Cross-posted from Rational Radical.

Well this is all getting very exciting isn’t it?! The hills are suddenly alive with the sound of housing bubble music. Never mind that a growing mosh-pit of ‘doomsaying’ international economic peak bodies, ratings agencies, investment houses, economists, researchers, entitled Gen-Y bloggers with an axe to grind, and the odd journalist and politician have been rocking out to this bubble tune for the best part of a decade (or more).

We are somehow to believe that we’ve only just pushed play on the soundtrack of dangerous and devastating debt-fuelled asset inflation, rather than the truth that a megaphone has simply been retrofitted to the broken little music box that has been gathering dust on the proverbial shelf of values Australians once cared about, cranking out that same neglected and hated old tune of housing bubble doom.

Our three economic regulators have finally revealed themselves as the three witches busy tending their poisonous brew while chanting “Bubble, bubble, toil and trouble!” to a nation of tone-deaf property speculators and commentators-come-experts. The architects of our dreaded housing and economic Frankenstein are among the last to formally recognise the monster of their own creation for what it is – a hideous creature that defies all reason, logic, decency, ethics and ultimately, any ability to survive.

Such is the well documented exceptionalism and wilful blindness of the collective Australian bubble psychology, that bubble believers and sceptics alike have come to the physics defying conclusion that Australia has invented an actual perpetual motion machine. The problem with perpetual motion machines? They don’t exist. Can’t you just feel the growing friction rubbing up against the bloated sack of housing hot air? I am amazed at how tenacious the belief is that exponentially growing imbalances can go on forever, when every fibre of the economy must be sacrificed at the altar of housing speculation in ever more dramatic interventions just to keep the damned thing afloat for another few months or years. For just one more election cycle.

I’ve been researching the housing bubble, its root causes, and the concomitant bastardisation of our once dynamic and sustainable economic structure for about 6 years. I’ve been writing about it privately for 5 years, and writing about it publicly in this blog for nearly 3 years. Like many hard-working and determined commentators covering this matter of number one moral, political and economic importance, I’ve had my fair share of detractors and flat-earthers taking strips off me and trying to personally discredit me for having a “vested interest” as a young renter (imagine!).

Yet never before have I been so convinced that a self-fulfilling day of reckoning (a ‘Minsky Moment’ for those playing at home) is inevitable and closer than ever. For a passionate blogger with a day job and a family, it has become almost impossible to keep up with housing bubble news these days. It has for the first time in history become the daily issue, and is only set to become more so. If I were a highly leveraged property investor, I’d be starting to get very worried about now. If they haven’t been listening so far, they must surely be starting to sit up and take notice.

In the last month alone (in chronological order):

- A United Nations report concluded that the financialisation of housing is the key determinant of inequality

- All four big banks are hiking mortgage rates “out of cycle”, targeting investors

- Parliamentary Budget Office costed a plan to abolish stamp duty in favour of broad-based land tax

- ASIC chief Greg Medcraft declared the housing market a bubble

- The RBA warned that household debt levels and house prices are endangering financial stability and damaging the economy

- Property bubble called by economist and former Liberal leader John Hewson

- Yet another IMF report concluding that current household debt levels are an unprecedented problem in Australia

- Brisbane and WA developers conducting “the fire sale you have when you’re not having a fire sale“

- Mortgage arrears continue to rise to cycle highs

- APRA rolled out further macroprudential tightening, this time targeting interest only lending

- ASIC joined APRA in interest-only home loan crackdown and scrutiny on mortgage lending standards

- Treasury is rumoured to announce immigration cuts

- Dwelling construction pipeline keeps “building into the bust“, with massive pending oversupply in the major cities

- The RBA detailed its deep concern over housing risks, backing tax reform and tightening of investor lending

- Wage growth and rental growth remain in the gutter

- Chairman of the Financial System Inquiry David Murray warns of 1890s style housing crash and depression

- Limits to negative gearing and capital gains tax concessions have been modelled by treasury

- APRA announced that banks will need to hold more capital against their mortgage books, raising the cost of borrowing

- RBA, APRA and ASIC stand ready to tighten credit conditions further

Everyone is covering their arse, a natural reaction to panic

So here we are. It’s official. We are in a lot of trouble. Nearly everyone in a position of leadership, influence, regulation, expertise, and editorial responsibility has commenced covering their arse. Regulators, economists, politicians, and major media outlets, faced with an incontrovertible truth that runs against their fixed world-view, are promptly following their natural instincts to re-write history and deflect any possible blame for the coming fallout.

