DXY has broken out again as CNY and EUR fall:

But the Australian dollar hung on grimly anyway versus DMs:

Not so much versus EMs:

Gold was thumped as DXY surged:

Oil too:

Metals were mixed but copper suffered:

Big miners were OK:

EM stocks hung on:

Junk lifted optimistically:

Treasuries were bid:

Bunds sold:

Aussie followed the latter:

Stocks tacked on gains:

Westpac has the wrap:

Event Wrap

Eurozone Aug. unemployment at 7.4% (est. 7.5%) continued its steady decline towards the low seen in early 2008 (7.3%). Sep German CPI (0.0%m/m, +1.2%y/y headline, vs est. 0.0%, +1.3%y/y) together with misses in Spain and Italy (missed estimates by -0.1% and -0.2% respectively) suggest that tomorrow’s Eurozone CPI may miss estimates (+1.0%y/y) by at least -0.1% and further underscore the lack of upside price pressures in the region. German Aug. retail sales (+0.5%m/m, +3.2%y/y) were firmer due to some upward revisions to July.

MNI’s Chicago PMI for Sep at 47.1 (est. 50.0) slid back into contraction after rebounding in Aug to 50.4 from 44.4 in July. Slippage was noted in new orders, production and inventories. Although employment improved it remained in contraction at 45.6. Dallas Fed’s. manufacturing survey dipped back to 1.5 (from 2.7 in Aug, est. was 1.0) but had a couple of improvements in orders to 5-month high, and although new orders slipped they remained above average levels. The key production level pulled back (to 13.9 from 17.9) but appears relatively stable.

Event Outlook

NZ: The NZIER business confidence survey, which is produced quarterly and closely followed by analysts, should provide a similar result to yesterday’s downbeat monthly version.

The RBA is set to cut the cash rate to 0.75% at their Oct meeting amid domestic and global uncertainties. Governor Lowe will then speak in Melbourne at 7.20pm AEST. Ahead of the RBA, house prices and dwelling approvals are also due.

In China, today sees the beginning of celebrations to mark 70 years of the People’s Republic. President Xi to speak. Chinese markets will be closed for 7 days.

Markit manufacturing PMIs is due for release in Asia, Europe and the US, along with US ISM manufacturing and construction data. The Fed’s Evans and Bowman will speak.

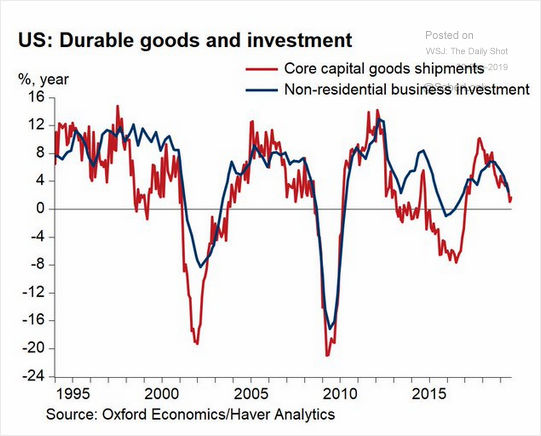

US data is beginning to resemble European with industry struggling but households keeping it together (charts from the Daily Shot). Manufacturing has stalled:

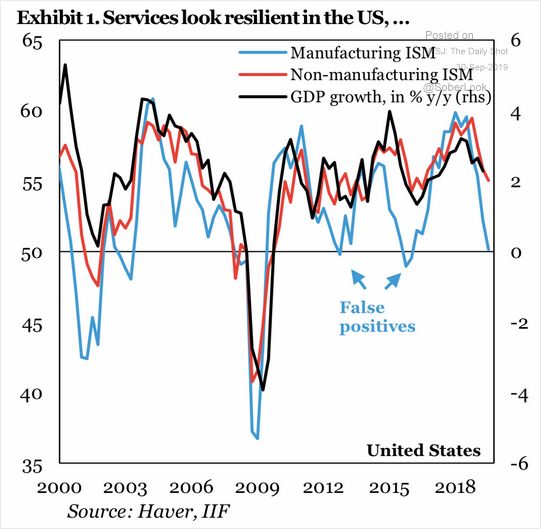

But services are strong:

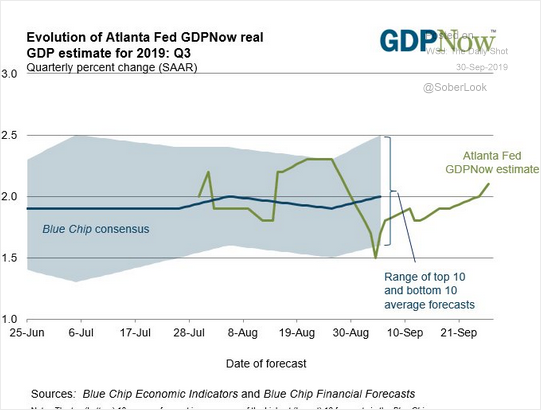

The mix is moderate GDP:

And moderate inflation:

Whereas Europe is materially further down the track of deterioration as weak Chinese and British imports have their way:

With mild recession:

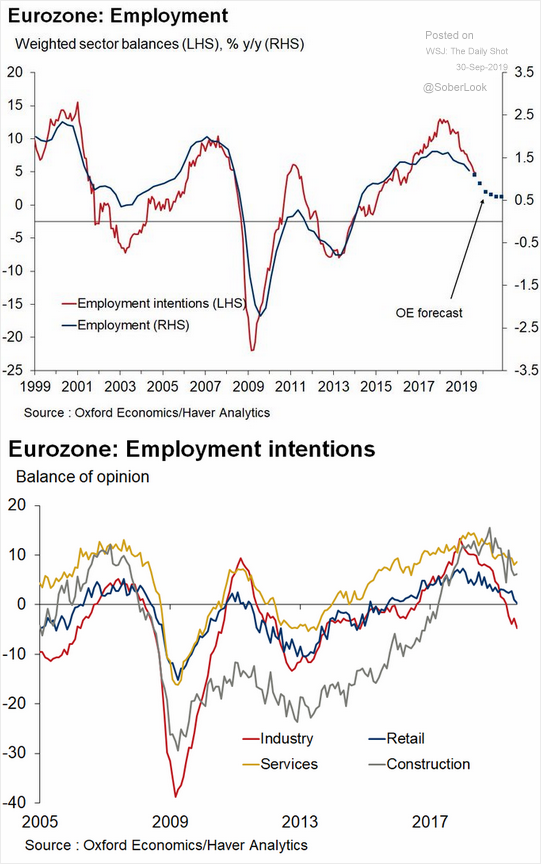

Now hitting employment:

With the obvious risk that households will fold in due course.

With CNY and EUR falling, the AUD is doing a remarkable job of holding it together in these circumstances. My best guess is it is in part iron ore, in part the epic market short position, and in part hopes for US/China trade resolution.

What I can say for certain is that so long as Europe falls and the US does not then AUD can only see further selling, just as in the case of gold.

When the AUD breaks lower may hang on when one of the three supporting factors also breaks.