Note: This is part 1 of a 2-part series on trading and valuing the big four Australian banks. Part 2 shall be forthcoming soon.

Fellow equities blogger Sell on News completed an excellent thematic post on the bubble like growth of the finance industry recently. In the face of a likely change in how capital is costed, he rightly suggests:

So what does this mean for investment? A probable long term portfolio shift from finance stocks to what will be increasingly scarce resources (even water) food and energy. Manufacturing has been globalised, which has destroyed margins. And the era of debt driven speculation is not looking good, so the financial sector may find their conventional forms of theft a little more challenging.

Back in May 2010, my business partner (Q Continuum) and I re-evaluated our position on the banking industry.

Now, we are not economists and do not use top-down macro-economic analysis to quantitatively value a company. However we do lean heavily on the first class analysis provided at MacroBusiness to give us a qualitative macro perspective.

We are first and foremost business analysts, then behavioural analysts i.e first, what is the value then what is the price people are prepared to pay?

So our questions back then were:

- Are these businesses sustainable?

- Do they have any pricing power?

- What are the inherent risks of owning a bank stock?

- Will the market re-value banks in light of this?

Good, but only just

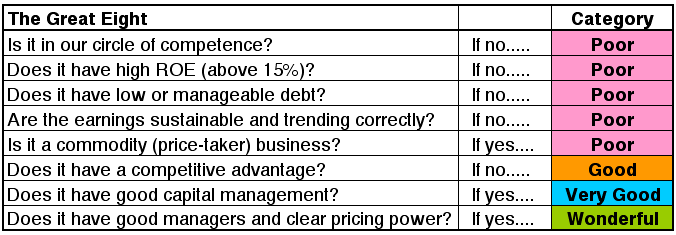

Up to May last year, we had all four major banks listed and categorised as “Good, No Competitive Advantage”. A little explanation of our “Quality Ladder” – or how we categorise a company – is in order here before moving on.

A+, High Achievement, Competent and Poor

We contend that there are four “grades” of businesses, based on quality and then quantitative metrics. We use a Quality Ladder to filter out the diamonds from the crud, as shown below:

At that time, we considered the big four banks as having good businesses, sufficient and stable Return on Equity (ROE), modest uncertainty and risk exposure but no competitive advantage, although Commonwealth Bank had the edge in terms of its very cheap BankWest takeover and much higher ROE. During the GFC, the Stevens Put and Federal deposit guarantee gave the big four a major edge over their weaker regional and small bank competitors in terms of wholesale funding, brand domination and reach. A very pliable government (and opposition) and media rounded out the oligopolistic package.

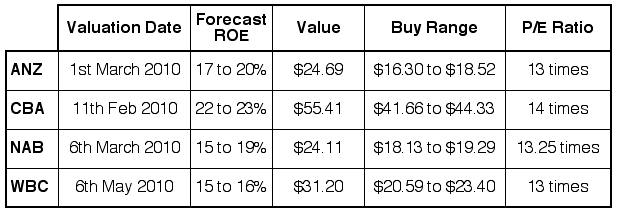

Our valuations up to that point were as follows:

