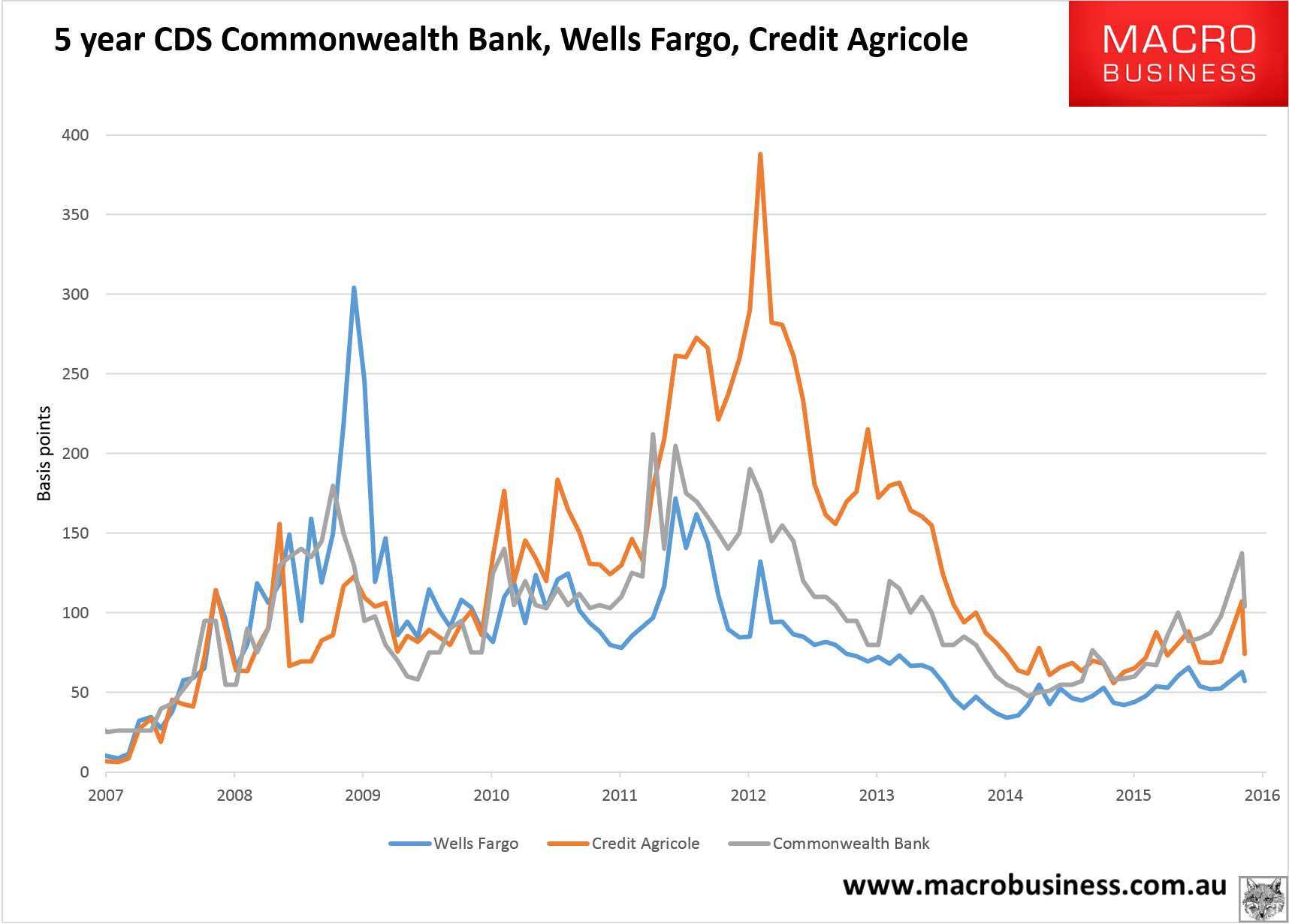

Some more relief for Australian bank funding costs Friday, as expected. As global credit spreads also come in, CBA saw its CDS price tumble six points to 104bps:

