Quite a mixed session across Asia today with Chinese stocks slumping, Australian advancing while the long weekend dampener has seen Japanese bourses remain steady, despite a weaker Yen. Oil prices haven’t moved much since their weekend gap, but this could be the calm before the storm as OPEC is due to hold a press conference soon, with the expected supply crunch likely to see increased volatility tonight.

What a shame Australia doesn’t have much in the way of a strategic oil reserve – she’ll be right and all that hey?

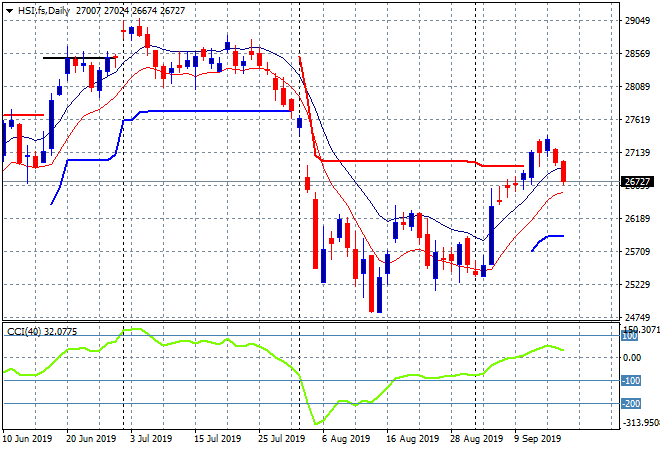

The Shanghai Composite slumped to finish nearly 2% lower at 2979 points, breaking below the 3000 point barrier that had been building as support while the Hang Seng Index followed in suit, closing 1.5% lower at 26726 points, also breaking below weak support/former resistance at 27000 points:

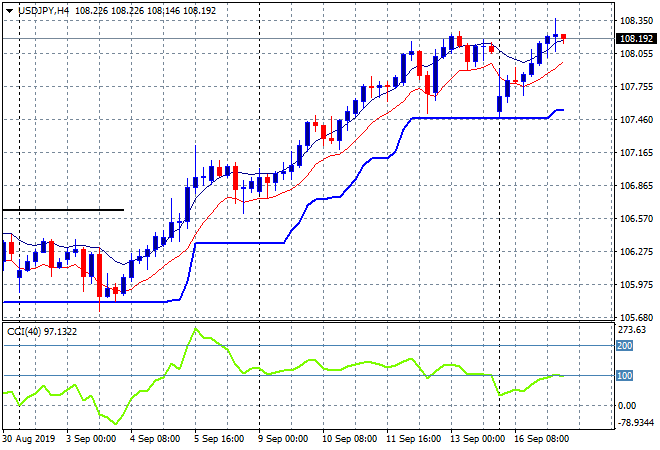

Japanese share markets reopened from their long weekend in a holding pattern with the Nikkei 225 closing right on 22000 points while the USDJPY pair advanced slightly above the 108 handle, and looks set to breakout to make a new weekly high soon:

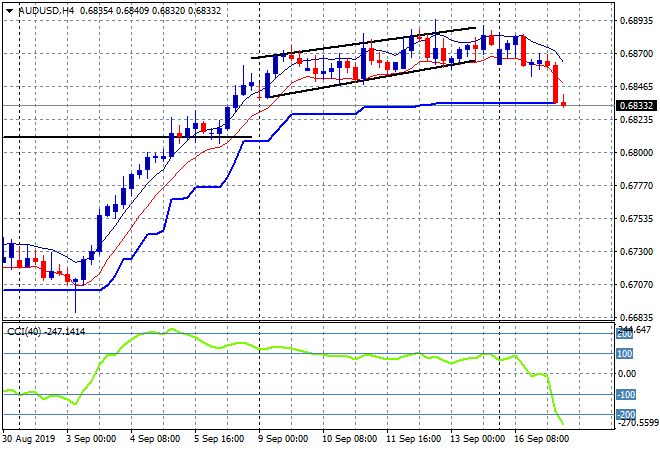

The ASX200 continued to make some gains in as iron ore advanced and the Australian dollar dropped on the back of the RBA minutes, climbing some 0.3% to finish at 6695 points. The Australian dollar finally moved – down – as the RBA easing bias is now crystal clear, sending the Pacific Peso off to a new weekly low, taking back all of last week’s gains and ready to break below tentative support:

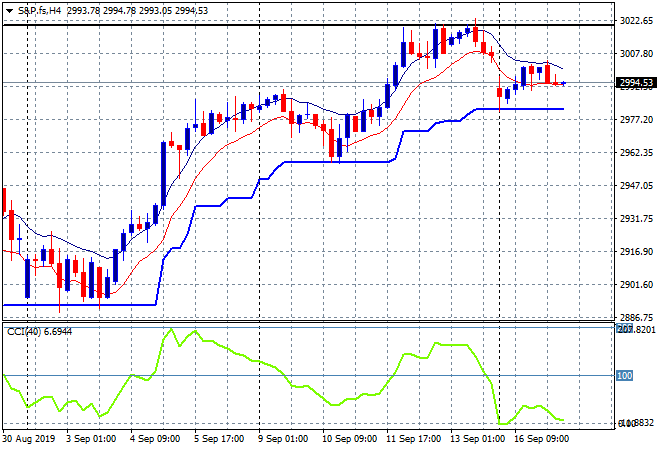

S&P and Eurostoxx futures are down only slightly as European markets open with the S&P500 four hourly chart showing a steady, if weak resolve just below the 3000 point barrier, as traders continue to weigh up the outcome of the Saudi oil attacks:

The economic calendar includes the closely watched German ZEW survey tonight, plus US industrial production for August.