DXY hit new closing highs last night as EUR sank and CNY fell:

The Australian dollar was roughly stable versus DMs:

Stronger than EMs:

Advertisement

Gold hung on but is clearly vulnerable:

Oil fell:

And metals:

Advertisement

Miners too:

EM stocks appear to have rolled:

High yield was OK:

Advertisement

Treasuries were bid:

Bunds too:

And Aussie bonds:

Advertisement

Stocks faded:

Westpac has the wrap:

Event Wrap

The third take on US 2Q GDP was broadly in line (remaining at an annualised 2.0%), but the core PCE component lifted to 1.9% (prior 1.7%) annualised. US trade balance data was much as expected at –USD72.8bn, with a notable lift in consumer and capital goods suggesting a push to beat tariffs on Chinese goods. US pending home sales in Aug rose 1.6%m/m, more than the anticipated +1.0%m/m, after July’s -2.5%m/m slip. Improvements were seen in all regions, with a notable lift of 3.1% in the West. Kansas Fed’s. manufacturing survey edged up to -2 from its recent low of -6 in August. There was anencouraging lift in production (+11 from -2) and new order declines were -3 from -16, but the employment component deteriorated, slipping to -13 from -7. FOMC member Kashkari said he did not forecast a recession, VC Clarida thought inflation was close to target, and Kaplan said trade uncertainty was affecting business investment.

German GfK consumer confidence firmed to 9.9 (est. 9.6, prior 9.7), suggesting stabilisation after slipping since mid-2018.

Event Outlook

NZ consumer confidence (ANZ) is below its historical average but did firm slightly in August. September’s survey will fully capture the RBNZ’s 50bp rate cut in August.

China industrial profit growth is expected to remain subdued in Aug, as global uncertainties weigh.

In Europe, confidence will again be in focus, with Euro Area economic and business confidence released and, in the UK, consumer sentiment.

Data in the US will have a higher profile. Durable goods orders will point to continued weakness in business investment. Personal income and spending data for Aug should be robust; however, Uni of Michigan sentiment will likely point to risks over the consumption outlook. PCE inflation will remain subdued, below the FOMC’s 2.0%yr target. Quarles and Harker will conclude a busy week for Fedspeak.

Politics was again ignored last night despite intensifying impeachment chatter, via FT:

Advertisement

The White House faced accusations of a cover-up on Thursday after the publication of a whistleblower complaint that alleged officials used a classified storage system to hide the transcript of a call between President Donald Trump and his Ukrainian counterpart.

The complaint added new details to a widening controversy over the call in which the US president asked his Ukrainian opposite number Volodymyr Zelensky to investigate Mr Trump’s potential election rival Joe Biden and the business dealings of his son, Hunter.

…According to the whistleblower — an anonymous intelligence official whose concerns have sparked an impeachment inquiry into Mr Trump — White House officials restricted access to details of the presidential call by storing the information in a specially classified storage system.

“I learnt from multiple US officials that senior White House officials had intervened to ‘lock down’ all records of the phone call, especially the word-for-word transcript of the call that was produced,” the whistleblower said in the written complaint. “This set of actions underscored to me that White House officials understood the gravity of what had transpired in the call.”

White House officials said internal lawyers debated how to handle the details of the July call, due to the “likelihood . . . that they had witnessed the president abuse his office for personal gain”, the whistleblower added.

Markets appear to remain comfortable that the US senate will block any real push for impeachment. There was also lots of positive rhetoric around a trade deal, as well as some negative around Huawei.

The balance was a breakout in King Dollar as US data flow, especially housing, is recovering. Pending home sales came in hot:

Advertisement

Pending home sales increased in August, a welcome rebound after a prior month of declines, according to the National Association of Realtors®. Each of the four major regions reported both month-over-month growth and year-over-year gains in contract activity.

The Pending Home Sales Index (PHSI), a forward-looking indicator based on contract signings, climbed 1.6% to 107.3 in August, reversing the prior month’s decrease. Year-over-year contract signings jumped 2.5%. An index of 100 is equal to the average level of contract activity.

…All regional indices are up from July, with the highest gain in the West region. The PHSI in the Northeast rose 1.4% to 94.3 in August and is now 0.7% higher than a year ago. In the Midwest, the index increased 0.6% to 101.7 in August, 0.2% higher than August 2018.

