In a February briefing Macquarie revealed that since Brazil established his new group, Corporate and Asset Finance (CAF), in 2009 the bank had invested an astonishing $33 billion in around 500 high yield loan exposures (including $1 billion into equity-like risks) across North America, Europe and Australia.

CAF’s contributions to Macquarie’s divisional operating profits have exploded from just $66 million in 2010 to $1.1 billion in 2015, which was 27 per cent of Macquarie’s total.

…by May 2009 Macquarie had raised more government backed funding than any other Australian bank. There was an urgent need to start generating returns to cover the cost of this capital.

Macquarie’s solution was an extreme version of the “carry trade”. Use Macquarie’s A rated banking licence to tap vast volumes of cheap money and then re-invest it in ultra high-yielding bonds and loans that don’t need to be “marked-to-market”. Since the high-yield (and sometimes distressed) debt Macquarie originated itself or bought off investors in secondary markets is accounted for on a “hold-to-maturity” basis, and not revalued regularly as a “trading” book, the assets have effectively zero volatility on Macquarie’s balance-sheet.

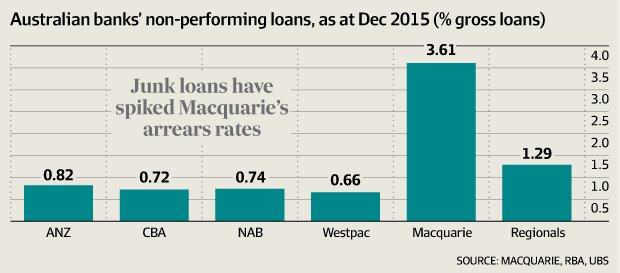

The only time risk is publicly recognised is when loans go into arrears—which is why Macquarie’s Pillar 3 reports look so troubling…

“Macquarie’s asset quality continues to slip at a disturbing rate,” [UBS’ Jonathon] Mott wrote. “Given the ongoing volatility in global credit markets, Macquarie’s higher risk tolerance, and exposure to oil and gas financing, we would not be surprised to see its asset quality deteriorate further.”

This hold-to-maturity accounting enabled Macquarie to avoid the huge spike in high yield spreads in 2015 and 2016, which inflicted searing losses on asset managers that have to revalue their investments regularly at market prices. What Macquarie has not been able to skirt is the ugly non-performing loan story.

This is maturity transformation stuffed full of nitro-glycerin, trussed in plastique, then sunk into a drum of rocket fuel and left in the sun.

Let me be clear that I don’t care if Macquarie wants to do this with its own money and perhaps it does have the expertise to manage the risks. But this is not what government guaranteed money should be doing (even if at this stage those guarantees have been refinanced away and reverted to being implicit). Joye returns with a second article today asking that question as well:

Advertisement

In its February briefing Macquarie reported that the Corporate and Asset Finance unit, which includes a $29.6 billion asset finance team and the high-yield lending unit that manages $10 billion, was funded with $4.1 billion in capital. Last year the division contributed $1.1 billion in pre-tax and pre-bonus profits, or 27 per cent of Macquarie’s overall profits, up from $66 million contribution in 2010.

The Future Fund’s former managing director, Mark Burgess, asked “what price the government guarantee today knowing how it is invested” in response to the article. Mr Burgess questioned whether “the implied [government] guarantee [of banks] remains?”

Macquarie’s banking subsidiary and the four major banks receive a higher credit rating on the assumption they will receive “extraordinary government support” in a crisis.

Standard & Poor’s says without this support Macquarie Bank would only be rated BBB+, less than Bendigo & Adelaide Bank and Bank of Queensland, which are both rated A-.

Because it is treated as being “too big to fail”, Macquarie Bank’s rating gets boosted to “A”. Higher credit ratings are associated with lower funding costs.

To summarise, Australia has a globe-trotting, too-big-to-fail, hot money hedge fund buried inside an implicitly government guaranteed liability flow and banking licence being misused to dodge regulatory rules that prevent excessive risk-taking via mark-to-market. Not only that, it has gambled in the assets that are at the epicentre of the Mining GFC.

This is the same integrated trading and commercial bank model that destroyed the US financial system in the GFC and has since been steadily unwound by the Volcker Rule and Dodd-Frank legislation which is still being rolled out.

Advertisement

There is no price high enough for the guarantee of this. Either the hedge fund is wound up or the guarantee openly and irrevocably stripped.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.