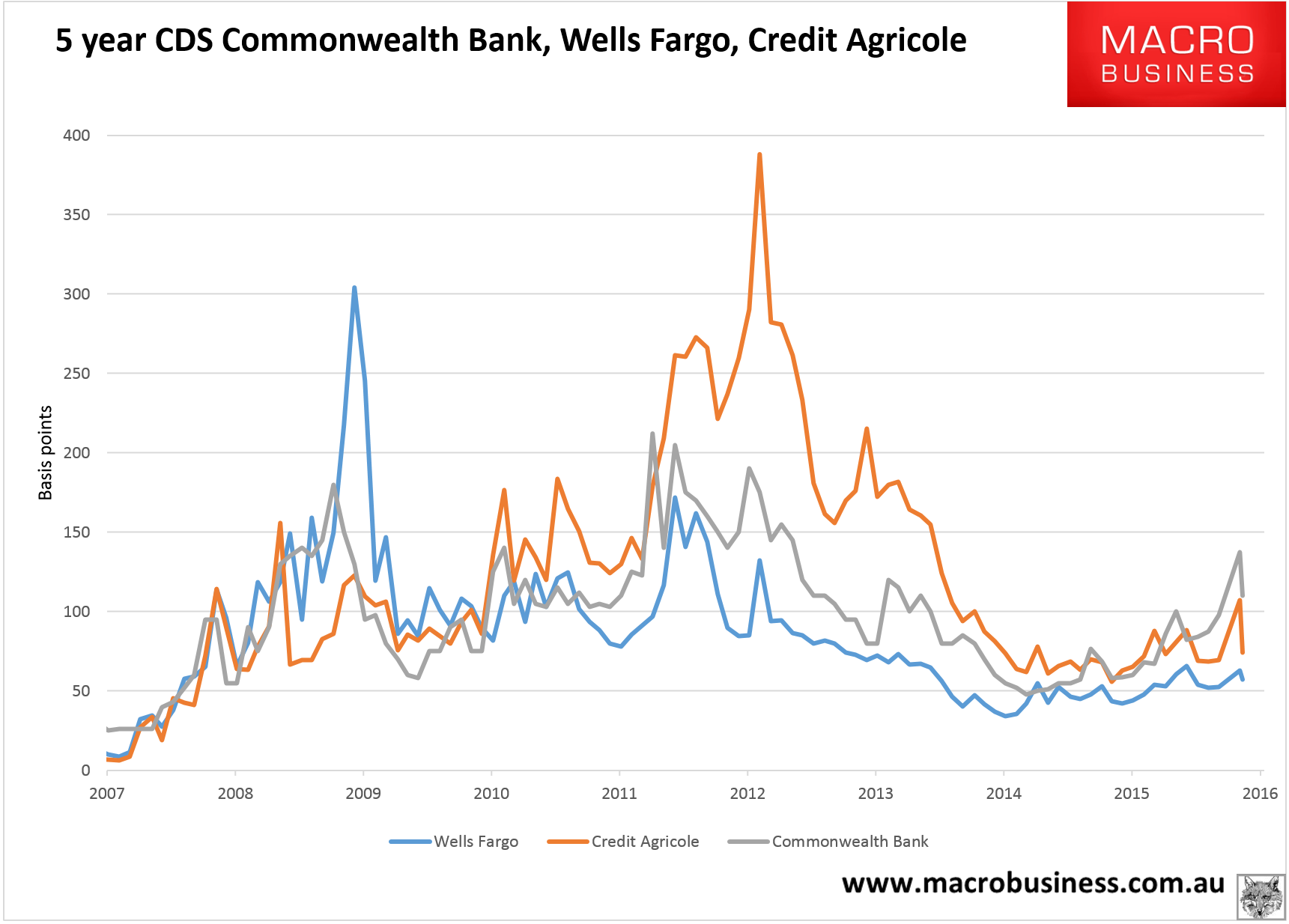

The CBA CDS price is finally demonstrating the easing I’ve been expecting for some weeks down four points from my last update to 110bps. Comparable banks Wells Fargo and Credit Agricole have actually seen a little widening in the same period:

