It’s getting worse not better as Do-nothing Malcolm’s political barstardry leads the nation down the energy rabbit hole. From the AFR:

AGL Energy has moved to avert any push from Canberra to break up the company amid speculation that an expected attack by the competition watchdog on anti-competitive electricity supply will be seized on by politicians under pressure over power prices.

Chief financial officer Brett Redman said that forcing a split between the power generation and retailing activities of companies such as AGL would only hinder the much-needed investment in new supply that would bring down electricity prices.

“The market badly needs new generation,” Mr Redman told The Australian Financial Review. “Breaking up vertical integration will dramatically reduce the chances of this coming from private investment.”

Mr Redman’s comments come ahead of a public address by competition chief Rod Sims next week on the energy crisis, where he is expected to expand on his views that the increased integration between power production and retailing has worked against consumer interests and helped to drive up electricity prices.

The ACCC has been useless on energy. It’s report into the domestic gas shortage was a disaster of test tube economics and it approved the Shell takeover of BG just eighteen months ago, handing the giant Arrow reserve to the Curtis Island cartel.

EnergyAustralia chairman Graham Bradley has cautioned the Prime Minister Malcolm Turnbull against riding roughshod over AGL Energy CEO Andy Vesey, warning the CEO’s first duty is to his board, shareholders and his employees.

…This relates to both the Turnbull government’s move to try and keep AGL’s coal-fired power station in Liddell open post-2022 and the domestic gas mechanism to block gas exports as well as the Victorian government’s threat to re-regulate power prices in the state.

AGL’s Andy Vesey said on Monday after meeting Prime Minister Malcolm Turnbull that he would put the idea of extending Liddell to his board even though it was “economically irrational”. Andrew Meares

Leave business to business

Myer CEO Richard Umbers reflected the view of most business people on Thursday when he said “businesses are best left to run their businesses” and directors are all talking about whether the Turnbull, Vesey meeting sets a dangerous precedent following the government’s $6.2 billion bank tax and banker accountability regime.

“The Prime Minister must appreciate that the AGL CEO is answerable to a board which has fiduciary duties which cannot be overridden by Prime Ministerial fiat. He cannot direct the company to make a decision against the long-term interests of its shareholders,” Mr Bradley said.

I sympathise given the AGL attack is purely political. However, it must be noted that Mr Bradley was also a major rent-seeking voice against carbon price, the scrapping of which has in part led us here. Moreover, only government fiat can fix this energy crisis.

The point is that intervention should not be directed randomly at the power generators owing to crazed Coalition coal-fetishes. But we do need a government-led restructure of the failed gas market.

Industry remains deeply worried about the state of the gas market. Contract prices and availability are poor; the market remains non-transparent; and while there have been some recent positive signs of action by gas exporters, it is far too early to know how effective these will be in rebalancing the market. The most sensible course of action is for the Government to maintain pressure on gas exporters by invoking the ADGSM export controls. This will require you to determine that 2018 is a shortfall year under Regulation 13GE of the Customs (Prohibited Exports) Regulations 1958 (the Regulations). You have considerable leeway under the Regulations to amend such a decision subsequently if you decide circumstances warrant the tightening, loosening or removal of export controls. However you have no power to impose export controls on LNG in 2018 unless you make a shortfall determination by 1 November 2017. The asymmetry of these options further bolsters the case for making a shortfall determination in order to maintain your freedom to respond to developments in the gas market.