Hell, even once raging housing ‘bears’, who in more recent times have given up hope of the laws of physics ever being applied to Australia, have been trying to keep up with recent developments, and are reasserting the likelihood of a major destabilising fall in house prices and an associated credit and banking disaster.

The three stooges of financial regulation move to save their own bacon

The RBA, APRA and ASIC have recently gone to long overdue lengths to explain the damage to the economy and risks to financial stability posed by record household debt levels and house prices. Yet the most significant mea-culpa inadvertently presented by regulators is that restricting growth in mortgage credit will lower house price growth. This is an implicit admission that rising mortgage debt drives prices higher, a fact long detailed by economists like Steve Keen and Philip Soos, and alternative economic media outlets like MacroBusiness who originally led the charge for macroprudential measures to slow the housing market back in 2013.

This admission is actually groundbreaking, because it agrees that physical supply/demand of housing is secondary to credit availability, and therefore that prices being so far detached from incomes and rent must represent a debt-fuelled bubble, not a fundamental shortage of houses to live in. It is an admission that the amount that each prospective buyer or investor can borrow is actually the chief determinant of house prices, and when backed by the favourable tax treatment of land and the textbook speculative belief that prices can only ever rise, has driven prices into the stratosphere without regard for the normal fundamentals of supply and demand.

By contrast, the real supply and demand fundamentals of housing (as a commodity), can actually be observed in the rental market where rents have not even kept pace with wage growth over the bubble period. There are both enough physical homes to house the population, and an inability to use leverage (borrow) to pay rent. The RBA’s admission is thus a refutation of the endless mantra of housing shortage (a characteristic mirage of all land bubbles), and from our top economic custodians.

The RBA has thus admitted that we have a credit-fuelled housing bubble, and they are now moving against it. No amount of mythical housing shortage is going to prevent a material effect on prices from tighter credit conditions. Why else would our regulators pursue these measures that they have for so long ignored or argued against? Contrary to views of the sceptics, it’s not just an exercise in managing public pressures. There is a unified and concerted effort here to dent investor lending, particularly the most dangerous form of lending: interest only loans, the very definition of ‘Ponzi Finance’.

If that doesn’t terrify you, the very fact that the measures announced by the regulators are minimal at best, and are still mostly an effort to deflect blame, means that they are terrified that any substantial measures to control housing credit growth would actually burst the bubble. As I’ve argued at length, they are damned if they do, damned if they don’t, and are trying to engineer a ‘permanently high plateau’ for at least as long as they remain in their jobs, which might see them avoid blame. This much vaunted feat has never been achieved in the long history of bubbles.

Government will never let prices fall, will they?!

Which brings us to the arse-covering measures about to be (or already being) employed by governments of all levels.

Further policy fraud intended to temporarily prop-up prices by bringing forward demand – such as first hone buyer grants, stamp duty concessions, unlocking superannuation etc. – are simply going to force the hand of regulators to directly burst the bubble by hiking interest rates or severe clamp downs on mortgage lending growth. It’s that whole rock and a hard place thing. We have reached a terminal stage of proceedings that prevents yet more gimmicks from manipulating the market much further. The housing ‘market’ is so comprehensively manipulated by successive and traitorous government policies on tax, pensions, superannuation, direct stimulus, investment and financial regulations etc., that further manipulations will have the opposite of their intended effect.

The latest attempts to stimulate the market will simply run up against regulators desperately trying to assist a flagging economy and shore up a financial system under significant threat – which is to say, they will simply force the hand of regulators and burst the bubble.

We look to be approaching the final panic stages of the last blow off in this epic bubble, as the kitchen sink is thrown at the market in a desperate attempt to avoid the inevitable. But it will only do further damage, and ultimately prove futile. This is the cost that we all have to pay for those beloved property prices – that illusory “wealth effect” that simply amounts to a pile of household debt as large as the difference between the total nominal value and the total fair value of the housing market.

