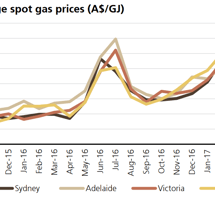

ACCC shames gas pensioner killers, backflips on reservation

The new gas narrative is given greater impetus today by the ACCC: Australian factories are at risk of shutting down and sacking workers as the nation’s gas exporters starve local customers in favour of overseas clients, according to a dire warning from the competition watchdog that clears the way for a gas crackdown.