pre-May 2010 "Big Four" valuations

An Unsustainable Change of Mind

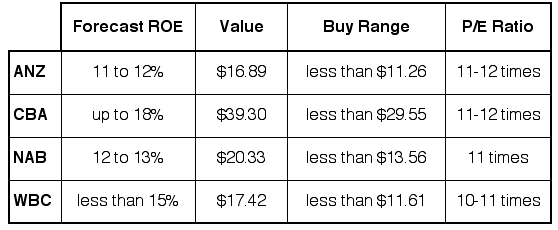

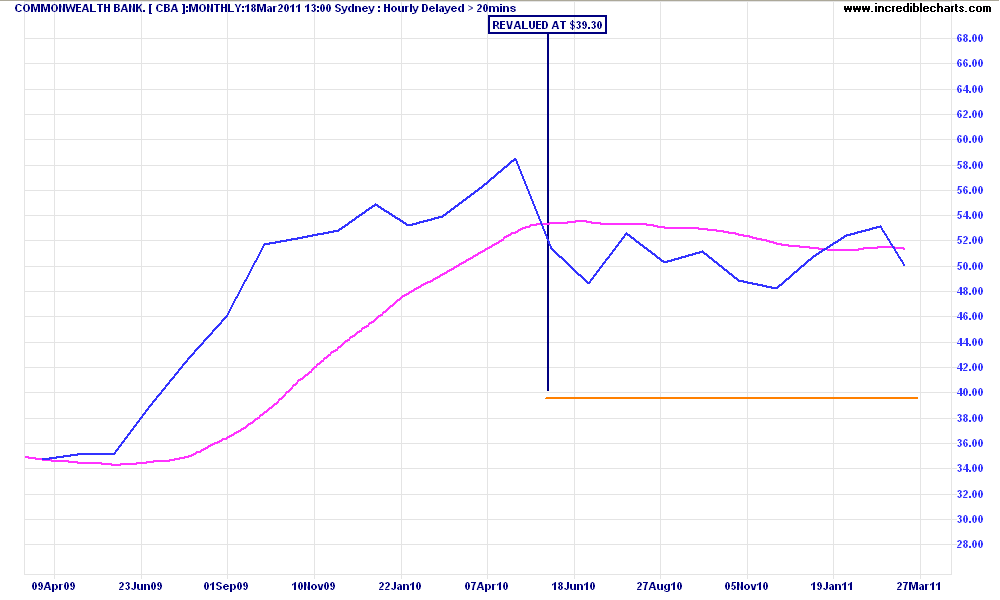

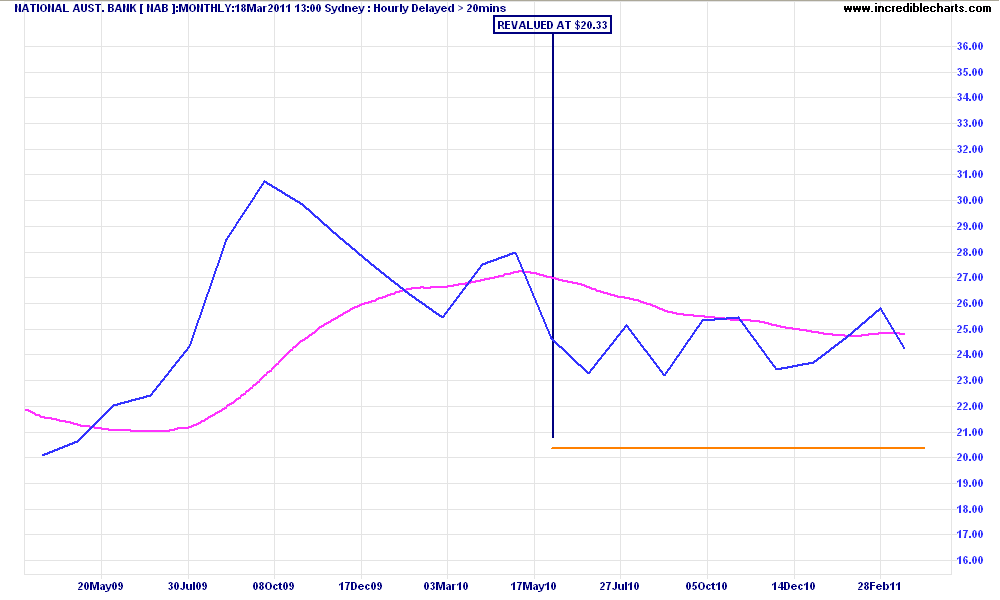

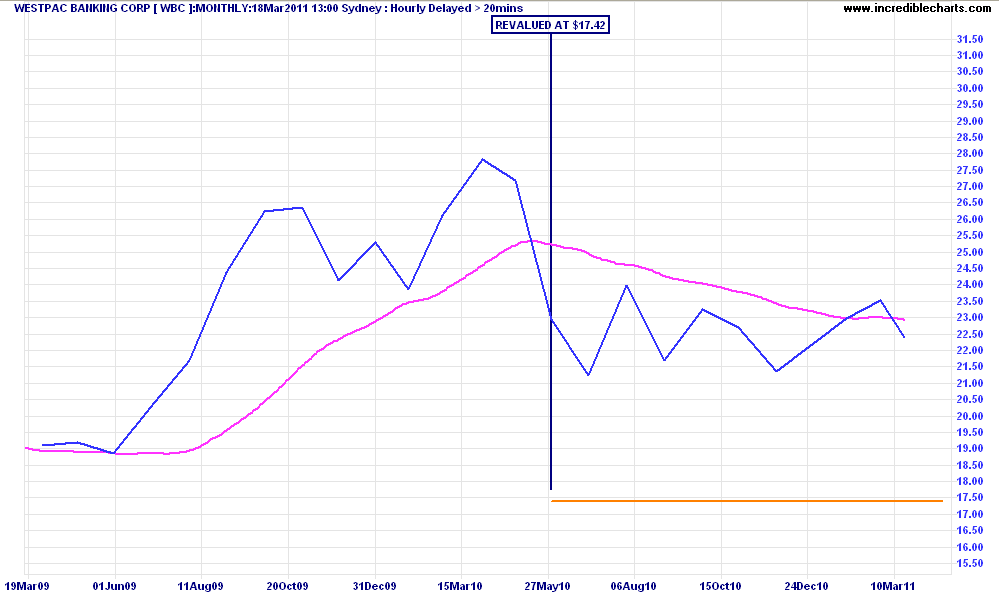

So what happened? Why did we then change (and maintain) our valuations to this:

Post May 2010 Valuations

The No.1 culprit is the quality metric of unsustainable earnings. This is where the junction of business analysis and macroeconomic analysis for certain sectors pays off.

