RP Data weekly Australian house price update

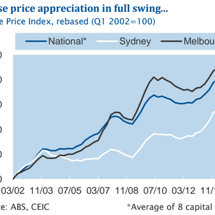

By Leith van Onselen In the week ended 28 May 2015, the Core Logic-RP Data 5-city daily dwelling price index, which covers the five major capital city markets, fell by 0.24% – the third consecutive weekly decline (see next chart). Values fell across Sydney and Melbourne, but rose elsewhere (see next chart).