Now that’s just the ‘extend and pretend’ side of the policy ledger. The actual anti-bubble, pro-market side of the policy ledger contains mounting risks to property speculators as well, as the affordability crisis has gone on for so long, and become so egregious, that political careers are now coming to depend on doing something about the problem instead of pretending there isn’t one.

Even a federal government that went to the previous election with a platform based on a property-crash scare campaign, and now hell-bent on avoiding real action on housing affordability, is coming under the greatest pressure in the history of this bubble to do something. There appears to still be a very real chance that the government will make some move on any/all of:

- federal land taxation replacing stamp duties,

- limiting negative gearing and/or the capital gains tax discount in some way,

- enacting further enforcement and monitoring of existing foreign investment laws,

- restricting ability of self-managed super funds to make leveraged property investment,

- supply side reform to increase / incentivise the faster construction of homes and infrastructure,

- implementing long-delayed anti-money-laundering legislation,

- or possibly even reducing the net annual migration intake.

Political risks have never been greater for those punting on endless property riches underwritten by a government who “would never let prices fall”. Indeed, yet another ironic and self-fulfilling destiny of such a terminal imbalance in housing affordability and wealth, is that political demographics eventually moves against house prices, as landowners come close to or actually become outnumbered by renters and people who simply understand the risks and damage caused to our collective prosperity by this epic housing bubble.

But isn’t this time different, even the bears have lost faith?!

Perhaps the surest sign of nearing the peak of the bubble is that many housing market ‘perma-bears’ and ‘crashniks’ have seemingly been losing their minds in frustration, and in agreement with many delusional bulls have begun proclaiming that the government and regulators have the ability to prevent the bubble from bursting, as though every economic leader prevailing over historic housing bubbles had not tried the exact same impossible feat.

Fundamentally (and self-evidently), bubbles cannot be supported by market manipulation indefinitely. Did governments in the US, Ireland, Spain (and indeed Australia in the 1890s) attempt to manipulate the market to prevent the bubble bursting? Of course they did. Did it work? Of course it didn’t – in the end.

One of the key characteristics of a bubble is that even the deep skeptics and rationalists begin to imagine that things can go on as they are indefinitely. The problem simply becomes one of self-fulfilling destinies however, as the mathematical imbalances become so extreme, that any move to keep the party going ends up having the opposite effect and panicking the market. Ultimately people are ruled by fear and greed. They are two sides of the same coin, as every bubble in history has proven time and time again. Humans just have a way of forgetting that lesson, over and again.

Surely the Chinese bid will bail us out?

The Great Aussie Housing Bubble is seemingly counter-cyclical to the major residential real estate bubbles that burst in the US, Spain, Ireland, and other European nations, but is actually part of what I think of as the Great Former British Colonies Housing Bubble, in which Australia, New Zealand, Canada, Hong Kong and the United Kingdom itself are all experiencing even worse housing bubbles than the afore-mentioned ones that brought the global financial system and economy to its knees, the true fallout from which still remains largely unresolved.

The main feature common to at least Australia, NZ and Canada (and the reason these bubbles deferred bursting during the GFC), is that they are all major commodity exporters to China, and were in no uncertain terms bailed out by Chinese stimulus over the last 5 to 10 years. As a consequence, they all became comparably attractive places for foreign investment in real estate owing to the perceived (experienced) lack of downside to capital values following the GFC.

Because of this shift in capital flows away from the devastated housing markets in the US and Europe, governments in commodity countries like ours turned a blind eye to damaging capital inflows in order to help ride their respective housing bubbles over the general deterioration in global business conditions. It was just the latest instalment in the global commodification of land and housing, not new in nature, just in scale and distribution owing primarily to the wall of money trying to escape China’s push to reform and restructure its economy.

In light of that context, anyone who looks closely will notice many problems with the idea that the floodgates to more foreign capital can simply be opened up in order to bail out the market (or any other form of policy intervention for that matter). Namely:

- Foreign investment in real estate was widespread in the US and Europe leading up to the GFC, and it did not stop their bubbles from bursting.