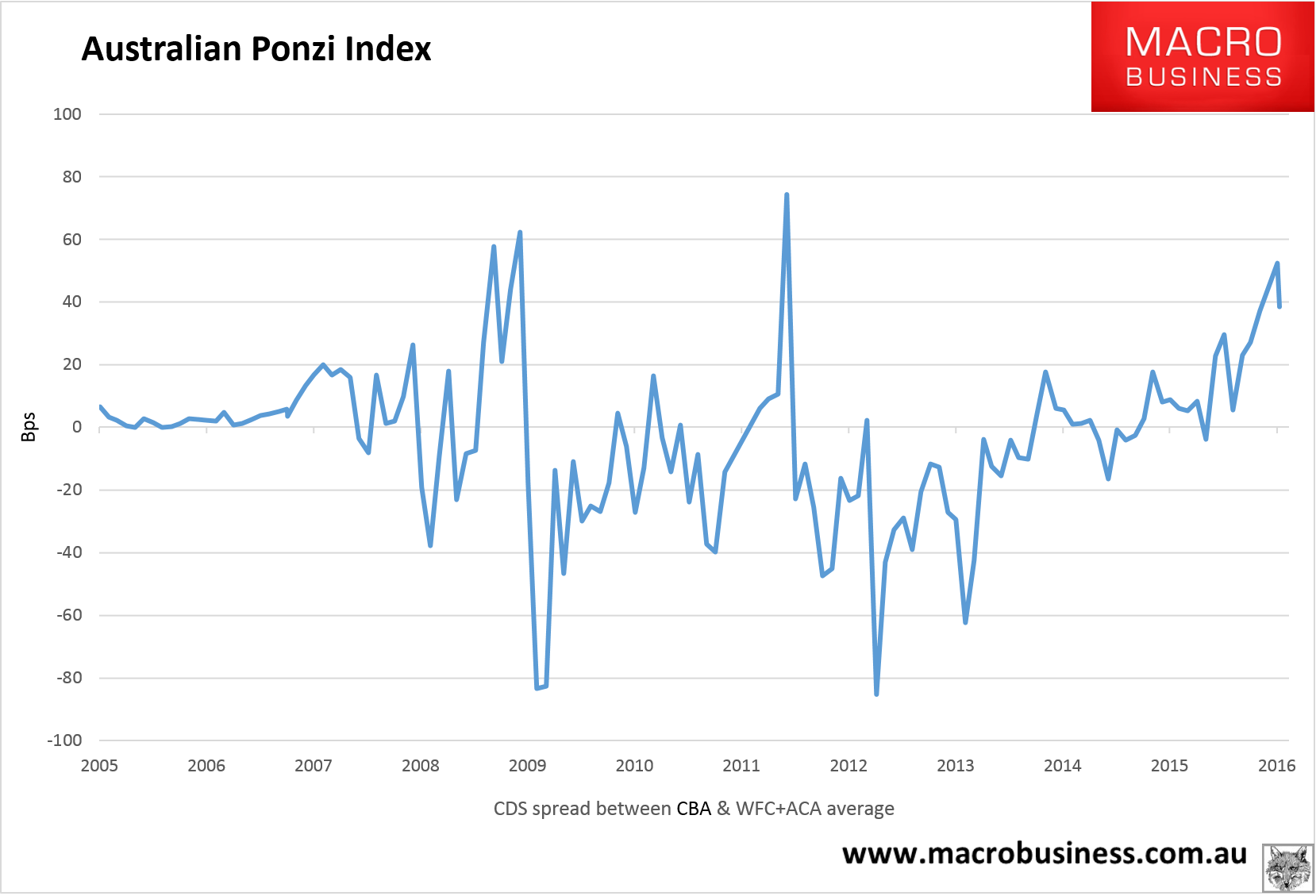

Wells Fargo and Credit Agricole were stable so the relief was Australian specific as US, emerging market and commodity high yield credit continues to de-stress. This the Australian Ponzi Index fell sharply as well:

I don not expect the up trends to break but more relief is possible as long as oil rallies. Chris Joye is putting the squeeze down to APRA, from Banking Day:

Wholesale credit markets are demanding Australian banks pay a higher premium for regulatory risk than their offshore peers for tier two issuance, in particular. And the main reason is perceived uncertainty over how the prudential regulator might apply bondholder bail-in rules in the event of a default.

This was one point made by Smart Money Investments economist and portfolio manager Christopher Joye to an audience of academics and banking sector risk professionals at Macquarie University’s annual Financial Risk Day in Sydney last week.

“When it comes to regulation, I suggest we need to hasten slowly … we should not embed regulatory risk,” he told the audience, suggesting that the Australian Prudential Regulatory Authority had been too quick off the mark in outlining a very strict application of global banking regulations.

“We want markets to price in credit risk. What we do not want markets to do is to price in APRA risk,” Joye said.

Joye asserted that this made the cost of capital for Australian banks accessing offshore credit markets “super expensive”.

By way of example he noted that CBA’s subordinated US dollar paper was recently trading “at 300 basis points over the [benchmark reference rate], whereas crappy European and Singapore banks are issuing at 230 basis points over – that’s a massive risk premium.”

His advocated that APRA’s wide discretionary powers in the event of a bank failure should be traded in for stronger statutory powers.

This compares to the US rules where bail-in of bondholders is set out as part of an orderly asset transfer, following rules set out in the Dodd Frank Wall Street Reform and Consumer Protection Act.

Joye further surmised that, while the major banks might argue that their senior bondholders should not be subject to a bail-in arrangement as that would limit their ability to fund themselves in a crisis, “that logic is completely bogus.”

And here’s why: “We had a crisis recently, in 2008-09 and the senior debt markets shut tight – banks could not borrow one cent on wholesale markets in 2008/09,” he said.

While there may be some uncertainty around APRA tightening, all of it is directed at higher capital which will lower credit spreads not raise them, as all ratings agencies have acknowledged. The Australian premium is a combination of the bubble and the Mining GFC.