The big four banks have posted interim results (ANZ, NAB, WBC) and updates (CBA) this last week to the market. In this post I intend to articulate the consensus view, analyse and value the banks and provide a contrarian view to why they are likely the most riskiest stocks on the market.

Consensus rules

The banks are indeed making profits of “biblical proportions“, although they pale into comparison to the “twins” BHP and RIO. Their relentless profit growth over the last 10-15 years has captured the views of the mainstream investor, analyst and commentator alike with such lofty rhetoric as “bedrock”, “profit bonanza” amongst the more common “stable”, “steady” and “good dividends”.

Last week’s results reinforced this view, with all banks experiencing growth in profits to record levels, ANZ up 23%, NAB up 16% and WBC up 14%, with CBA on a similar course. Dividend yields continue to be elevated, at approx. 6-7% across the board, with juicy full franking attached. Record profits aside, the market has not treated the banks kindly as they have generally tracked sideways, reflecting the “boring” nature of their business. Price/Earnings Ratios (PER) are also very low by historical standards. (see table below)

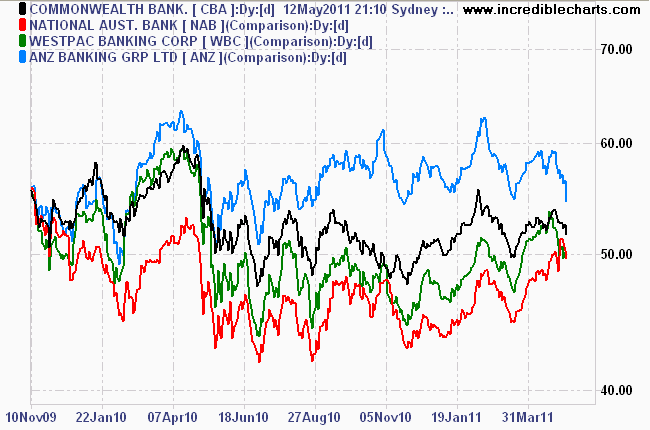

18 month daily price chart of the big four banks

18 month daily price chart of the big four banksValuation

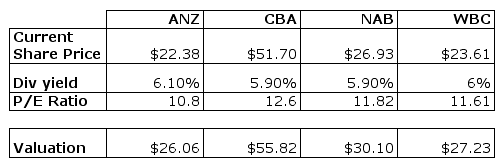

Based on reported earnings, consensus broker forecasts for future earnings and a return to the mean of historical P/E ratios, I have approximated the banks valuations as follows:

Valuations based on consensus earnings and 10 year average PE ratio

Valuations based on consensus earnings and 10 year average PE ratioGiven the discounted share price compared to these valuations, and the strong dividend yield, it would appear to be a no-brainer – something you can bank on. But is there more to it?

A variant view

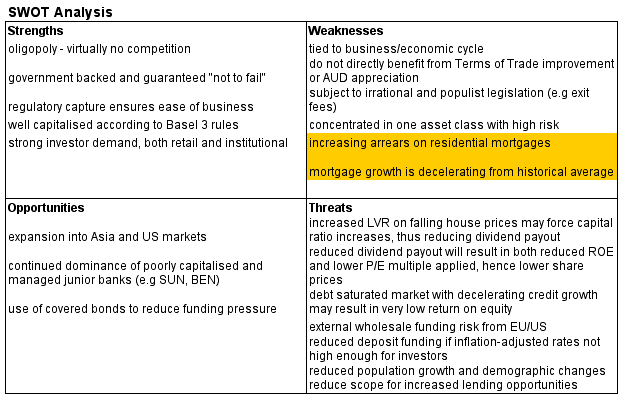

It has always been my contention that when the majority do not question a particular subject, strategy, political view or indeed, the fundamentals behind an asset price, that one should take a closer look and cautious nature. In a previous post, I highlighted how Empire Investing changed our own view on the banks based on the unclear nature of their operations and their unsustainable earnings profile.

The No.1 culprit is the quality metric of unsustainable earnings. This is where the junction of business analysis and macroeconomic analysis for certain sectors pays off.

In particular, the potential for the world’s most indebted households to expand that debt, the lack of potential for increasing the banks assets (i.e their mortgage loan book) and the interaction of macro and microeconomic factors that will weigh on the banking sector for the years and probably decade ahead (including capital/asset ratio rules which effect dividend payout and reinvestment ratios amongst others).

Has this view changed in light of the recent results? In fact, its been reinforced when a much closer look at the balance sheet and the way banks are recording profits is analysed.

Where’s the profit?

Almost half (NAB was the exception – only 20%) of the recent spectacular profit results are due to a reduction in bad and doubtful debt provisions, whilst at the same time, 90 day arrears on residential mortgages are accelerating. So on the one hand, the banks are asking investors to believe that things are so good we don’t need to set aside capital to cover loan losses, whilst on the other hand, their highly concentrated books of residential mortgages are accelerating into arrears – i.e into higher chance of default, and thus increased loan losses.

