DXY was firm Friday night as EUR sank and CNY held on:

The Australian dollar was hammered:

The recent bounce blasted out a decent chunk of shorts at -40k contracts. Is there room now for the price to break to new lows?

Gold was strong despite DXY. It is trading as a trade war proxy:

Oil eased:

Metals were soft:

Miners too:

And EM stocks:

Junk fell:

Treasuries were bid bigly:

The bund curve flattened:

Aussie yields are getting caned again:

Stocks took a moderate hit:

Trade war rhetoric deteriorated as China cancelled part of its US trip and El Trumpo declared no interest in any “interim deal” nor getting any deal done prior to the election.

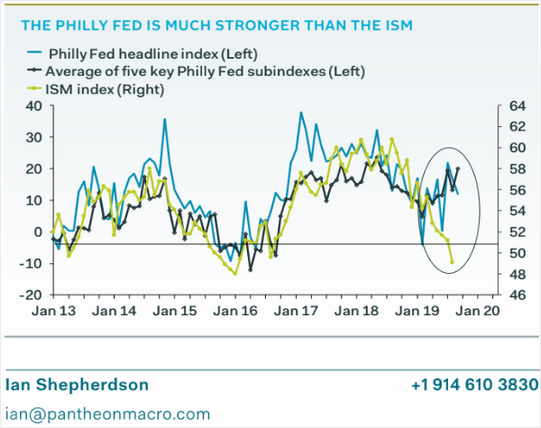

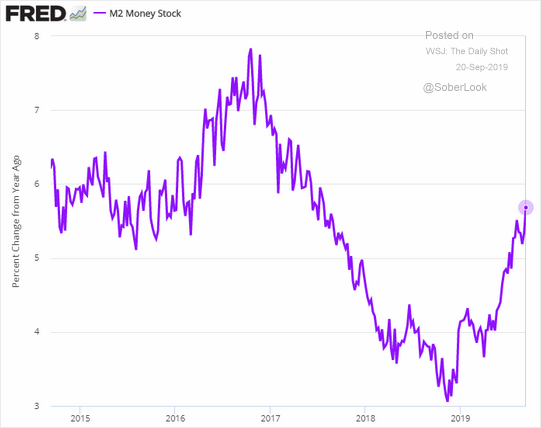

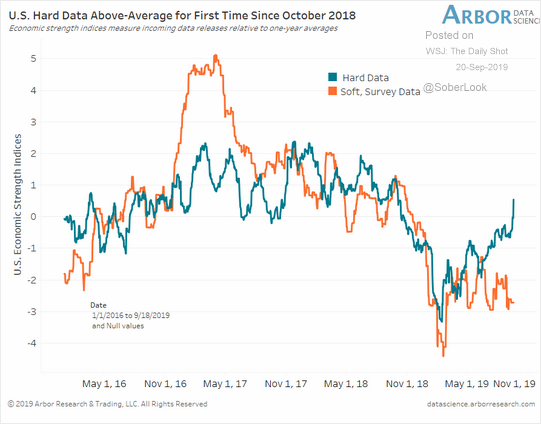

Perhaps his renewed confidence has something to do with a stabilising US economy. The following charts from WSJ Daily Shot paint a pretty decent picture. The supply side is still ticking along:

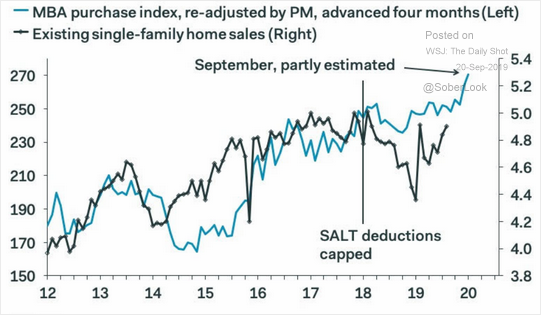

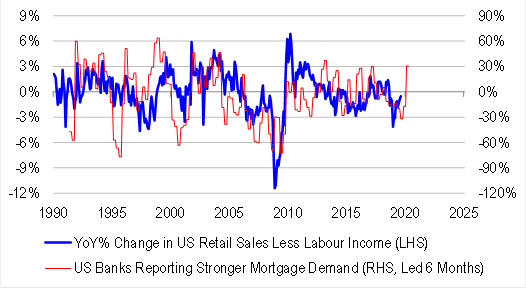

Demand is holding as lending is strong:

