Two explosions ripped through the check-in area at Brussels’ Zaventem airport, north-east of the EU’s capital and a few miles from Nato’s headquarters shortly before 8am. A third device at the airport failed to detonate and was later dismantled by police.

Then a little more than an hour after the initial attacks, another blast ripped through a metro carriage at Maalbeek station in the heart of the district dominated by EU offices, killing at least 20 people. Belgian media reported 14 deaths at the airport, citing staff at hospitals.

ISIS has claimed responsibility. Let’s put aside the tragedy of it and assess the implications for markets. They’re pretty obvious. The euro weakened:

Advertisement

For the life of me I don’t know why anyone would want to hold the euro. Sure, it is turning itself into an export-led economy with smaller imbalances than others but the politics underlying the currency are dire. Broken fiscal integration leading to anti-European domestic movements now being fed by an explicit ISIS guerrilla war aimed at disenfranchising European Muslims by further fueling local separatist movements. This has already birthed the Brexit referendum and next year we’ll have a Fraxit Federal Election with France’s anti-euro National Front rampant. And all of this fiscal and federal disfunction constantly falls back on the ECB which has to ease further and further to prevent interest rate contagion from tearing the block apart.

The euro is the most structurally weak major currency by a considerable distance and that leads directly to a stronger US dollar:

Advertisement

The strong US dollar is the virtual mirror image of a weak euro so ISIS directly adds fuel to the Mining GFC every time it throws another grenade.

On the night commodity currencies nonetheless rose with the Aussie up and away on the Tragedy of Glenn Stevens:

Advertisement

As oil held firm for no apparent reason:

Base metals eased:

