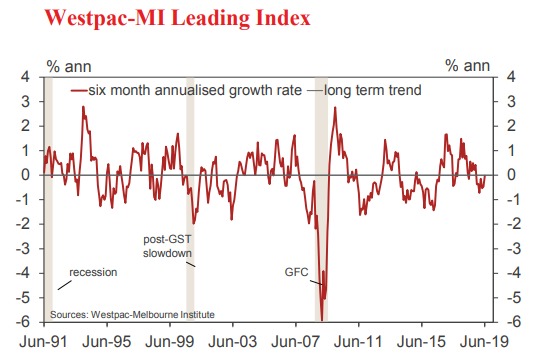

• The six month annualised growth rate in the Westpac– Melbourne Institute Leading Index, which indicates the likely pace of economic activity relative to trend three to nine months into the future, rose from –0.47% in May to –0.02% in June.

These monthly movements can be choppy. Nevertheless the index growth rate remains below trend for a sixth successive month. Over the month, commodity prices; the sharemarket and dwelling approvals explained the improvement. On the other hand these positives were partly offset by deteriorating consumer confidence both overall and in the jobs market in particular.

With this big monthly turnaround, the Leading Index growth rate has lifted over the last six months from –0.36% in January to the current -0.02%. Two components have driven the improvement this year: the S&P/ASX 200 (+0.7ppts), reflecting a sustained rally in the share market (up 17% for the year); and dwelling approvals (+0.4ppts), reflecting a reduced drag from housing as conditions start to stabilise at weak levels.

There has also been support from continued high commodity prices, measured in AUD terms (+0.08ppts); and a widening yield spread (+0.04ppts) as the RBA’s rate cuts have lowered short term interest rates. These positives have been partially offset by bigger drags from US industrial production (–0.39ppts); and domestically from weakening consumer sentiment, the Westpac-MI CSI expectations index (–0.14ppts) and deteriorating labour market expectations, the Westpac-MI UE index (–0.36ppts).

The Reserve Bank Board next meets on August 6. Evidence from the July Board minutes indicates the Bank is likely to pause next month in its current easing cycle. However we do see further easing coming later in the year.

Westpac continues to expect a further 25bp rate cut, coinciding with a downgrade to the Bank’s growth and inflation forecasts in November. By then it will also be clear to the Bank that it has made little progress in its objective of a significant reduction in the unemployment rate.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.