This post will not go into the specifics of how we determined that the banks earning capacity was not sustainable. Truth be known, it was the superb analysis (and prediction) of the GFC by Prof. Steve Keen, and then the work of the The Unconventional Economist and Delusional Economics that pushed us in that direction.

In particular, the potential for the world’s most indebted households to expand that debt, the lack of potential for increasing the banks assets (i.e their mortgage loan book) and the interaction of macro and microeconomic factors that will weigh on the banking sector for the years and probably decade ahead (including capital/asset ratio rules which effect dividend payout and reinvestment ratios amongst others).

For a prescient (yep, back in May 2010 when house prices stopped going up) analysis, go here, here and here.

Sustainability is important for Business and the environment

Determining the sustainability of earnings of a business is crucial in estimating its future value. From this you can derive an estimation of future equity per share and a multiple thereof, eventually working out how much a business is worth now, and how much the market is prepared to pay.

For any investor, the best businesses to invest in are those with stable, robust (i.e to external (economic/non-systematic) and internal (management) risks) and if possible, growing earnings (at a minimum, keeping up with inflation).

Eliminating those businesses whose earnings capability is compromised – in this case by the concentration of assets in the worlds largest housing bubble – substantially reduces the investor’s risk to a loss of capital (either real or opportunity cost).

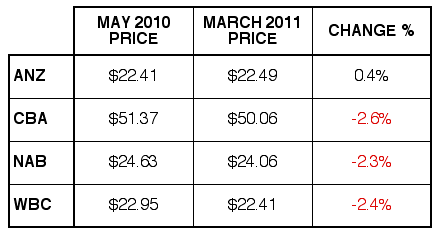

How have our valuations panned out?

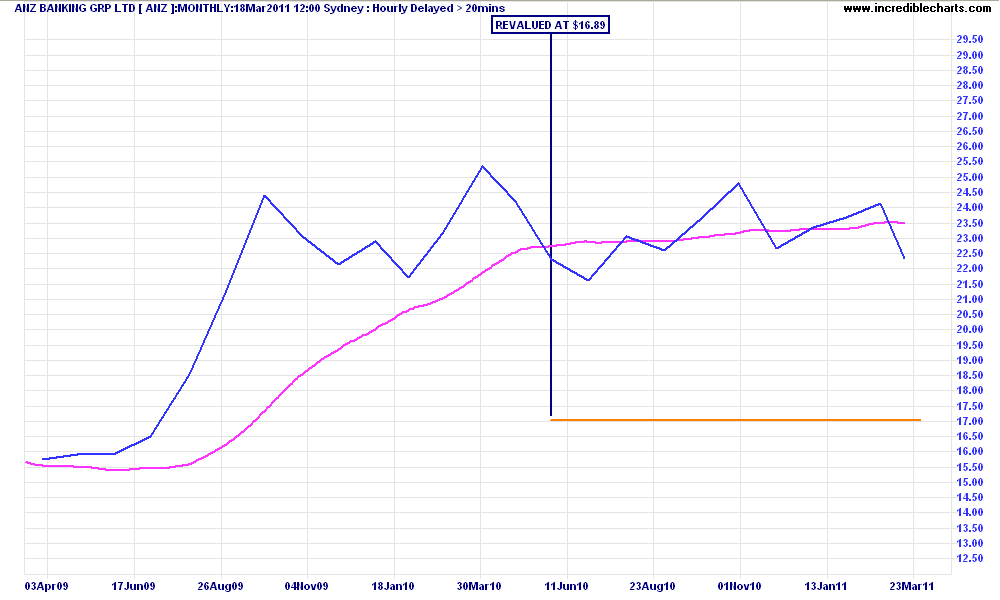

Since May 2010, the big four banks have done the following:

ANZ up 0.4%

CBA down 2.6%

NAB down 2.3%

WBC down 2.4%

Summary of Results

Although none of the banks have dropped to our new valuation range (which for comparison are in the same price range after the rebound rally in April to June 2009), they have not appreciated as some have expected.

As a result, we still consider them considerably overvalued, which leads one to question – even after the large correction in world markets this week – is there any further downside to the banks, and how can an investor/trader profit in the short and long term?

In Part 2 of this series, I will explore some techniques for trading the Big 4 banks.

Please note that Empire Investing may have or is considering future positions in any or all the companies mentioned above. This post is general information only and not a recommendation.