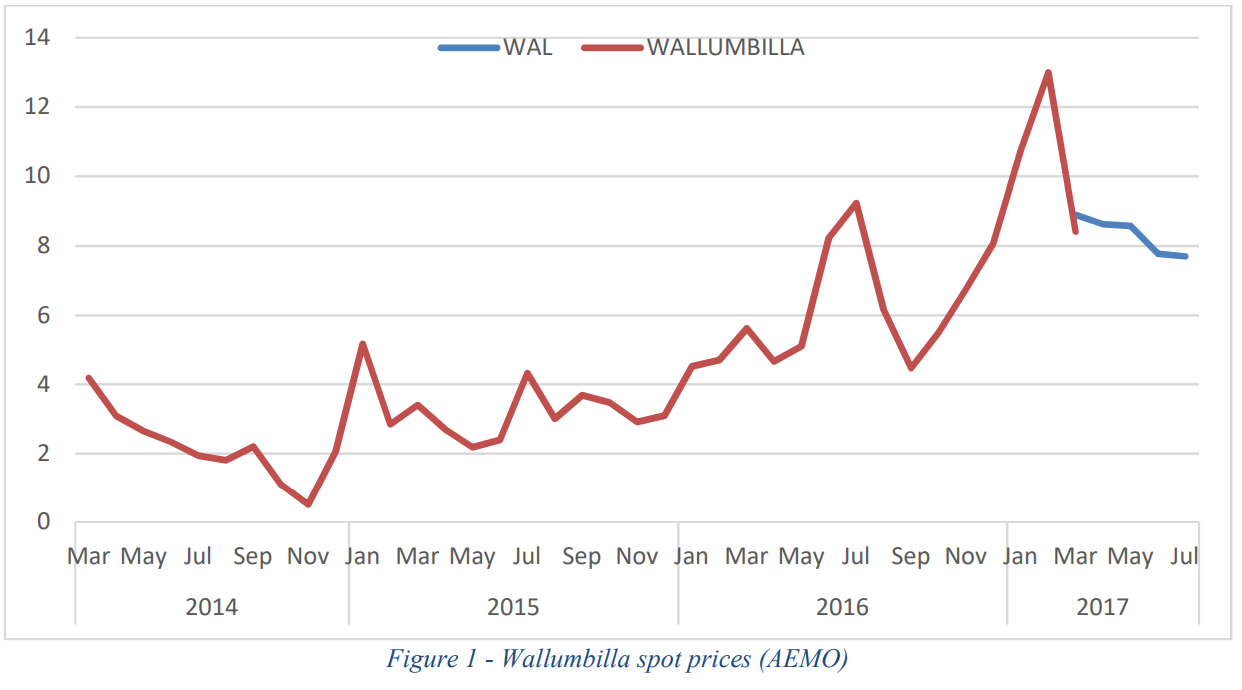

The Eastern Australian gas market is much less transparent than the electricity market and it is a great deal more difficult to observe meaningful prices. Most gas is sold through long-term and confidential bilateral contracts, not through open trading platforms. Most of the open platforms that exist are relatively new and all are largely used for balancing and dealing with transient shortfalls in demand and excesses of supply. There is no direct connection between these markets and the prices offered to retail gas customers.

The dip in late 2014 likely reflects the brief surge of uncontracted ‘ramp gas’ from wells coming into production to serve the not-yet-operating Queensland LNG export terminals. The spikes in July 2016 and January-February 2017 likely reflect surges in demand for gas-fired electricity when intense weather events coincided with problems for other generation sources. The dip since March likely reflects the easing of these seasonal pressures. The larger dynamics of the market – the volumes of gas sought and made available for long-term contracting – only lightly coincide with the pressures of this short-term market.