Pending home sales in the South increased 1.4% to an index of 124.4 in August, a 1.8% bump from last August. The index in the West grew 3.1% in August 2019 to 96.4, an increase of 8.0% from a year ago.

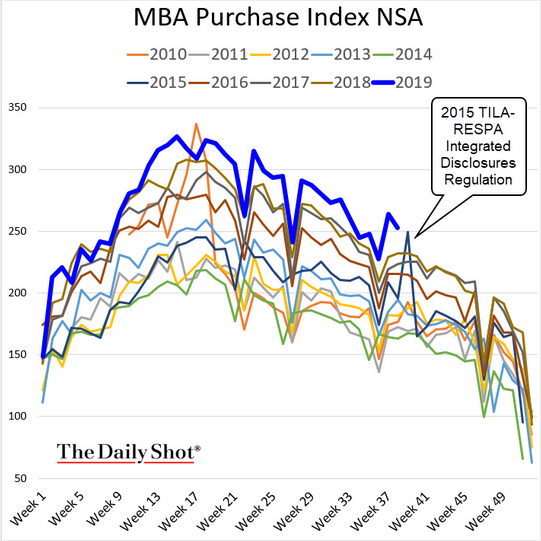

Mortgages are at record highs:

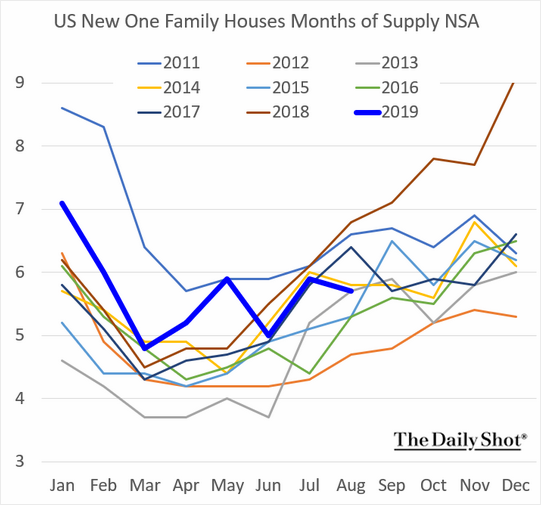

And inventories are fine:

Advertisement

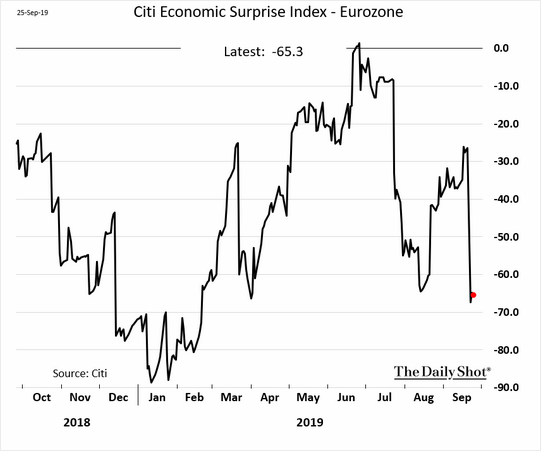

Citi’s economic surprise index has powered back:

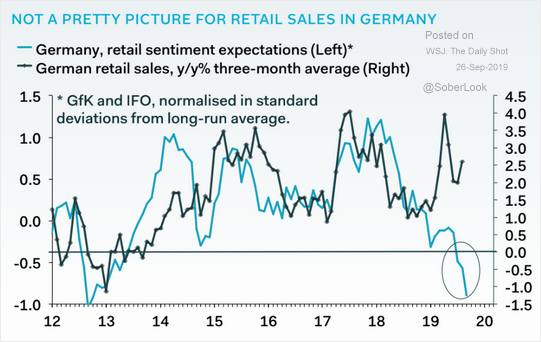

Meanwhile, the Eurozone keeps falling with Germany leading the way:

Advertisement

And the Citi economic surprise index keeps shocking:

So EUR keeps falling and DXY keeps rising.

This is not simply a benign bilateral forex shift. The higher DXY goes, the more pressure will come to bear upon EMs as external funding costs rise. This is a double whammy for commodities as demand falls and USD pricing becomes a headwind. Hence when EUR falls so does the AUD:

Advertisement

And there you have it. Until these dynamics shift, the AUD falls.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.