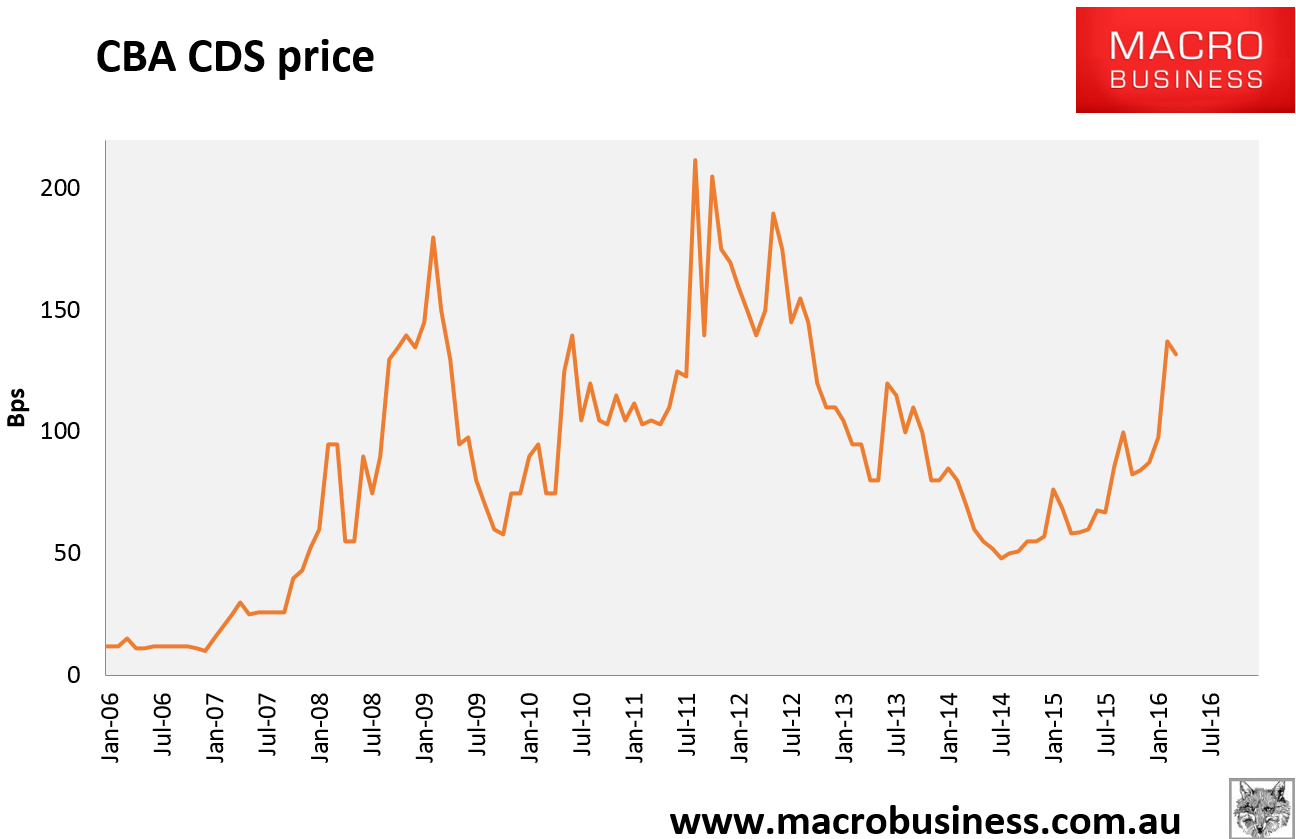

It’s the fly in the ointment that just won’t go away. Despite the iron ore rally, rampant RBA barracking, above trend GDP, wall-to-wall bullish triumphalism and the big move in for global credit spreads, the CBA CDS price just does not want to fall. In fact, yesterday it rose 2 points to 132bps and is threatening to break above its recent 137bps closing high:

I could be wrong but it seems to me that the recent Variant Perception report on Australian housing appears to have sparked some very serious soul-searching in markets about the sustainability of the Australian business model. FTAlphaville captures the mood:

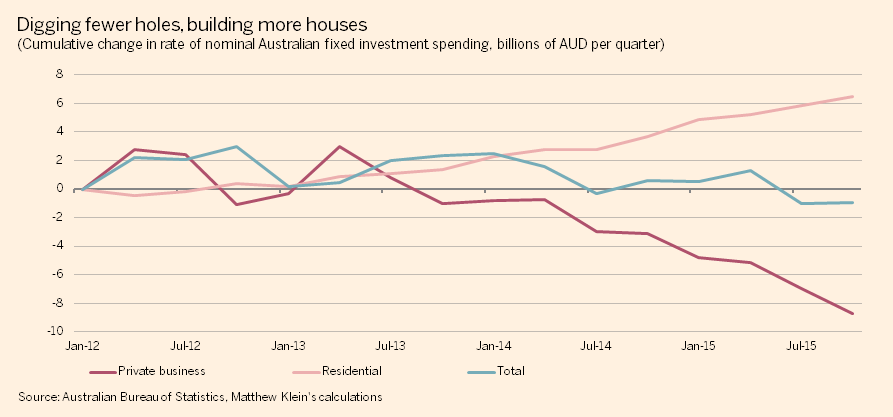

The boom in nominal residential construction has almost completely offset the collapse, so far, in mining capex:

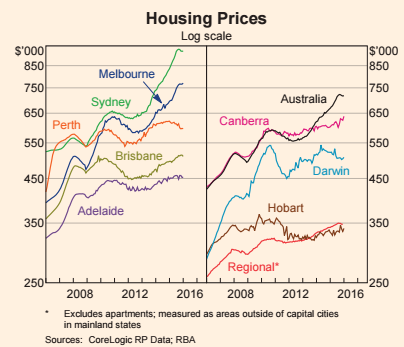

It’s reasonable to worry about this. After all, Australia’s housing market features mortgage debts at record highs relative to incomes, a rising share of mortgages going to investors rather than owner-occupiers, and bubbly prices. Homes in Sydney have soared more than 50 per cent in value just since 2012, for example, while prices across the country are up about a third over the same period:

Even economists at the RBA, who are generally sanguine about the prospects for house prices admit current valuations only make sense relative to rents if you expect house prices to keep rising at least 2.4 per cent per year above inflation, forever.

On the other hand, at least some of the bubbliness in prices, and the associated surge in lending to people to buy investment properties, can probably be attributed to underbuilding in the past, relative to robust population growth. The recent boom in building looks impressive, but as you saw higher up, the longer-term trend of real investment in residential construction has been quite weak.

Nominal spending on homebuilding had steadily trended down from about 6.5 per cent of total output in 2004 to just 4.5 per cent by mid-2012. Since then it has recovered to roughly the long-term average of 5.5 per cent.

The coming boom of “higher-density housing” supply could help moderate price increases in the cities most in need of boosting affordability. Soaring prices across the country are a signal to increase supply, and the markets are (finally) working.

The danger comes from the lag time between the decision to build more housing and the moment the extra space actually becomes available to live in. Worryingly, a close look at Australian house prices suggests they may have already peaked, which suggests historically bad timing for all those new building approvals.

The obvious analogy is with the commodity industry, which should be particularly poignant for Australians. The standard cycle goes something like this:

Prices start going up, maybe because traders think there won’t be enough supply to satisfy future demand

(Some) existing production starts becoming more profitable

Investors respond by encouraging more capacity

Businesses invest in new supply

There is a lag, so you have a period when prices keep indicating new supply will be profitable to produce, but the extra production hasn’t started yet, which leads to more investment

A whole bunch of new supply shows up at the same time

Prices go back down

Production looks less profitable than before

New investment plans get cut

Time passes, then go back to step 1

It doesn’t take a particularly robust imagination to think something similar could happen to Australian housing markets, especially given the magnitude of the boom in prices. The tight housing market and ridiculously high prices may have even been good for growth (at least in the short-to-medium term) by bolstering household balance sheets, helping the country avoid the fate of more flexible markets such as Ireland, Spain, and the United States.

Advertisement

It’s too early judge whether we’re past some kind of tipping point but the stickiness of high major bank CDS prices suggest it is a live concern.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.