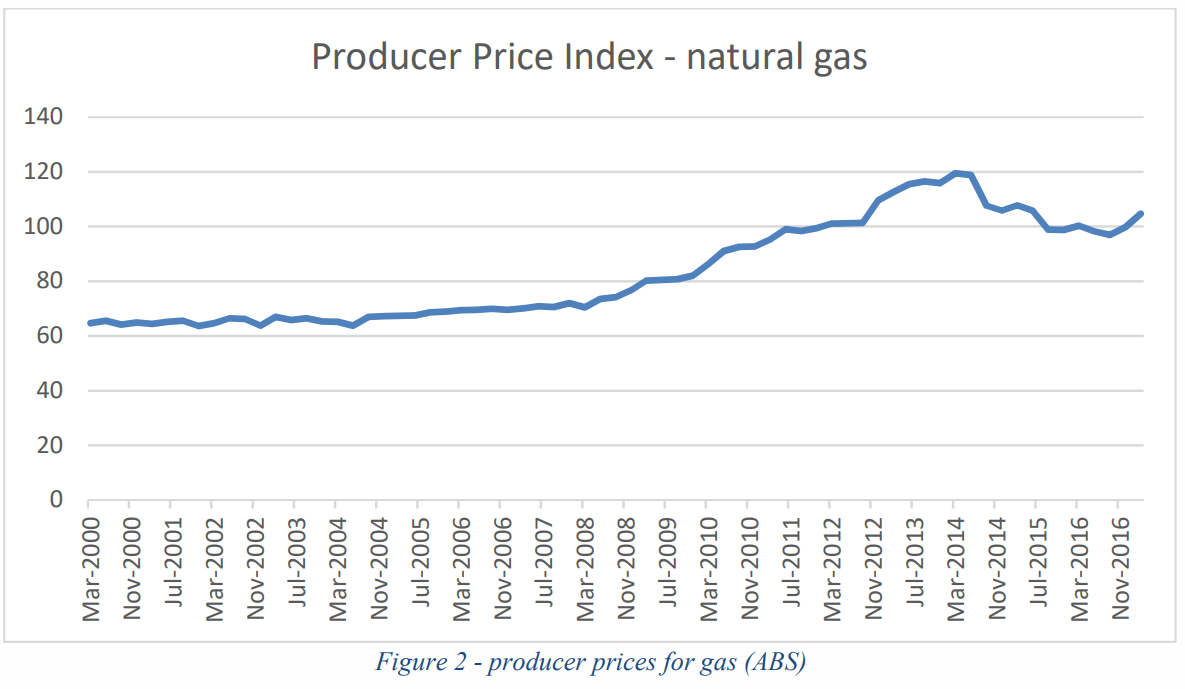

Seeking data directly from energy users is a more promising window into the market. One obvious source is the ABS Producer Price Indexes, which includes a measure of gas prices paid by businesses, including manufacturers. This index shows a gradual rise since around 2008, a shortlived price spike around the introduction and removal of the former carbon price, and only a modest uptick in the past year.

However, while the PPI is survey-based and substantial, there is a strong reason to believe that it is not a useful descriptor of the situation confronting most industrial gas users. As we understand it, the ABS includes LNG producers in their definition of manufacturers. LNG consumes vast volumes of natural gas – in Eastern Australia, LNG now uses twice as much gas as all other users combined – and much of this is produced by related entities and priced on an internal basis. The PPI is also a national index, encompassing the unconnected WA and NT markets where prices have differed greatly from the East. As a result, we think the PPI movements reflect the increased production of LNG and its internal pricing decisions, rather than anything visible to power, industrial and residential gas users.

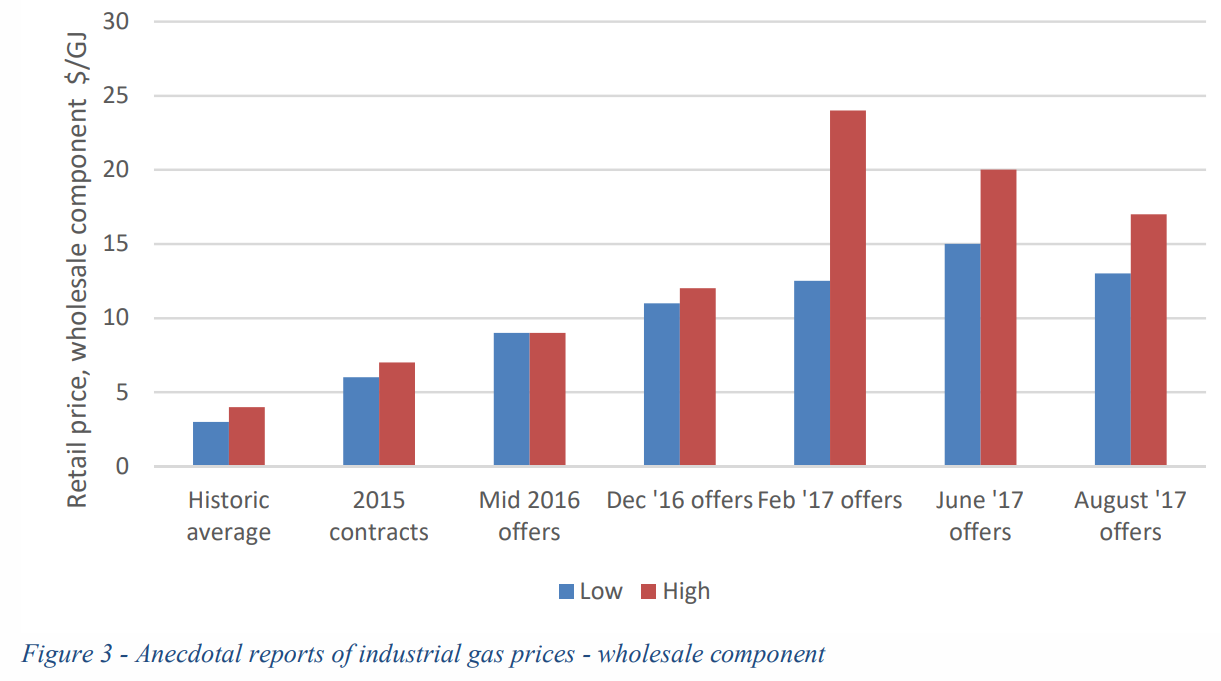

Our best guide to trends in gas pricing is the reports we receive from individual businesses. This is necessarily anecdotal and also needs to be treated with care; but the story from businesses of all sizes across many sectors has been very consistent, and is illustrated in the chart below.

