People flood hands VIC CommSec ponzi economy award

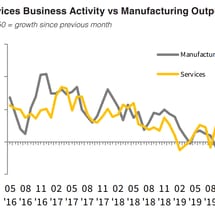

Like Groundhog Day, CommSec has released its latest State of the States report, which again ranks Victoria on top due largely to a combination of strong population growth, construction, and debt-fuelled consumption: How are Australia’s states and territories performing?