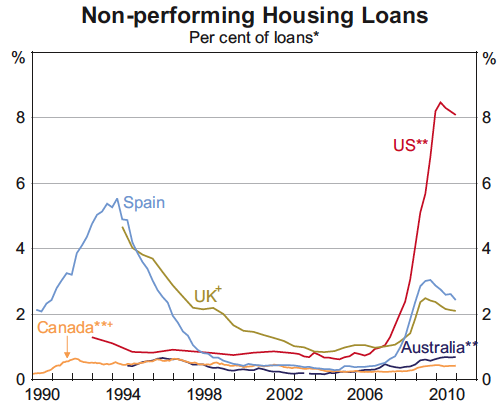

CBA (and its cheap takeover target Bankwest) reported over 11% growth in arrears, whilst ANZ and WBC had almost 25% growth. NAB again stood out with negligible increases. Clearly the banks are nowhere near their overseas counterparts in terms of the percentage of their mortgage book in arrears (see chart below), but in total they now have over $10 billion in mortgages 90 days behind payments.

Even an increase in non-performing loans to UK levels would be severe for the banks.

Even an increase in non-performing loans to UK levels would be severe for the banks.Where’s the credit growth?

Banks bread and butter – through their own design – is a concentrated reliance on residential mortgages. Thus any analysis of any banks earning sustainability is dependent upon the ability of maintaining the current loan book, and to grow that book over time to maintain high Return on Equity.

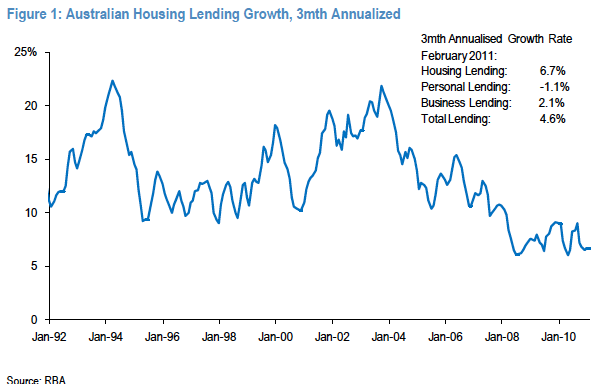

There are two clear barriers in the path to that growth. Mortgage lending has stalled at 6.7% annualised growth – the lowest level in over 30 years.

The latest Fujitsu/JP Morgan Mortgage Industry report forecasts “mid to high single digit growth” over the coming years, a complete change from the gangbuster high teen credit growth. They also point out that any growth above 4% would only be as a result of increased house prices and/or increasing LVR on new lending. This is what happens when you reach over a TRILLION dollars of mortgage debt – exponential growth has limits.

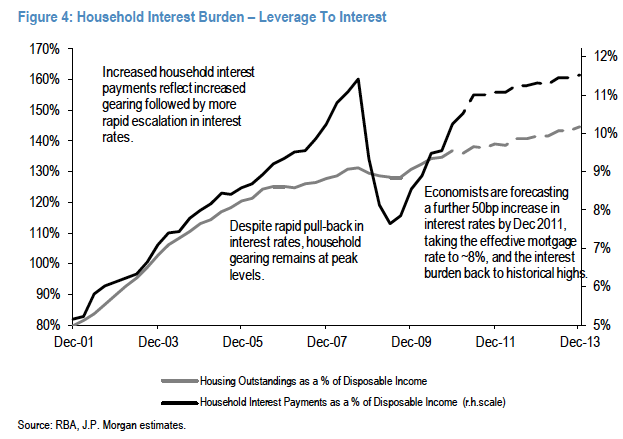

The ability of households to continue to pay the current loan book is facing renewed pressure as the bullhawks and consensus crowd push for higher interest rates. Although at very low inflation adjusted levels, First Home Buyers in particular are extremely sensitive to interest rate rises. As the chart below illustrates, even a small 50 bps rise in rates will put serviceability back to the heights of the 2008 near-recession.

Bring on the interest rate rises property bullhawks….

Bring on the interest rate rises property bullhawks….Fujitsu/JP Morgan highlights that the same amount of disposable income is being used to service mortgages at a rate of 7.8% compared to rates of 8.5% in late 2007. This is due to the very large increase in mortgage debt over this time period, even though growth rates itself decelerated.

The sustainability of high earnings is completely in question, whilst the probability of negative earnings growth is rising as households struggle to pay existing debts and mortgage growth stagnates. It is clear that the banks will not be able to substantially increase earnings past current levels, with earnings growth likely to be in the 2-4% range at best, not the 8-10% consensus forecast range.

What about business lending?