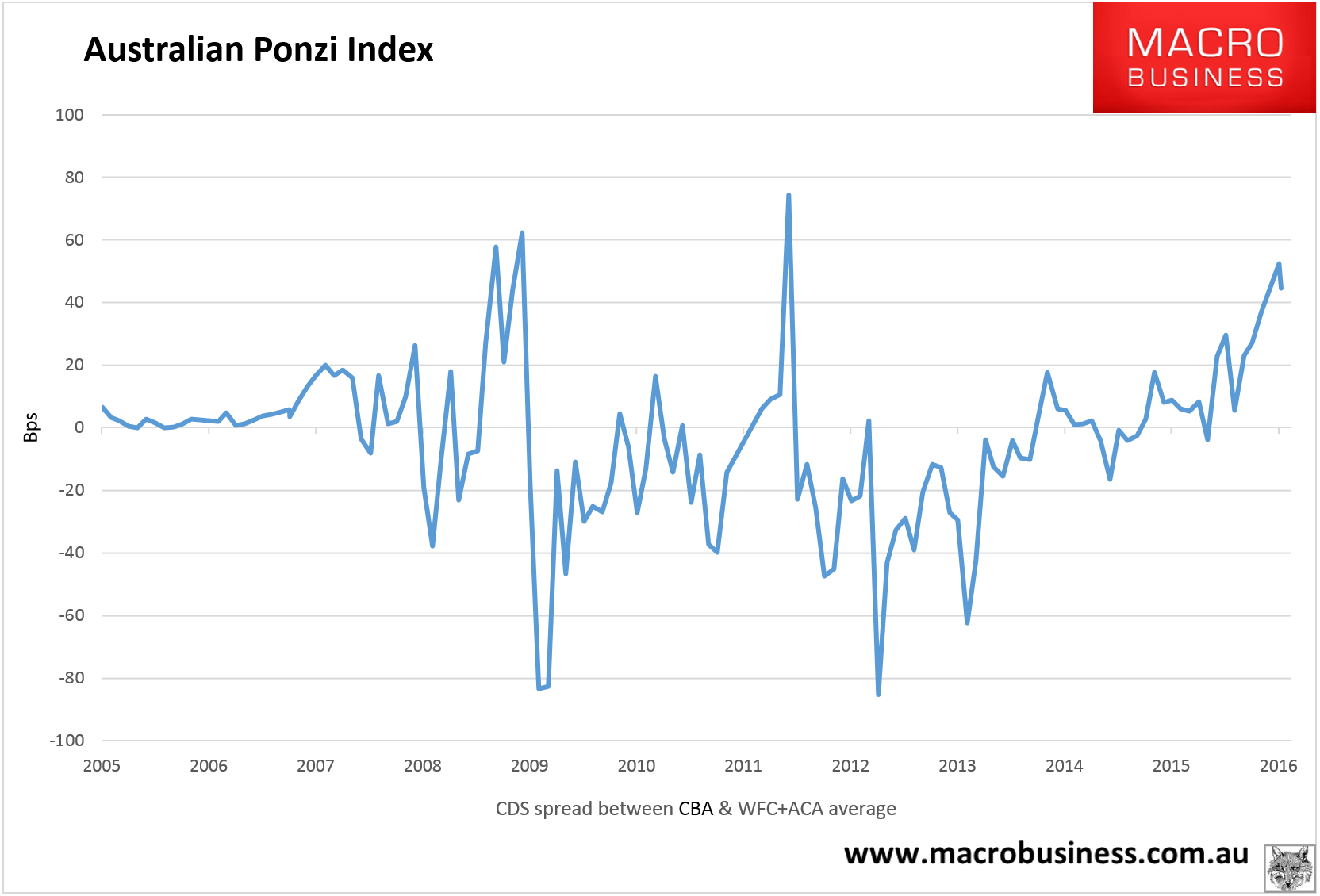

Thus the Australian Ponzi Index has fallen back a little further from its recent peak:

Advertisement

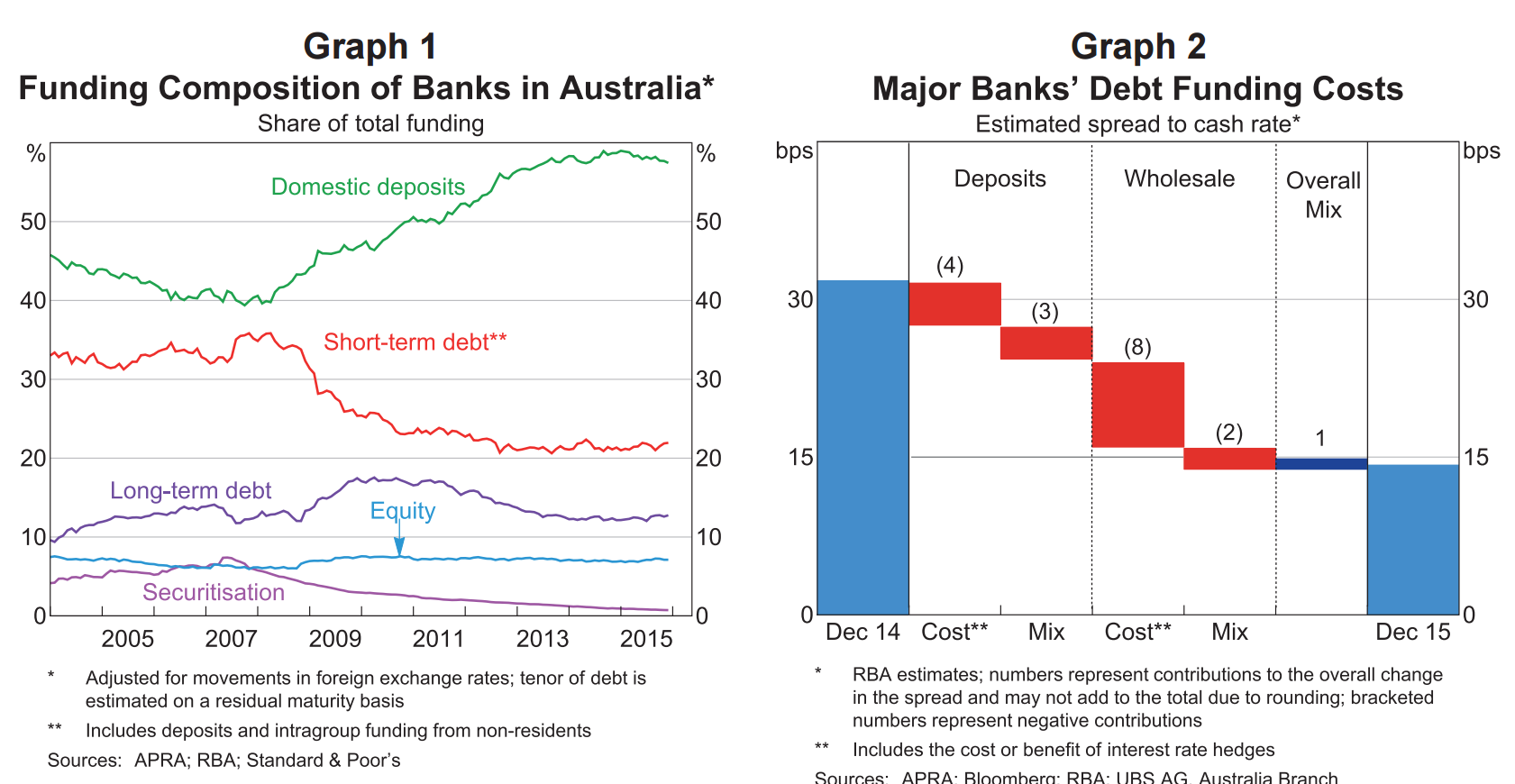

The RBA has produced some good new material on the ponzi:

In aggregate, debt funding costs (hereafter ‘funding costs’) for the major banks are estimated to have fallen by around 70 basis points over 2015, partly reflecting a reduction in the cash rate of 25 basis points in February and then again in May. The spread of major banks’ funding costs to the cash rate is estimated to have narrowed over 2015 owing to the fact that both deposit rates and wholesale funding costs declined by more than the cash rate in the year (Graph 2). Compositional shifts within the mix of deposits and wholesale funding also contributed to the narrowing in the spread. Much of the fall in funding costs relative to the cash rate occurred over the first half of 2015, with major banks’ outstanding funding costs estimated to have been relatively stable over the second half of the year. Notwithstanding these developments, the spread of major banks’ funding costs to the cash rate remains higher than it was in the period before the global financial crisis.