In south-eastern Australia, the wholesale element of industrial gas bills used to be around $3-4 per gigajoule. Contracts concluding in 2016 often had prices around $6/GJ. Like-for-like prices offered have increased rapidly and dramatically since then, with high-end offers of up to $24/GJ emerging in February 2017 and average offers above $15/GJ in June. The highest prices have receded somewhat since February; we understand that the retailer who signed some customers up at above $20/GJ has subsequently acquired more gas and re-contracted with those customers at a modestly lower price. The latest input from our members is that prices offered range from $13-17/GJ and that contracts remain difficult to get. Businesses large enough to deal with producers directly often find that discussions go nowhere or that uncommercial terms are offered around volumes or duration; smaller gas users find that there are typically only two retailers at most in a position to offer contracts to industrial gas users, Origin and AGL, and no room for negotiation. The frequent message to industrial gas users of all sizes is that there is little gas to be contracted for, and that they need to take what is offered or risk missing out.

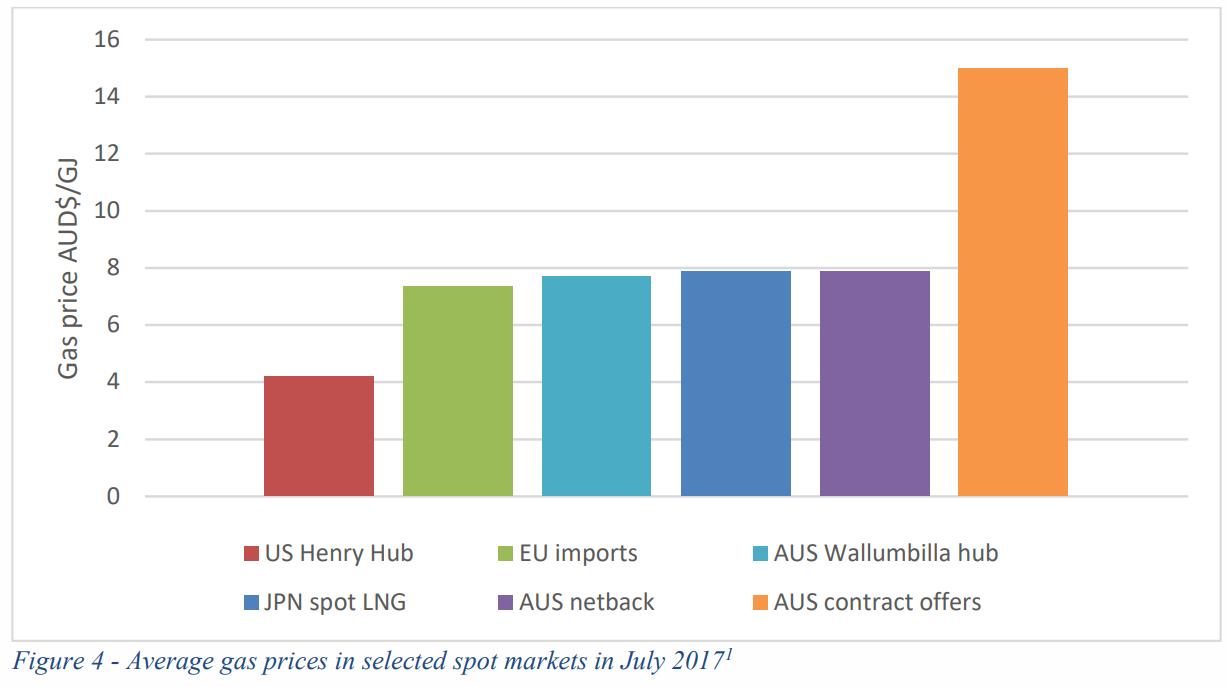

Meanwhile, global gas and LNG markets are strongly supplied and domestic prices are low in relevant major economies. As the chart below highlights, there is good alignment between spot gas import prices in Japan and Europe, the Wallumbilla spot price and a simple calculation of Eastern Australian oil-linked netback pricing. Recent Eastern contract prices are double that benchmark, and nearly four times higher than prices in the United States.