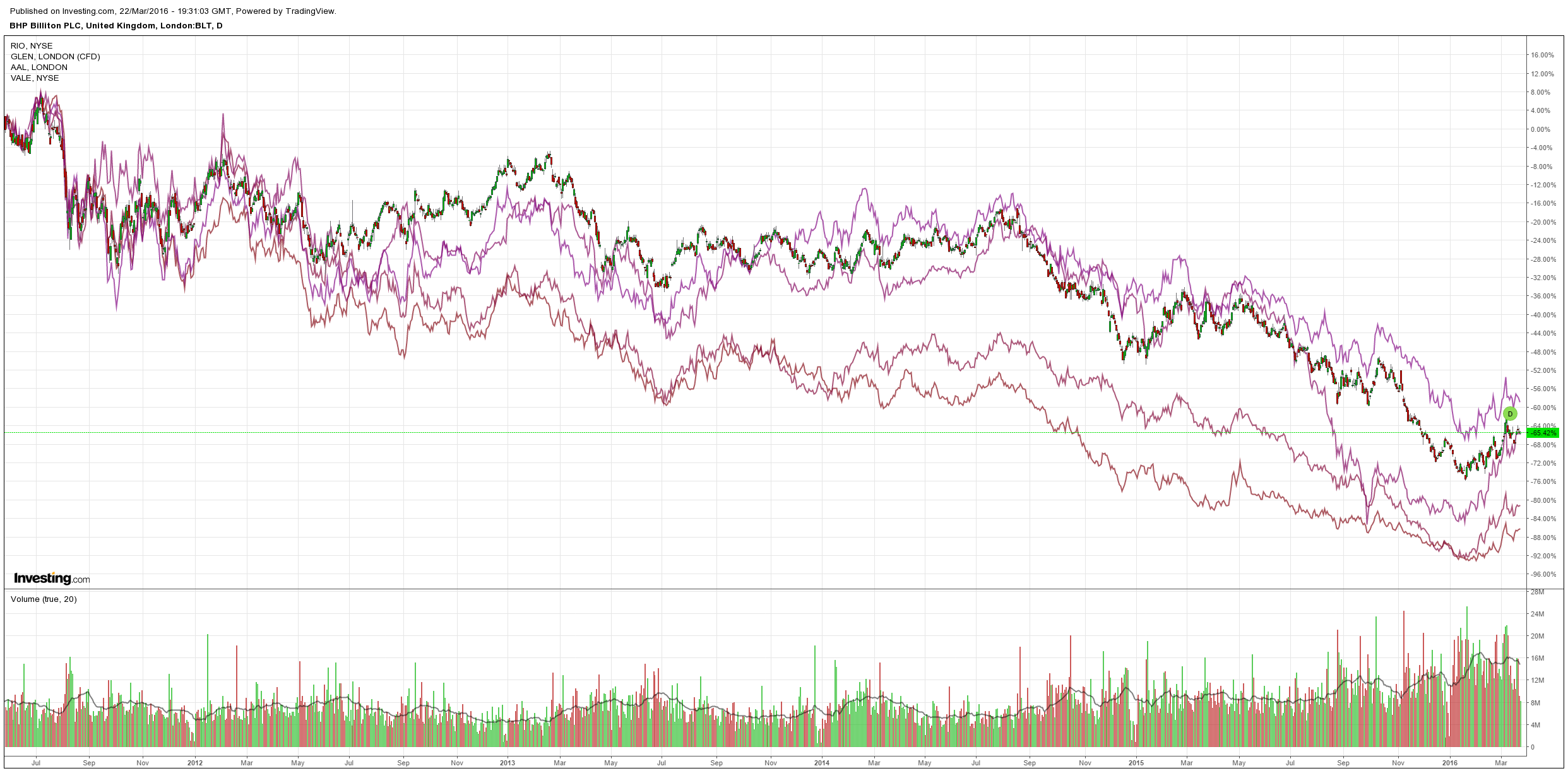

As did miners:

Advertisement

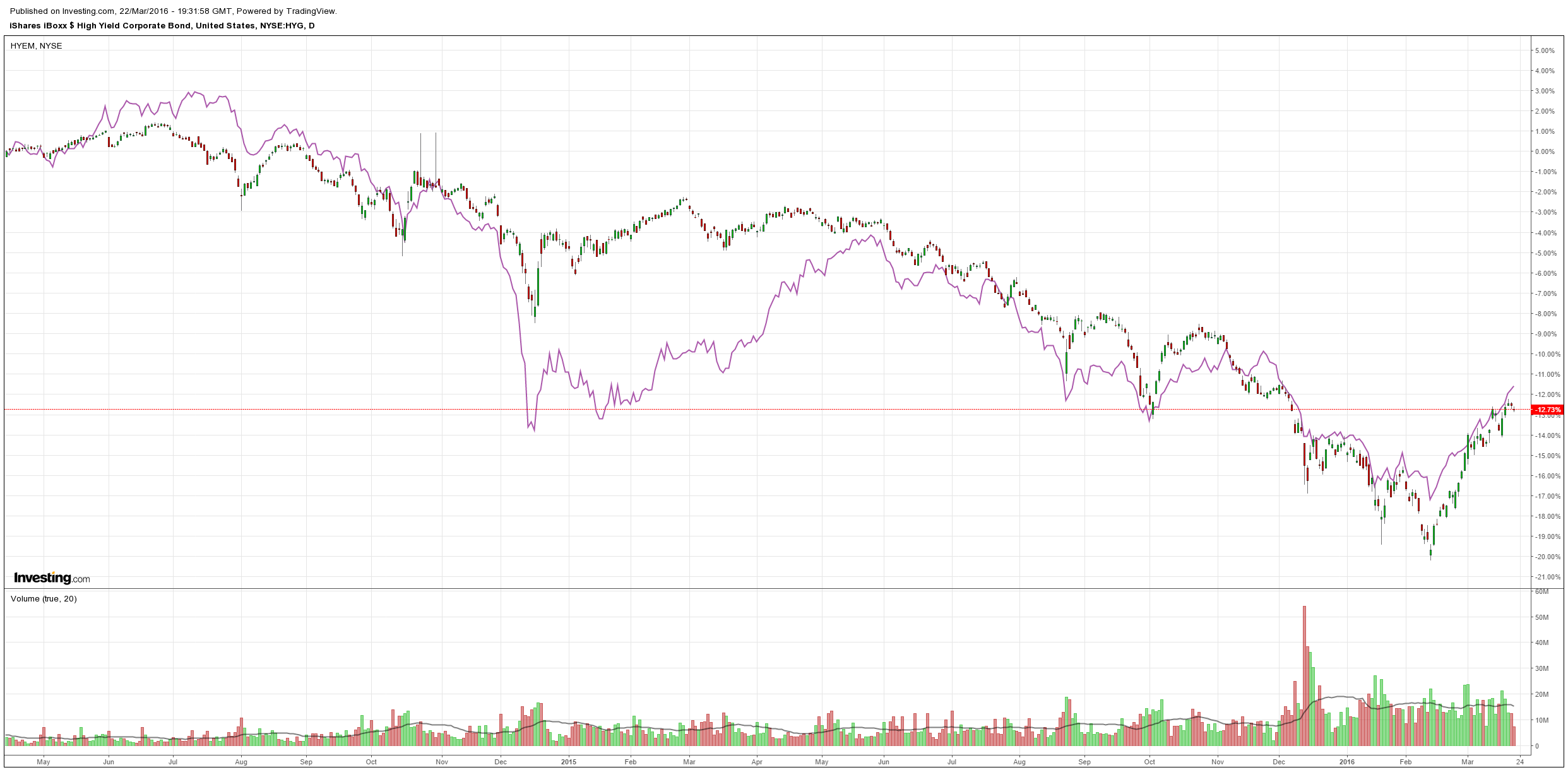

And US high yield was weak but EM remains bid:

Goldman has a second warning for the bear market rally in two days for this column:

Advertisement

Since February 11, oil prices have rallied together with risky assets, supported by better sentiment on global growth, increasing indication of future supply rationalization, and declines in US oil production. At the same time, bond yields have picked up and US breakeven inflation has started to recover, indicating the market is starting to price US reflation. While we see potential for reflation to gain steam in 2H, in particular in the US, the current relief rally across risky assets might fade over the near term. We remain Underweight commodities over 3 months and Neutral over 12 months. As supply adjustments take place, we believe commodities will become more attractive. Until then there is risk of a self-defeating rally as supply cuts might be delayed. We expect volatile oil prices in a US$25-45/bl range, which coupled with negative roll yields should result in poor risk-adjusted returns. Sharp declines in oil prices are likely to weigh on risky assets again. In addition, we see several additional risks entering 2Q (e.g. Brexit, migration concerns, US elections, China, rate shocks), which are likely to drive higher volatility across assets. As a result, we reduce risk in our 3-month asset allocation as we enter 2Q.

We upgrade cash to Overweight over 3 months to position for and take advantage of more volatility. With the potential for cross-asset correlations with oil to increase again should oil prices decline sharply, the potential for diversification is limited. Similarly, rate-shock risk is difficult to diversify. Within cash we have a preference for the USD. We remain Underweight government bonds over 3- and 12-month horizons as inflation continues to pull yields higher and we still expect three Fed rate hikes this year. Over the near term, central bank easing, the dovish Fed, and lower oil prices might support bonds but we do not think US 10-year yields will trade below 1.75% for long.

Our key Overweight remains credit as we believe credit valuations are already pricing a worse growth environment. We continue to prefer EUR IG (and HY) due to a combination of better technicals (especially with ECB credit easing), fundamentals and valuations. Following the strong relief rally in USD HY, over the near term, we think the risk/reward is least favourable if oil prices reverse course. We prefer USD IG to HY near-term. While we expect equities to rebound within a ‘fat and flat’ range once reflation gains the upper hand and as oil prices stabilise, we remain Neutral over 3 months. Until then, equities are likely to remain volatile. Also, equity valuations are not attractive, in our view, having increased further in the rally, with negative earnings revisions. Without a sustained pick-up in growth and inflation, we think equities are unlikely to turn decisively. We retain our preference for Japan and Europe over 12 months, for which we believe valuations are not as stretched and policy remains supportive. However, near term, we are Neutral across equity regions; we like the low US beta and Brexit/migration concerns might weigh on Europe

Correlations across assets and with oil prices have been high this year to date. The oil price recovery since February 11 (due in large part to China relief and the dovish March FOMC meeting) has come with a broad relief rally across assets.

Again I agree but oil still looks strong and the market may push things right through to a firmer shale recovery before freaking out. That will show up in high yield debt first, from BofAML:

The market reaction from last week’s dovish FOMC statement took us by surprise. Due to risks stemming from global economic and financial developments, Chair Yellen kept the target range for the federal funds rate unchanged at ¼ to ½ percent. And although this outcome was largely expected by markets, the Fed also cited global growth concerns and subsequently reduced their growth and inflation forecasts for this year and next. Under normal conditions, the mentioning of global growth concerns by the Fed has been met with a market selloff as a negative economic outlook brings concerns of lower corporate earnings. In fact, the last two times the Fed indicated global risks to the domestic economy, while holding rates steady, high yield declined 4.5% and 4% over the next 13 days (Chart 1).

