The IMF has released a new working paper entitled “Excessive Private Sector Leverage and Its Drivers: Evidence from Advanced Economies”, which provides a quantitative assessment of the gaps between actual and sustainable levels of debt and identifies the key factors that drive excessive borrowing.

Below are some key extracts:

High private debt can have a substantial adverse impact on macroeconomic performance and stability. It hinders the ability of households to smooth consumption and affects investment of corporations. In addition, elevated debt levels can create vulnerabilities as well as amplify and transmit macroeconomic and asset price shocks throughout the economy. Excessive private debt increases the likelihood of a financial crisis, especially when it is driven by asset price bubbles fueled by lending. The subsequent deleveraging could be potentially disruptive for economic activity.

Long-term growth prospects deteriorate significantly following debt-related financial crises. Furthermore, the accelerated pace of private debt accumulation can lead to economic and financial instability, which often coincides with great risk-taking and poorly regulated and supervised financial sector. Finally, spillovers from private balance sheets to the public sector due to government interventions, either direct in the form of targeted programs for debt restructuring or indirect through the banking sector, weaken the fiscal position and increase interest rates. All the above factors may potentially compromise public debt sustainability…

In particular, low interest rates and unemployment along with high house prices tend to be associated with larger gaps in the case of household. This implies that policymakers should pay attention to excessively low interest rates and inflated house prices to avoid imbalances that may ultimately pose risks to macroeconomic stability.

…generous mortgage-related tax incentives that favor ownership over renting can induce excessive borrowing by households and boost asset prices which, as discussed above, are positively correlated with the sustainability gaps. Furthermore, such incentives have important distributional implications and can be costly in terms of foregone revenue for the budget.

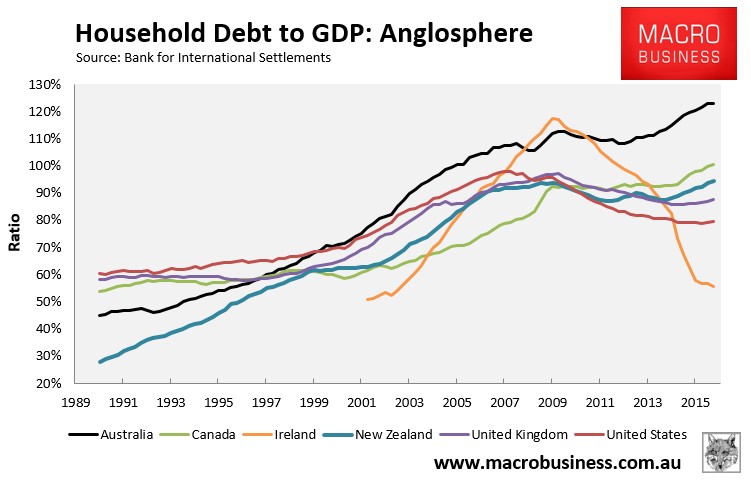

While the IMF doesn’t specifically target Australia, it should. After all, we have the second most indebted household sector in the world and tower above other Anglosphere peers:

Australia also meets many of the risk criteria identified by the IMF, such as “excessively low interest rates and inflated house prices”. We also offer “generous mortgage-related tax incentives” that “induce excessive borrowing by households and boost asset prices”.

Now watch on as the IMF’s warnings are ignored by Australia’s regulators and policy makers.