Thus while domestic prices do appear to have eased modestly since February, they remain far above international levels. Industrial energy users are experiencing enormous cost increases as a result. Network charges tend to be a much smaller proportion of the bill for industrial gas users and their overall price is lower than for residential customers. Contracts have tended to be multi-year. Thus many industrial gas users are experiencing a threefold increase in their gas prices from one contract to the next – a rise from around $6 to around $18 – or to report a four- or five-fold increase on the basis of a longer term comparison to the prices in older contracts. Our best explanation for the extreme rise in gas contract prices – not closely reflected in spot market outcomes – is that the market is out of balance. There is a looming and significant shortfall in uncontracted gas supply relative to the sum of pre-existing domestic demand and the new LNG industry’s requirements.

Given the marginal role of the spot markets compared to bilateral contracting, it is perfectly possible for longer term shortage to coexist with a spot market with very different dynamics. Demand destruction potentially means that spot market prices never match the highs of current contract prices for any sustained period.

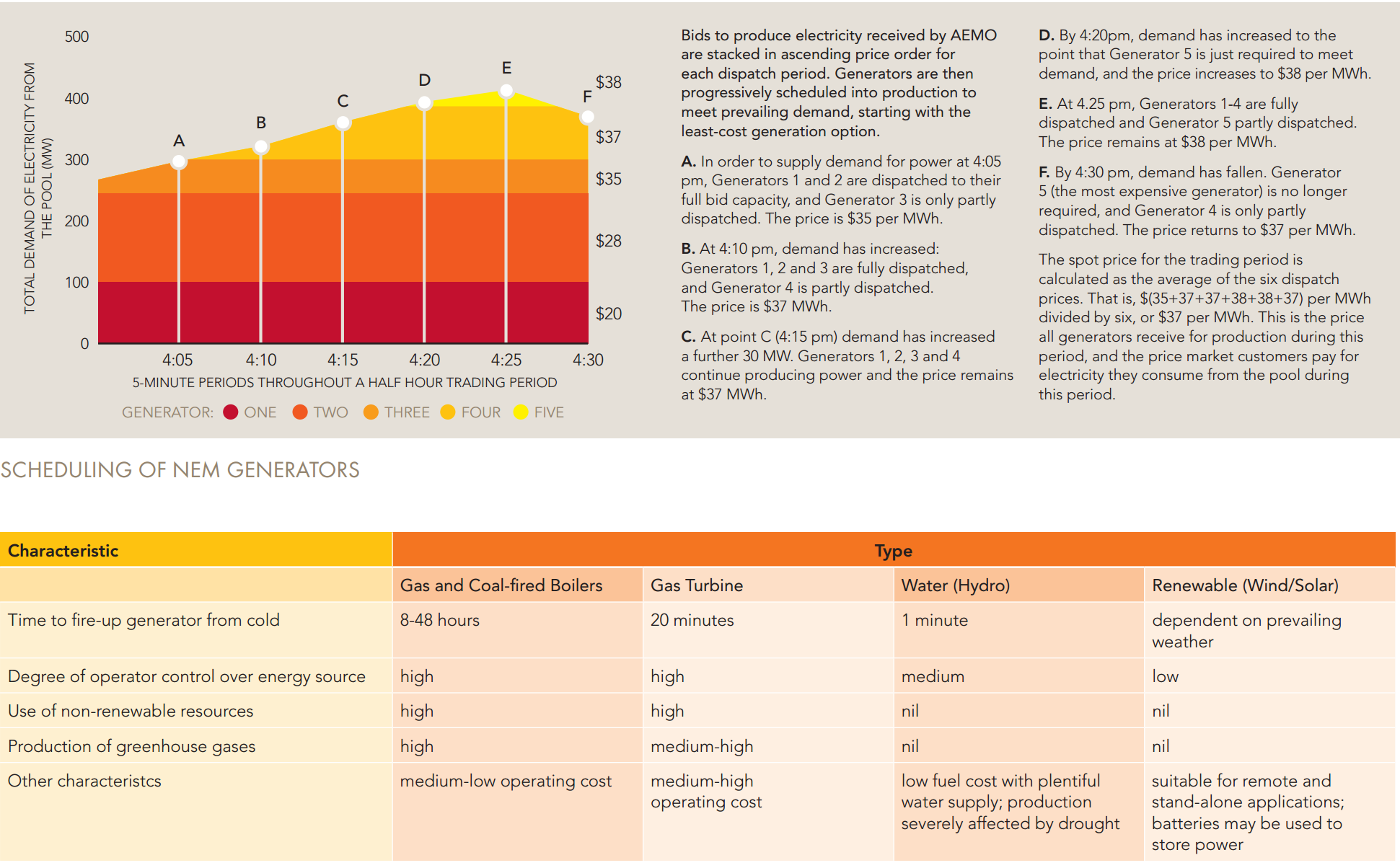

As we know, the gas price is the primary driver of rising electricity prices across the east coast economy. It is gas that sets the marginal cost of electricity owing to where it sits in the national electricity market (NEM). Via the Australian Energy Market Operator (AEMO):

