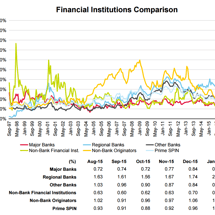

APRA soothes on mortgage risks

By Leith van Onselen Heidi Richards, APRA’s General Manager of Industry Analysis, has delivered a speech today entitled A Prudential Approach to Mortgage Lending, which delves into Authorised Deposit-Taking Institution’s (ADIs) mortgage lending and finds that Australia’s ADI’s have significantly improved their risk management practices.