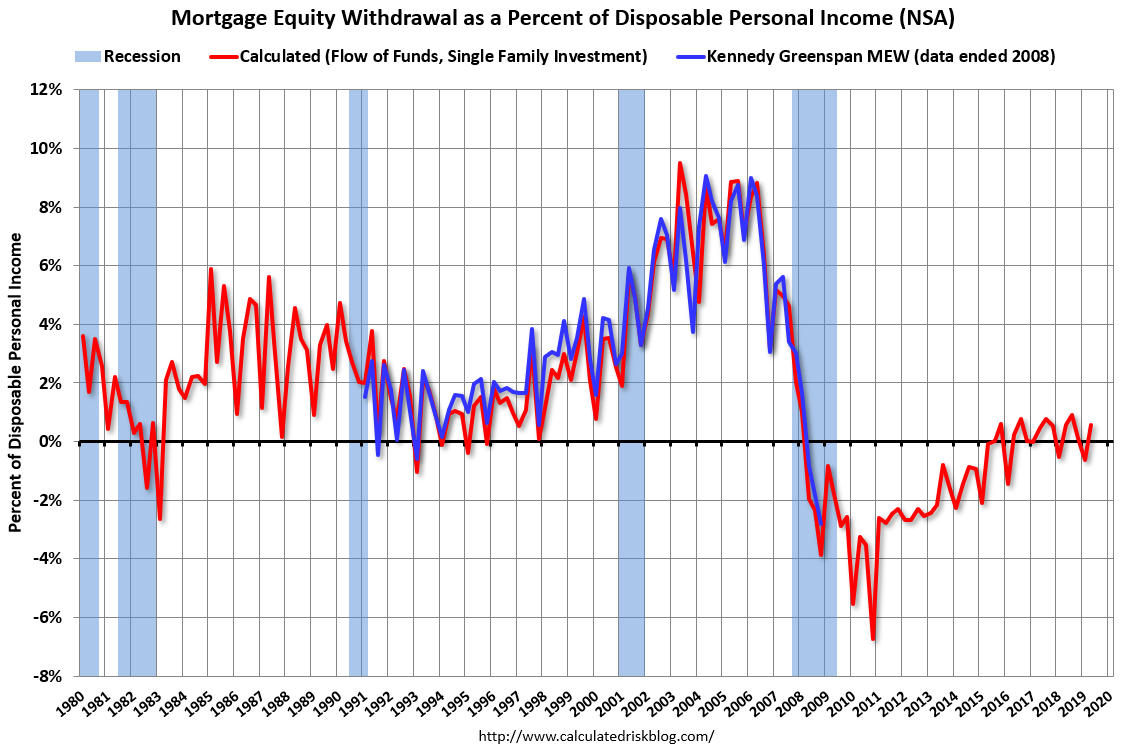

With house prices grinding higher and now mortgage equity withdrawal:

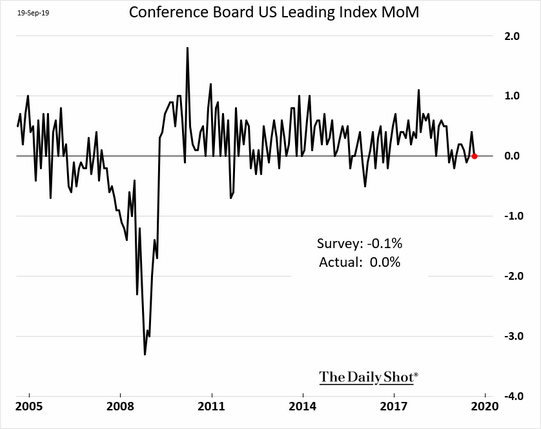

Keeping leading indexes OK:

The oil patch is the greatest worry but the US is still plodding along at 2% growth, enough to sustain a tight labour market. From Merrill Lynch:

We expect 2Q GDP to be revised slightly higher to 2.1% qoq saar in the final release. 3Q GDP tracking remains at 2.0% qoq saar.

From Goldman Sachs:

[W]e left our Q3 GDP tracking estimate unchanged on a rounded basis at +2.2% (qoq ar).

From the NY Fed Nowcasting Report

The New York Fed Staff Nowcast stands at 2.2% for 2019:Q3 and 2.0% for 2019:Q4.

And from the Altanta Fed: GDPNow

The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the third quarter of 2019 is 1.9 percent September 18, up from 1.8 percent on September 13.

Meanwhile, Germany disappointed again as its stimulus package proved fiscally neutral:

Merkel on Friday had the chance to use domestic concern about climate change as cover to issue new debt to re-set the economy on a green path and inject some short-term stimulus.

But the plan announced, offering a headline figure of 50 billion euros of new measures but in a budget-neutral package spread over four years, fell short of some expectations.

“We think any boost to demand would be too small to make much difference to short-term growth prospects in the euro-zone as a whole,” Andrew Kenningham of Capital Economics wrote in a note entitled “Wishful thinking about German fiscal policy”.

He noted that the package fell well short of the stimulus announced by Merkel’s coalition in 2009/10, worth 1.5% of GDP.

So, we have an ongoing circumstance of US-outperformance. In the past, one would see recovering US demand lead a recovery in global activity. But with the trade war in full roar, the transmission mechanism to higher Chinese exports is cut off. In turn, that weighs on European exports to China, made worse by Brexit worries and slowing.

The weakness everywhere outside of the US drives up the DXY, making it all worse as US dollar funding costs rise, an effective tightening of monetary policy everywhere.

America First can’t reflate the world. It can only lift DXY and drive AUD lower, right along with commodity prices as EM demand falls.

My guess is the Australian dollar is on the verge of new lows.