Domestic market accepts diverted Qld LNG gas; GLNG the surprise player

Our June 2017 research note on east coast gas concluded that there would be no physical gas shortage, just a shortage of cheap gas, as Queensland LNG projects divert more gas into the domestic market. Since June we have seen this thesis play out more rapidly than expected. The real surprise has been GLNG’s willingness to divert gas into the domestic market; GLNG was not expected to play a major role due to its gas-short position, unless compelled to via the Australian Domestic Gas Security Mechanism (ADGSM). However GLNG gas supplies are involved in 2 of the 3 contracts announced in the past 6 weeks, and Santos is involved in all of them.

Cooper Basin gas used as key swap volumes to minimise pipeline tariffs

A key feature of these agreements has been the use of gas swaps with Santos’ Cooper Basin supplies to minimise pipeline tariffs on the South West Qld (SWQ) pipeline (APA is quoting $1.17/GJ for firm capacity on the pipeline). In total these agreements equate to ~100 PJ supply from Qld to southern markets over the next 2-3 years. But the volume available for gas swaps from here is limited (< 10 PJ/annum) – future Qld LNG sales will need to ship gas down the SWQ pipeline, incurring higher delivery charges.

GLNG buyers reduce exposure to higher contracted LNG prices

These transactions are win-win for LNG producers, who gain the dual benefit of assisting the domestic market shortfall and reducing the sale of more expensive LNG into an oversupplied global LNG market. For GLNG offtakers Petronas and Kogas, the diversion of gas from contracted LNG into the domestic market provides an opportunity to reduce the cost of LNG procurement. We estimate the recent domestic gas sale could save them up to $36m/annum. Will this be enough to placate the Government and avoid triggering the ADGSM? We still expect a shortfall to be announced.

Gas prices not announced, but expect these were completed at LNG netback

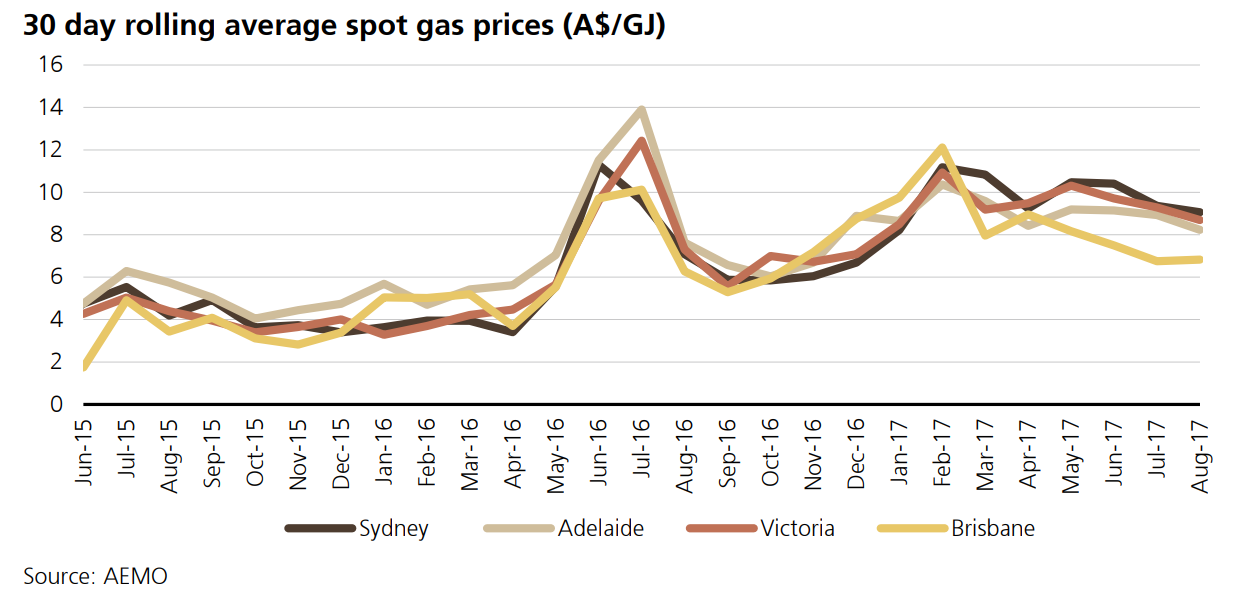

We note the short duration of these gas contracts of up to 3 years. We expect there is some reluctance on behalf of the LNG players to enter into longer term domestic supply agreements, in case LNG prices increase. Domestic gas prices haven’t been disclosed, but with gas buyers reluctant to take oil price risk we expect the gas has been sold exMoomba at $7.50-8.50/GJ, resulting in gas prices in Sydney/Melbourne of between $8.50-$10.20/GJ. So LNG supplies will be supplying gas into the domestic market, just not cheap gas. Direct beneficiaries are incumbent producers (Exxon, Shell, BHP). Indirect beneficiaries include ORG and AGL (higher wholesale electricity and retail gas prices).

The ADGSM still needs to be toughened and lengthened. There’s no security of supply in three year deals. A gas reservation mechanism that only assesses the subsequent year’s market balance has no scope to force longer term contracts.

Moreover, export net-back is only the first port of call for prices. We should be aiming for lower prices still to ensure competitiveness is intact for industry and household’s benefits from the resource endowment is optimised.

US gas prices are a good benchmark. They’re at roughly half our export net-back price.

Advertisement

Remember, to deliver much lower prices we’d only need to reserve 200Pj of gas which is a lousy 4% of planned national export volumes.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.