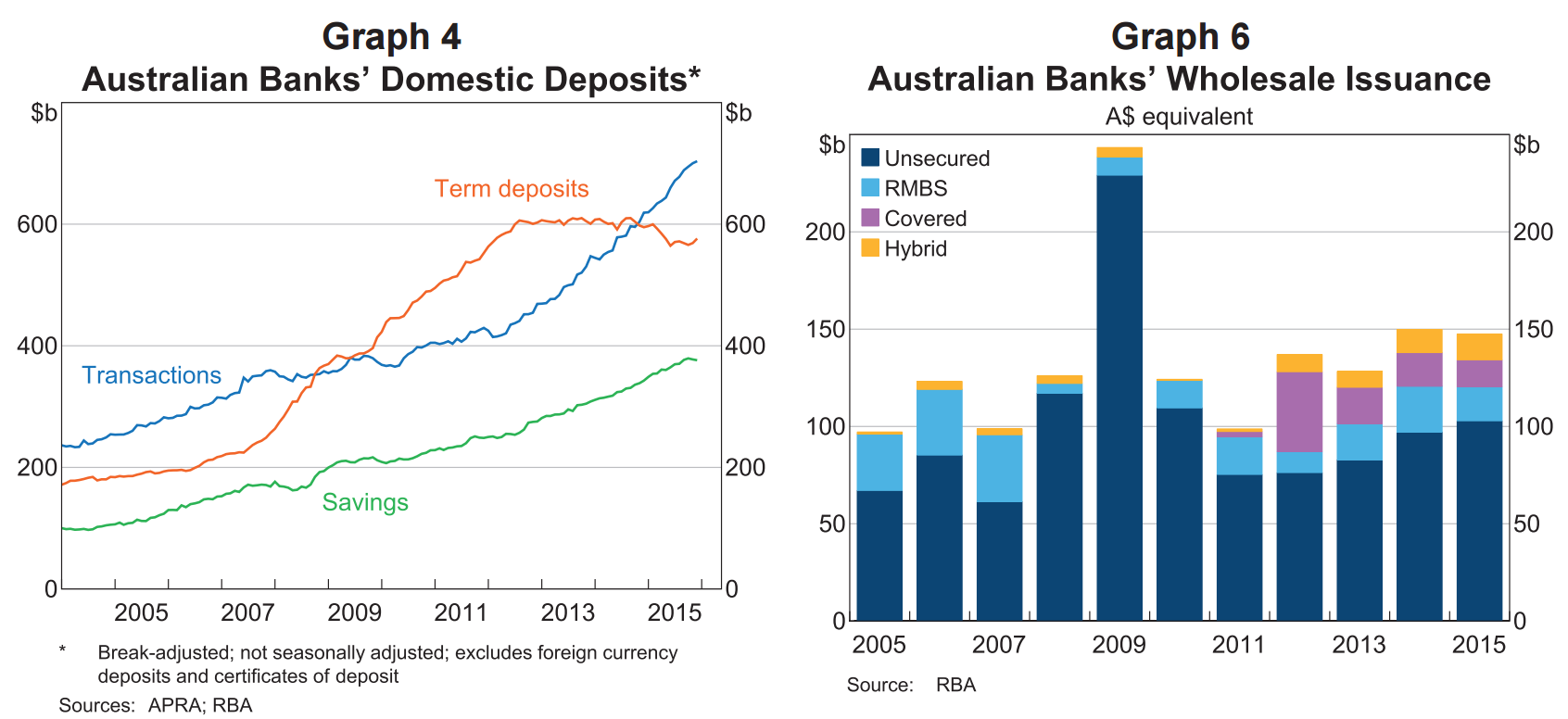

…The volume of bank bond issuance in 2015 was broadly similar to the previous year, although banks issued slightly less in covered bonds and residential mortgage-backed securities (RMBS) (Graph 6). Issuance of hybrid securities (hybrids) has steadily increased since 2012, and banks’ hybrid issuance was slightly higher in 2015 than the previous year, possibly reflecting proposed international prudential standards which call for a higher share of such funding. The mix of wholesale funding outstanding was little changed over the year. A shift from offshore long-term debt to offshore short-term debt contributed to a marginal reduction in funding costs for the major banks (Graph 7).1 However, the share of major banks’ total funding from offshore short-term debt remains below that for the banking sector as a whole, reflecting the fact that some other institutions, particularly foreign banks, make more extensive use of such funding (Graph 8). During 2015, declines in wholesale funding rates and the roll over of existing higher-rate funding lowered the major banks’ funding costs by 8 basis points more than the reduction in the cash rate. Yields on major banks’ senior unsecured debt largely moved in line with sovereign and swap rates, and yields in 2015 were on average lower than in the previous year (Graph 9).

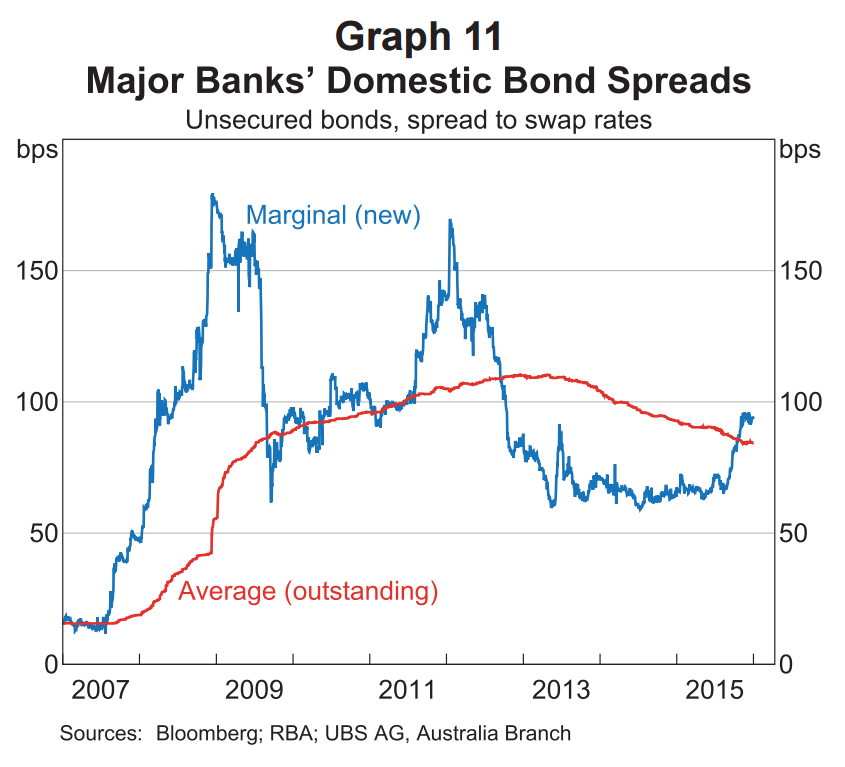

The modest widening in spreads on bank debt to Australian Government securities (AGS) and swap rates towards the end of the year was associated with perceptions of increased global macroeconomic risks and a rise in the cost of funding in other markets, particularly in US dollars. The all-up cost to banks of issuing new wholesale debt fell substantially at the beginning of 2015. The lower level was sustained through most of the year. This gradually flowed through to outstanding wholesale funding costs as the new cheaper debt replaced higher cost maturing funding (Graph 10). Graph 7 Graph 8 Graph 9 Graph 10 Towards the end of 2015, the cost of issuing new debt increased. Yields on new short-term debt rose to be higher than those on outstanding short-term debt, while the cost of new long-term debt was a little below the cost of corresponding outstanding debt. One component of the cost of long-term debt is the spread which banks pay above the swap rate (interest rate swaps are used to convert fixed rate debt into floating rate debt). The estimated spread to the swap rate on new issuance in the domestic market rose to be slightly above the average of outstanding issuance, which suggests that there is some upward pressure on funding costs once the cost of hedging is taken into account (Graph 11).

The spread widening is not so “modest” now and, if sustained, it will damage net interest margins. As always, the RBA driving using the rear vision mirror…

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.