DXY eased Friday night as EUR and CNY bounced:

That was enough to hold the Australian dollar up:

CFTC positioning added more shorts last week, hitting -47k contracts:

Gold was hit:

And oil:

Metals were stable:

And miners:

EM stocks have rolled as DXY powers:

Junk is holding so far:

All bonds were bid:

Stocks took a solid hit:

Westpac has the wrap:

Event Wrap

The US administration announced that it would examine US investment and portfolio flows with China. The issues were reported to include Chinese companies listed on US exchanges, US exposure to China through state pension funds, and how these might be restricted.

US personal income rose 0.4%m/m in Aug, meeting expectations, with spending (+0.1%m/m, est. +0.3%m/m) and PCE (headline 1.4%, core 1.8%) broadly as anticipated. Durable goods orders – a volatile series – were mixed in Aug but overall firmer than anticipated. Headline orders edged up +0.2%m/m (est. -1.0%m/m) as did ex-transport orders (+0.5%m/m, est. +0.2%m/m) but non-defence capital goods dipped (-0.2%m/m, est. flat). Univ. of Michigan consumer confidence survey lifted to 93.2 (initial estimate 92.1, July 89.8) mostly on solid current conditions (108.5, prior 106.9) but also expectations (83.4, prior 82.4). Although 1yr inflation expectations were unchanged (2.8%), the 5-10yr outlook did rise (2.4% from 2.3%).

FOMC centrist Harker said he was not in favour of cutting at the last meeting, thinking it won’t have much impact, and feels the Fed should now remain on hold.

Eurozone Sept. economic confidence missed estimates (-0.22, est. +0.11), reflecting the broad weakening in other surveys. Disappointing German Aug. import prices (-0.6%m/m and -2.7%y/y, est. -0.3%m/m and -2.6%y/y) and French Aug CPI (headline +1.1%y/y and core +0.9%y/y, est. 1.3%y/y and 1.0%y/y) underscored the risk that inflation pressures are to the downside.

Event Outlook

NZ business confidence fell to a post-GFC low in Aug and is expected to remain weak in Sep. Aug dwelling consents are likely to edge lower again, but the level remains elevated.

Aust private credit to post another weak read in Aug. But new lending is now lifting, pointing to stronger momentum ahead.

China PMIs should continue highlighting global uncertainties’ heavy impact on China’s business community. Japanese and Korean industrial production are also expected to remain weak.

UK GDP final estimate to confirm Q2 contraction. Euro Area unemployment and German inflation are also due.

US: Chicago PMI and Dallas Fed survey will give regional colour on manufacturing industry.

The Trump capital flows attack is all wrong and, this morning, appears to already be in retreat, via Bloomie:

A U.S. Treasury official said there are no current plans to stop Chinese companies from listing on U.S. exchanges, a day after a report that the Trump administration is discussing ways to limit U.S. investors’ portfolio flows into China.

“The administration is not contemplating blocking Chinese companies from listing shares on U.S. stock exchanges at this time,” Treasury spokeswoman Monica Crowley said in an emailed statement on Saturday.

Crowley was responding to Friday’s Bloomberg News report on various measures under consideration by the U.S., including delisting Chinese companies from U.S. exchanges. The report unnerved markets, with the S&P 500 Index closing about 0.5% lower. U.S.-listed shares of China-based companies, such as Alibaba Group Holding and Baidu Inc., tumbled.

That’s awfully wrong-headed. If the US wants to correct the trade balance, and put a lid on Chinese growth, then it needs to tax capital inflows not outflows. China has excess savings, the US not enough. Not the other way around. It the US applied a Tobin tax to Chinese capital inflows then it would force China to abandon the currency peg. This, in turn, would drive the USD down and CNY up, as well as radically reduce Chinese domestic liquidity, crimping its credit boom. It would almost single-handedly force China into its needed structural reform towards consumption over investment, lifting US exports (and crashing Australian, which would likely smash the AUD).

If there is one reform that the world needs more than any other, it is the taxation of Chinese capital flows into the US, not the other way around.

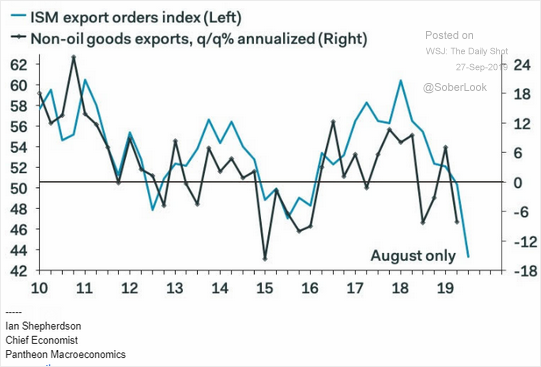

Meanwhile, cyclical indicators are unchanged for further AUD weakness. The US is still being drawn into global weakness:

Hitting business investment:

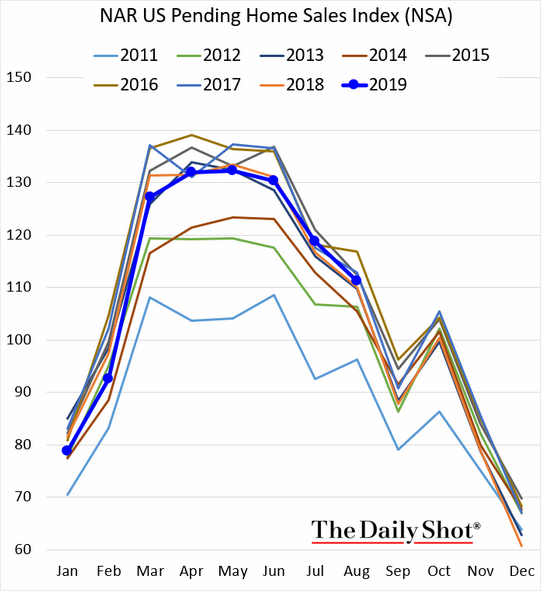

But the key housing sector is the great offset:

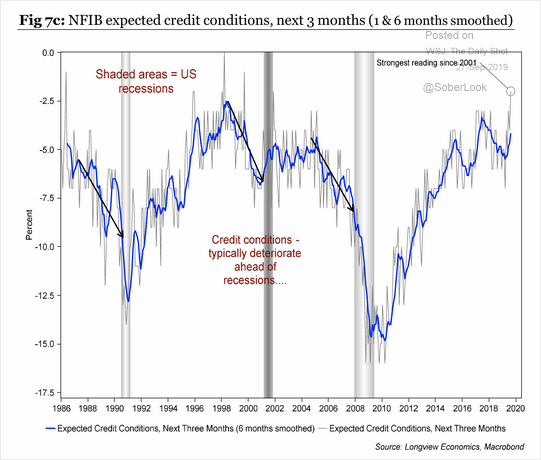

As credit conditions support:

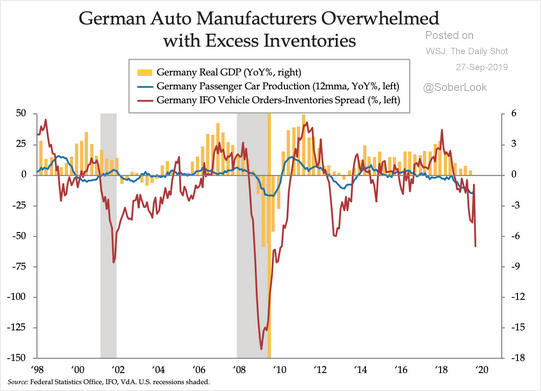

Across the pond, there is more weakness ahead for German autos:

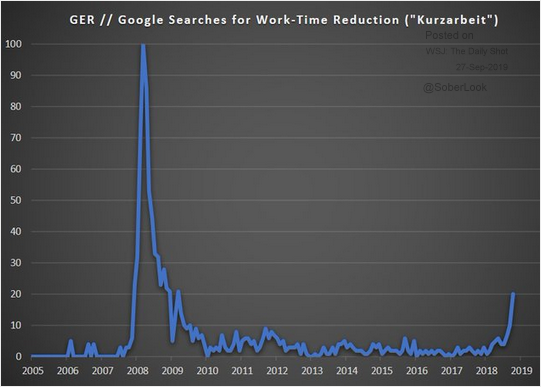

And here comes unemployment or, in Germany’s case, underemployment as its excellent Kurzabeit system kicks in:

The consumer is hanging on:

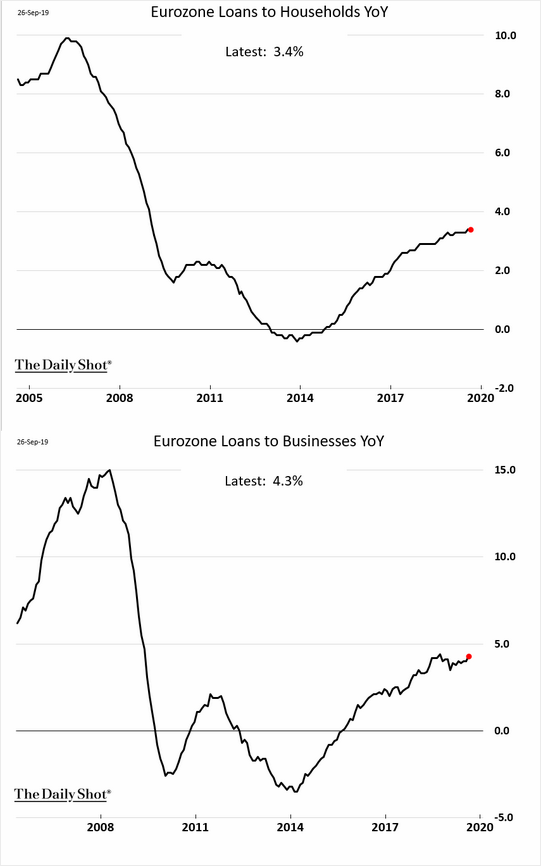

With credit:

As we know, so long as Europe is weaker than the US then the AUD will continue to be sold.