- More accurately, such “investment” likely worsened the crash, because foreign capital was much more able and likely to flee a souring market than domestic capital.

- As such, widespread foreign investment in our market has worsened the upside to prices, and will thus worsen the coming downside to prices. It’s a classic case of the demand / supply curve. Steeper up = steeper down.

- Foreign investors are still investors at the end of the day, and while they may not care for cash flow, like anyone they will always care for capital preservation. When the writing is on the wall for a bubble, they will get the hell out, no matter how lax the investment laws may be.

- Additionally, and a point frequently overlooked or underestimated, is that China cannot allow further capital to flee the country in the same volumes as recent experience. It is debasing their currency and destroying their attempts to reform their economic structure away from capital investment towards services and consumption. As such, they have announced tighter and tighter controls on capital flight, including their latest decree that all foreign investments and capital flows must explicitly state its purpose. They will never catch everyone, but recent experience shows that if ever there was a government determined to intervene in its own economy and financial system, it is the Chinese government.

- Chinese investment has helped push the Antipodean / Colonial Real Estate Bubble into its most extreme and final stage. Anyone following global developments will know that the bubble is already bursting in Canada, New Zealand and the UK, and Australia will most definitely be next.

- Because of commodity exports and foreign real estate investment, our collective housing bubbles are in fact bubbles hypothecated on top of the largest debt and housing bubble in human history: modern China. When that finally goes, we are so toast it is not funny.

- A bubble that has caused such severe damage to the social and economic fabric of a country means that political pressures are always ready to invert when people least expect it, and as we have seen in Canada, and now in the state of Victoria, political jobs are now coming to depend on reducing foreign investment and mass immigration. The tide has turned, and we may even see movement on these factors in the upcoming federal budget.

- The proof that foreign capital has already thinned out is in the actions by the Victorian government, which in my view are absolutely a panic move to shore up buyers for the massive pending glut of shoebox concrete boxes, which Chinese nationals are less and less willing and/or able to buy.

But what about our world-beating immigration rate – supply and demand, right?!

One of the last of the dying housing bubble myths is that Australia’s highest rates of immigration in the developed world will bail us out and keep prices from falling. Even a cursory analysis of historical bubbles demonstrates the fallacy of this assumption. Immigration flows tend to be cyclical in nature, and there are many historical examples of immigration crashing through the floor when the bubble finally bursts – as unemployment spikes, recession arrives and asset prices fall.

Our own land bubble from the 1890s, centred around Melbourne post the massive commodities and population boom of the second half of the 19th century shows that unprecedented population growth did nothing to prevent land prices collapsing, and subsequently immigration rates collapsing into the negative. People packed their bags and left, no doubt with good reason as the bust triggered an economic depression worse than that experienced in the 1930s.

