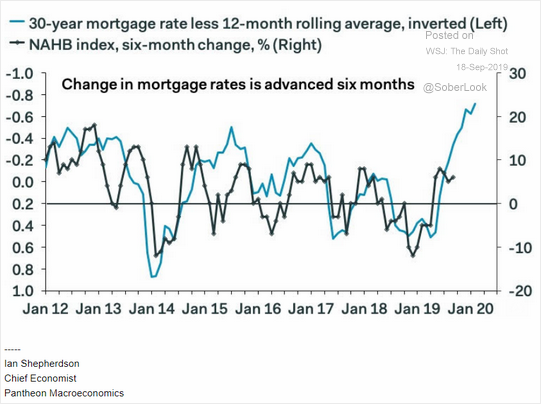

In support of that, the data was good. In particular, the bond market has already revived the housing pulse:

Housing Starts:

Privately‐owned housing starts in August were at a seasonally adjusted annual rate of 1,364,000. This is 12.3 percent above the revised July estimate of 1,215,000 and is 6.6 percent above the August 2018 rate of 1,279,000. Single‐family housing starts in August were at a rate of 919,000; this is 4.4 percent above the revised July figure of 880,000. The August rate for units in buildings with five units or more was 424,000.

Building Permits:

Privately‐owned housing units authorized by building permits in August were at a seasonally adjusted annual rate of 1,419,000. This is 7.7 percent above the revised July rate of 1,317,000 and is 12.0 percent above the August 2018 rate of 1,267,000. Single‐family authorizations in August were at a rate of 866,000; this is 4.5 percent above the revised July figure of 829,000. Authorizations of units in buildings with five units or more were at a rate of 509,000 in August.

Advertisement

With more to come:

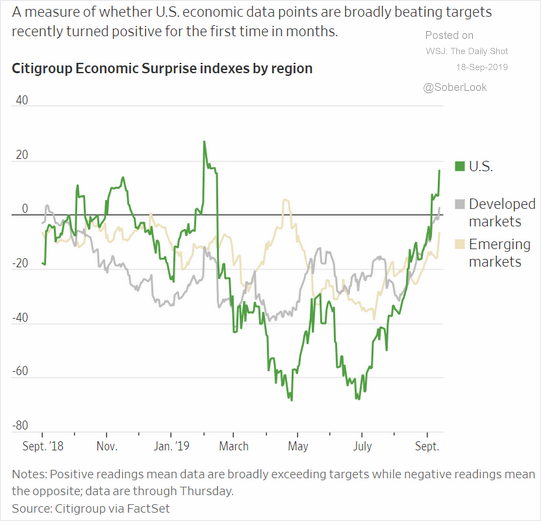

And the US has led a recovery in economic surprises globally:

Advertisement

It’s hard to see US growth falling much further with a healthy housing market, which usually leads economic weakness when it comes. As well, those Fed forecasts look quite happy to absorb any modest slowdown to quell wage and tariff inflation.

Powell was soothing in comments which lifted risk back to parity on the night but it was at the margin.

In short, the DXY bull case is intact and that strengthens the case for a lower Australian dollar.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.