ANZ released its first-half update today. Below is a brief summary of some of the key figures along with graphs taken from the presentation.

Profit

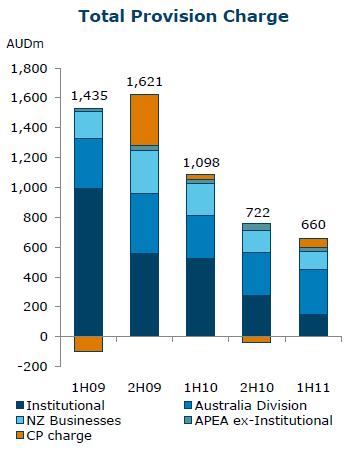

Up 23% compared to 1HY10 results, however revenue is down whilst expenses are up. It seems a 40% reduction in provisions for the same period has contributed the lions share to the improved NPAT (see the provisions graph below).

Revenue from Asia Pacific, America and Europe (APEA) are on the increase as ANZ purses its off-shore expansion plans. At the moment, 70% of ANZ’s revenue comes from Australia, 15% from New Zealand and 15% from APEA.

Net Interest Margin

NIM contracted slightly over the last 6 months (249.7 to 247.2), due in part to the increased costs of a competitive deposit market.

Lending

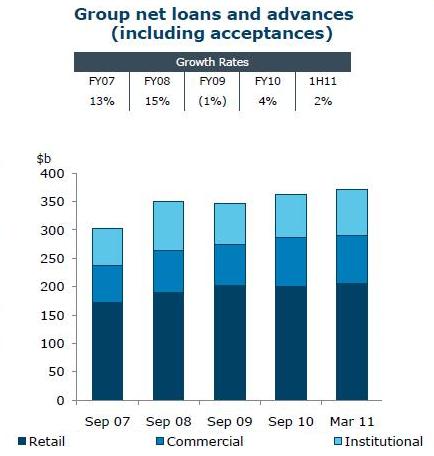

Loans are up 7% on 1HFY10 and 2% over the last 6 months, however as you can see from the graphs below retail loans are flat.

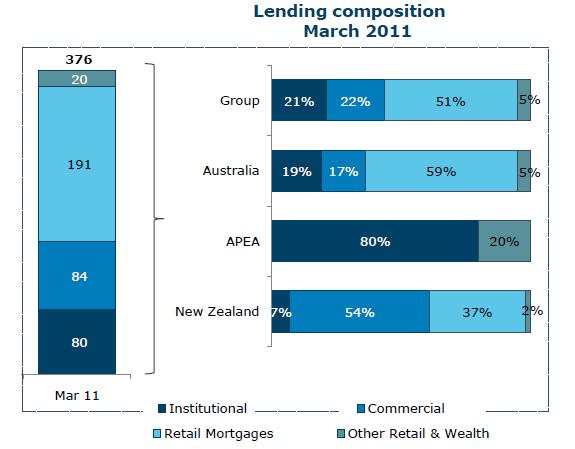

Lending composition by geography is shown below.

Funding

ANZ seems to have learnt from the GFC, with customer funding now accounting for 60% of funds whilst short-term wholesale funding has reduced to 11%. By comparison, in 2008 the two figures were 50% and 22% respectively. Obviously ANZ is moving to a lower-risk profile.

A point which caught my attention was the poor performance of regional commercial loans. They have been highlighted as a risk due to “long-term” stress and extreme weather events, although cyclone Yasi has not been factored in yet. Regional deposits were up 12% whilst lending is down 3%, meaning HOH revenue was down 1%. This deleveraging probably indicates regional businesses are not overly optimistic about future conditions.

Summary

So, deposit funding composition is on the increase, but this is putting pressure on NIM due to the increased competition for deposits. People and businesses are saving more whilst lending growth is slowing – familiar themes to readers at MacroBusiness. The regional banking results are further indication that things outside of mining aren’t too rosy.

From a patriotic viewpoint, it’s good to see ANZ pursuing growth offshore. However, Australian banks don’t have the best form at competing outside the home market, so we’ll wait to see how that pans out.

Overall the result appears to be a decent one, although increasing costs have been masked by a decrease in provisions for bad credit. ANZ still depends on Australian mortgages for a lot of revenue (although less than CBA and WBC) so any housing correction will have a significant impact. From a long-term viewpoint, ANZ is my pick of the big 4 banks because of its current international push. However, Empire still considers it non-investment grade due to it’s Aussie mortgage exposure.

The Prince will be publishing a more in-depth article on the banks soon, so stay tuned to the MB channel.

Disclosure: The author is a Director of a private investment company (Empire Investing Pty Ltd), which has no interest in any business mentioned in this article. The article is not to be taken as investment advice and the views expressed are opinions only. Readers should seek advice from someone who claims to be qualified before considering allocating capital in any investment.