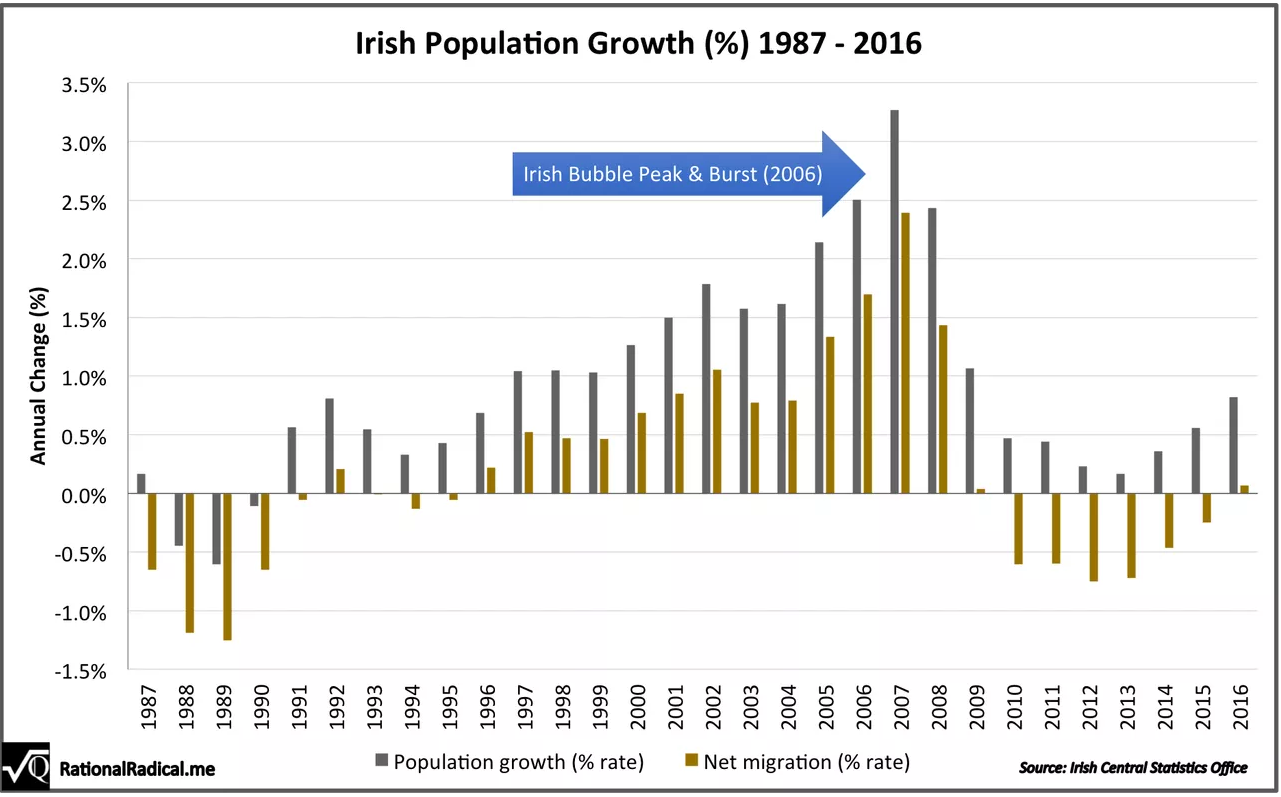

I’ve dedicated an article to this topic previously, but to help round out the destruction of bubble myths currently underway, take a look at the immigration rates in Ireland leading up to and following the bursting of their real estate bubble:

Speculators, foreign investors and baby boomers will to try to cash out all at once

Regulators are specifically (and rightly) worried about the dominance of investors in the market, especially the roughly two-thirds of investors using interest only loans. The unprecedented stock and flow of interest only loans is one of the clearest signs that we are indeed in a speculative credit-fuelled housing bubble, wherein much of the mortgage debt will never be repaid. The investor dominance is also unique compared to previous bubbles and examples from overseas, in that it is much worse. Unlike owner-occupiers, investors (particularly interest only investors) have very little reason or ability to ride out a short-term fall in prices, and will not hesitate to liquidate when trouble strikes – if their bank doesn’t do it for them.

The massive proportions of cash flow negative speculators are the single biggest driving force behind price rises. There are simply not enough homes for every house-flipping speculator to build their property empire, so prices inevitably spike dramatically under this competition and artificial demand for physical housing. That rents have not followed prices (let alone wages) in the bubble era attests to this fact.

Roger Montgomery describes the madness (bubble-fever) that this entails, as investors implicitly assume that the next buyer to facilitate their profit-taking (capital gains) will accept an even poorer yield on their asset, making their negative cash-flow (known as carry) ever more risky. Mathematical and economic certainty ensures that there is a point where the yield is so poor, the cost of transacting and holding the asset so great, that it is either impossible for new entrants to bear or simply unpalatable compared to alternative investments:

“Property income yields are at historic lows and yet property buyers couldn’t be more enthusiastic. Buyers who tell me that they don’t mind buying on a yield of 2.5% because they will get a capital gain need to understand that the capital gain will only come when a buyer is willing to accept an even lower yield. And yields cannot fall much further when your oversupplied property is vacant and your yield is zero – as many leveraged Brisbane apartment owners are about to discover. The end of every bubble is marked by the appearance of the greater fool principle; betting a bigger fool will come along and accept an even worse return. It’s speculation, pure and simple.”

These speculators are utterly reliant on capital gains, and when enough of them realise that capital gains are not forthcoming, the artificial demand for housing will be decimated.