Advertisement

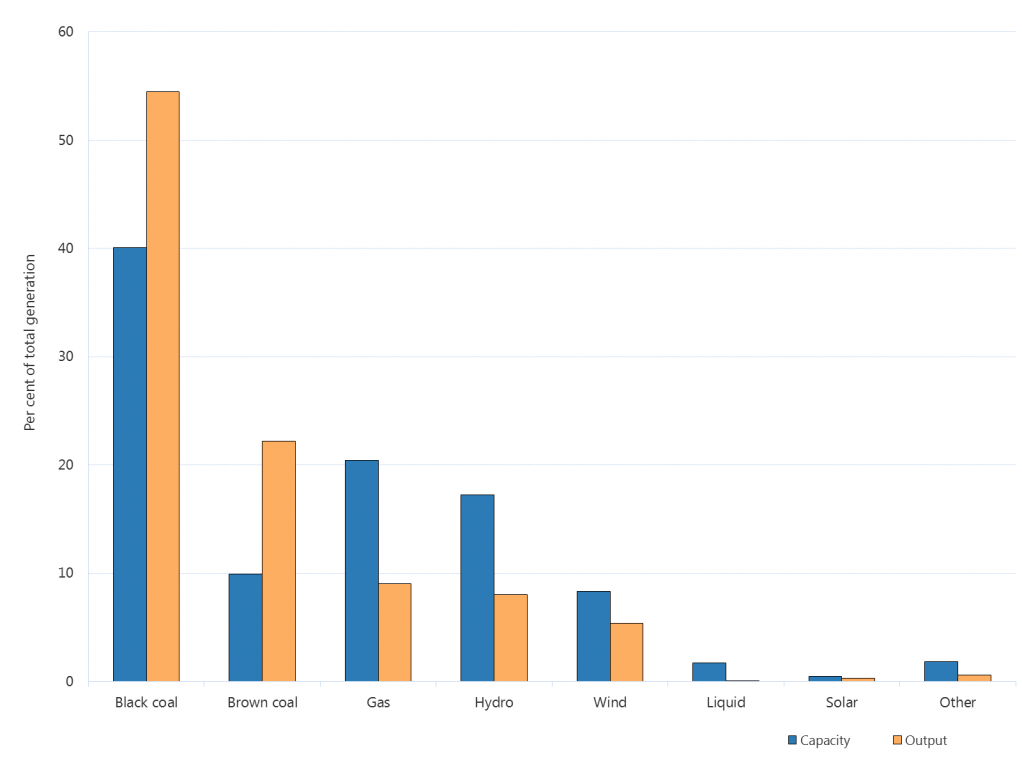

There are already oodles of gas generators offline across the country because the price is uneconomic, also from the AEMO:

Advertisement

If we had a lower gas price, then we would not be having this conversation at all, electricity prices would collapse. But we have a astronomically high gas price because an east coast gas cartel has monopolised and sold the cheap reserves to Asia.

The answer, the only answer, to the crisis, is unchanged. We need to fix the gas shortage and price so it can release present and future power generation resources.

If it wants to see quickly falling electricity and gas prices before the next election then the government’s gas reservation facility, the ADGSM, must be radically boosted. It is too slow and weak to bring down prices enough as it stands.

Advertisement

Longer term, the government will need to reshape the gas market too. It will need to nationalise somewhere along the supply chain. Buying Santos and shutting one LNG train is one option. Buying (or expropriating) and force developing reserves in a national gas company with mandated rates of return is another. Either of these options would benchmark east coast prices. The simplest and quickest solution is plain old price controls.

The east coast gas market has collapsed and requires radical restructure any way you look at it.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.