A much repeated theme is Australia is undergoing a private investment boom – so is this reflected in increased business lending by the banks? Can they switch their reliance upon residential mortgages to take advantage of this boom? Both current results and historical performance in this area – whereby banks can actually have a positive role in increasing wealth and productivity for the broader economy – show a lack of evidence.

ANZ has not improved business lending above GDP growth in over 12 months, although they forecast NZ business lending is likely to improve post-earthquake. CBA claims to have experienced some growth in business lending over the quarter, but are experiencing difficulties in commercial property lending and SME lending volumes. WBC also experienced flat business lending, reducing exposure to commercial property, and experienced slowdowns in their NZ division.

NAB Business lending, although flat over the last year, has seen an increase in revenue, net interest margin and market share in this area. Amongst the big four, it is best setup to take advantage, whilst having the lowest exposure to residential mortgages, although it is growing the latter at substantially higher rates than business lending.

As and Small/Medium Enterprise (SME) would know, dealing with any of the four banks with regard to business lending is wholly dependent on existing equity values in residential property as collateral, not based on cashflow or the business case. Commercial property developers are facing similar (or even harsher) restrictions on lending, with smaller LVR’s and tighter controls on cashflow required. Although NAB and ANZ may have a case for a better focus on business lending compared to the others, all are caught up in this paradigm. The stark fact is most of private investment boom is likely to be funded by cashflow from the mining companies.

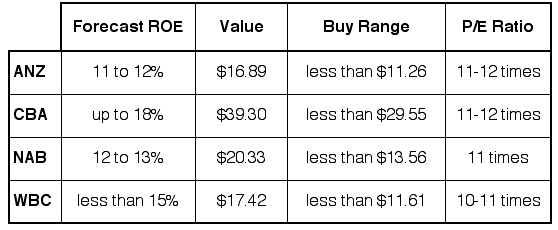

What are they really worth?

Given the weaknesses and potential threats to the banks businesses, and the likelihood of reduced earnings, here’s where we stand with our analysis:

Based on this variant view of the banks, here are our valuations, with some slight changes from March of this year:

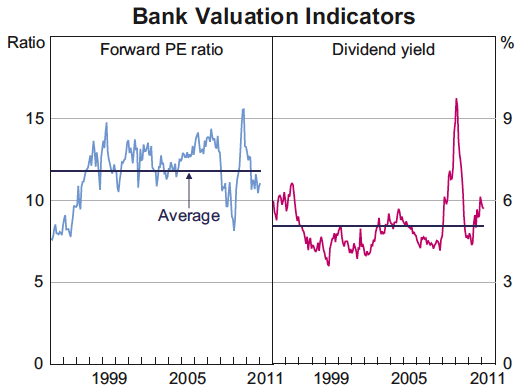

For those of you who think that banks share prices could never go down to 10 or sub-10 P/E ratios (ANZ is already at 10.8 yesterday), or dividend yields in the 3-4% range? Do any of you remember the last recession in the early 1990’s?

Notice the left hand side of the chart – low yields, low PE.

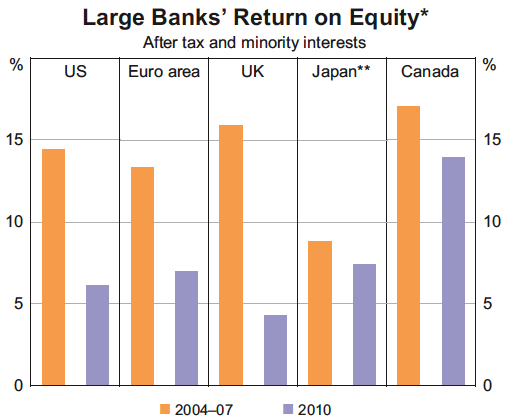

Notice the left hand side of the chart – low yields, low PE.Or what about Return on Equity measures in the low teen, high single digits? What happened to every major overseas bank during the Great Recession?

Why so ROE? Increased capital ratio, reduced (zero) lending growth.

Why so ROE? Increased capital ratio, reduced (zero) lending growth.What would trigger a change to the consensus?

What event or situation would trigger a change from the consensus to this variant view, and precipitate a new range of share prices for the big four banks? In our view its likely to be one of the following:

- Increase (reversal) in unemployment,

- Substantial increase in arrears that require reversal in debt provisions,

- 50-100bps rise in RBA rates that are passed on by the banks,

- Continued reduction in immigration and continued increase in permanent migration, combined with reduced housing construction

- Annualised mortgage growth drops to 4% or below

- Any of the banks report reduced earnings for the quarter

Disclosure: The author is a Director of a private investment company (Empire Investing Pty Ltd), which has no interest in any business mentioned in this article. The article is not to be taken as investment advice and the views expressed are opinions only. Readers should seek advice from someone who claims to be qualified before considering allocating capital in any investment.