The army of retirees yet to cash out on their paper-wealth is another overlooked aspect of the issue. Unless you are flipping houses or downsizing substantially, you have not actually been made rich by sky-high house prices, as you have not yet cashed-in on the inflated price. When the investor bids start disappearing as their cash flow negative situation forces them to capitulate to a negative capital appreciation future, retirees and superannuants will follow soon after in a come-to-Jesus moment, rushing for the exits in a bid to cash out their presumed gains.

All of a sudden there will be next to no reason to pay the prices currently being demanded – the maxim ‘houses are worth what people are willing to pay’ will come home to roost with devastating speed and certitude. Liquidity is crucial when choosing a quality investment and managing risk. It is always the first thing to disappear when a bubble bursts, and prices can indeed drop significantly faster than the time it takes for the media and market to accept and report that the bubble has burst. By then it is mostly too late.

Housing bubble panic is justified, time to cover your own arse!

So when is the long-awaited crash going to finally happen? And how fast and far will prices fall?

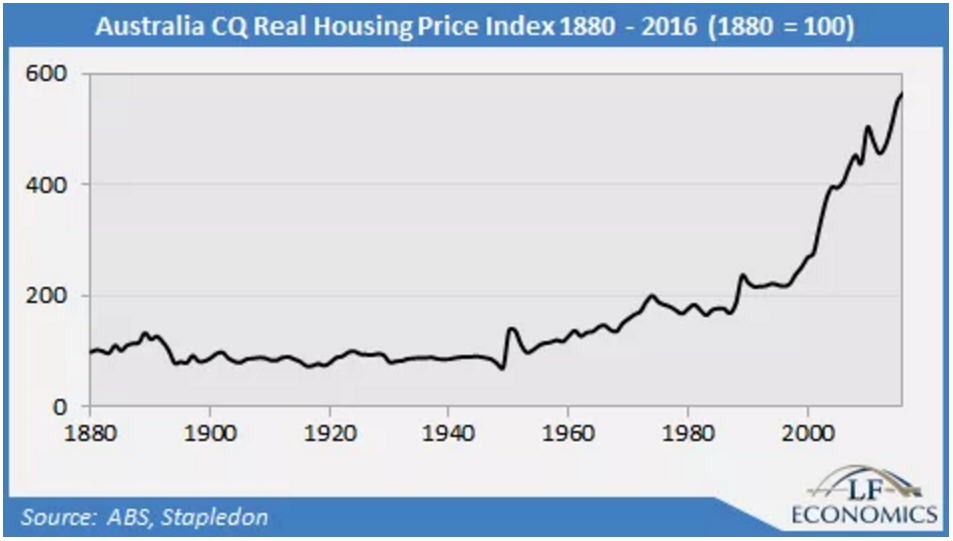

I’m going to cover the issue of price trajectory in a subsequent article, but to give you some robust analysis to this effect, Lindsay David and Philip Soos, two outstanding economists and housing research analysts have recently estimated the likely downside required to return housing to fair value. They estimate price declines of 40% – 60% nationwide, with Melbourne and Sydney needing more like a 65% decline, two-thirds of current prices. Anyone who understands percentage growth / falls knows that 65% fall equates to the erasure of 200% of gains. And that’s before we even consider that markets nearly always overshoot their mark in a major correction.

Put another way, those sort of falls would take real house prices (adjusted for inflation) right back to the fairly stable price-base in the 90s. Their eponymous and widely referenced constant quality real house price series should confirm the validity and likelihood of this possibility:

The crucial issue therefore is one of inevitability over imminence. Timing is a fools game when the risks are so monumental and inevitable. It doesn’t matter whether or not the crash is imminent, it’s coming. I’ve lost track of how many times I’ve explained this point to those pesky bubble-deniers who try to use failed crash-timing predictions to discredit the whole risk argument put forward by ‘doomsayers’ like me. It’s also a point I occasionally have to make for those angry bears who keep running out of patience for the crash that never seems to arrive.

It simply does not matter when exactly the crash will come, because the crash is now undeniably inevitable, and the expected price falls will take us back the best part of 20 years. In the same chart above we can observe that the 1890s price crash went on for half a century, invalidating any folks who might have been regretting “not getting in years earlier”.

Waiting it out really is the only option available to anyone who can comprehend the long and torturous series of events that brought us to this terminal phase of the largest debt-fuelled land bubble in our history. The snapping sound you hear is the dawning realisation in the cultural psyche that we should have listened these past 5, 10, 15 years to those warning that housing bubbles destroy economies and impoverish everyone in the end. And worse, the realisation that no one actually knows what the f*k to do about it, and have thus commenced their elaborate and predictable arse-covering. It is clear that the arse-coverers are already attempting to rewrite history before the bubble has even officially burst.

Whatever happens, always remember that the warnings were ignored for so many years, that any attempts by those with the power to save us from calamity at such a late stage were doomed to fail. Worse, they were probably doomed to actually be the pin that eventually burst the bubble.

Thus it is finally dawning on the collective consciousness that there is an intractable contradiction between Australia’s housing bubble and the ability to have a sustainable economic structure. It is no longer a ‘doomsayer conspiracy theory’ that our current epic house prices and household debt levels are not only a major threat to our financial system, but are also strangling the economy, as I’ve argued exhaustively. This is the ‘damned if we do, damned if we don’t’ Faustian Pact central to our housing bubble, which in the end is bad for everyone, including those who believe that high prices represented wealth without cost.

We have let this thing run so out of control, that if we act to rein it in, the bubble will burst, if we do nothing it will burst, and if we stimulate it further it will burst. And in the mean time the economy is bled dry as the reform process completely freezes in terror at this contradiction.

It’s hard to underestimate the significance of recent developments, which we can broadly summarise as confirming the following terrifying facts:

- The housing bubble is damaging the economy.

- The housing bubble is holding our economic and financial regulators to ransom.

- The housing bubble is only kept alive by sub-prime lending and market manipulation in the form of repeated policy intervention, which enjoy ever diminishing returns to the point of eventual negative returns.

- The housing bubble is one external shock away from a self-fulfilling crash.

- The housing bubble does not need unemployment or interest rates to rise in order to burst, but they will rise anyway.

- The housing bubble will burst if NO reform is made to housing or tax policy.

- The housing bubble will burst if reform IS made to housing or tax policy.

- The housing bubble will burst if more policy stimulus is NOT forthcoming.

- The housing bubble will burst if more policy stimulus IS forthcoming, as it will force the hand of regulators already failing to reign in runaway prices and household debt.

- The housing bubble is set to destroy the fifth government in a row, as all of the above facts completely freeze the political process and any hopes for reform.

- We are now certain to face a very painful and damaging downturn in the housing market, financial system and broader economy, once preventable, now inevitable.

- The longer we attempt to avoid that fate, the worse the adjustment will be – for everyone.

- We cannot escape that fate forever.

So with regulators officially declaring Australian housing a bubble, government set to announce arse-covering measures of their own, and literally millions of cash-flow negative investors, superannuants, and pending down-sizers all set to simultaneously realise their capital gains prospects have vanished, are we still willing to bet that house prices always rise? Are you willing to time one of the most over-valued markets (for anything) on the face of the planet, and cash out just before the crash really arrives? Buy into an investment after 20 years of staggering gains, predicting that more of the same is ahead for you? That a greater fool will eventually accept an even worse investment yield on the assumption of even more capital growth – and the resulting political, social, economic and financial instability? Still think the government has your back? Good luck with that.

Whatever happened to “Buy low, sell high” as a sound investment strategy? Bubbles destroy such rational investment notions. What about “Buy and hold”? Sadly that only works if you don’t need to sell any time in the next number of decades to realise profits. It sure isn’t the strategy employed by that massive army of house-flippers is it? There is no investment strategy that can protect you from this market any more, except for refusing to participate. It’s the only sane choice at this juncture, and I don’t think it’s gonna be too much longer before “Buy low, sell high” becomes the figurative fish that got away. A regret that will likely torture the minds of the masses for at least a generation.

All of a sudden it’s fashionable to panic, and in typical Australian fashion, we love to follow the crowd into the latest fashionable trend. This is a once in a lifetime opportunity to dodge the housing bubble while you still can. So panic now or forever miss out.