However, the prospect of lower rates for longer dominated investor sentiment in the 2nd half of the week, causing high yield to return 1.23% in just 3 days. While in the short term lower rates spells risk on and may be good for high yield, we believe the underlying commentary provided by Chair Yellen shows the vulnerability for high yield issuers to longer-term growth trends. Tighter financial conditions, slower global growth, and a strong dollar will all negatively impact future earnings from high yield issuers, in our opinion. And with ex-Commodities YoY EBITDA growth running negative in 3 out of the last 5 quarters (the worst in a non-recessionary period since 2000), we question how much further balance sheets can deteriorate before investors question the overall health of the high yield market. And as we discuss below, when looking at measures other than EBITDA, the fundamental picture becomes even less compelling for the asset class.

We also believe it is telling that bank stocks moved significantly lower after the rate decision. Though the price action in banks makes sense – a lower for longer rate environment reduces these companies’ net interest margin – typically the moves in bank equity and high yield spreads are very well correlated (-48%). In our view the challenging bank environment could be a canary in the coal mine for high yield. As financial volatility increases, bank earnings decline, and unease about the global economy heightens, banks pull back on risk and lending and the ability for corporates to access funding in times of need is compromised. Note the latest Fed survey on lending standards as a prime example of declining risk tolerance for loan officers.

Ultimately, we believe markets are currently responding to a major influx in cash and ignoring the fundamental backdrop for high yield- and this could continue for some time, likely until a negative catalyst takes the market lower. Case in point, in the past 4 months non-commodity spreads have been 85% correlated with crude oil prices (Chart 2). Such a high correlation suggests to us that investors have taken their eye off the ball with respect to non-commodity balance sheet health- something that is likely to lead to a surprise increase in defaults and negative price action later this year.

To this end, we wonder how long asset allocators will continue to focus too intently on transitory risk-on signals while ignoring the weak macro credit environment. Couple the deteriorating fundamentals for high yield issuers with downgrades outpacing upgrades by a ratio of 3.5:1 and a worsening of global growth potential, and we believe the recent rally, though boosted by strong inflows and cash generation, will ultimately fade.

…Bolstering our view that investors should not be lured into the temptation of throwing caution to the wind is that from our perspective, there still seems to be very heavy headwinds blowing directly into the path of the global and domestic economies. In fact, though the manufacturing and production portion of the economy appears to have bottomed out, the consumer now looks to be experiencing unexpected – if only modest so far – weakness. And as capital markets continue to remain challenging for the lowest quality issuers, we are concerned of the potential pitfalls of a tightening credit market in the context of a world where revenue growth and share prices were boosted by easy monetary policy and cheap debt. Although our economists wrote last week that they are not seeing signs of economic deterioration through the credit channel, we still worry that an elongated period of tight credit markets could ultimately weigh on hiring over the course of 2016 and 2017. And although it seems that for the time being investors are willing to overlook some signals suggesting a weaker consumer, we believe eventually renewed concerns of a global and US slowdown will overtake any reach for yield activity. Whether the concerns are justified or not is likely to define the shape of the cycle (slow and exaggerated, as the last 18 months have been, or shorter and steeper, as in 2009) but not whether the cycle has turned.

Our economists believed in the beginning of the year that recession concerns were overdone. And although we are more bearish than they are on the longer term prospects of the economy, we agreed. The market clearly got ahead of itself in thinking we were currently in a recession or headed toward one within the next few months. However, we stress, it doesn’t take a recession to have bad markets (4.95% yields to 10% yields in 20 months can attest to that) and the study of recession probabilities should only be viewed in determining the shape of the cycle, not whether the cycle has turned or not. In other words, a recessionary environment is likely to bring a peak default rate while a non-recessionary environment is likely to bring exactly what we have experienced over the last year and a half: a rolling blackout. Not exactly a time period most credit investors will look back fondly upon and very reminiscent to 1998 – 2002.

Having said the above, we think it’s necessary to break down the economic data; not only to show that a) our economists were correct, but b) to show that markets have reacted just as irrationally on the way up as they did on the way down.

Not only has the ratio of tangible to intangible assets fallen markedly since 2013, but by further adding back “1-off” impairments to EBITDA, companies are inflating cash flow while also not taking into account the decreases in asset values that have direct consequences to the value of the firm. Because the ability of a company to finance itself through debt markets is (or at least should be) a function of the firm’s value in addition to its cash flow, the amount of debt a corporation has relative to its tangible assets becomes more and more important as the credit cycle wanes. In fact, as we are seeing from the commodities sector today, as well as some other idiosyncratic businesses that have recently run into trouble, debt to asset value is as important a measure as any when a firm realizes problems and needs to liquidate holdings. And the trend in total debt to tangible assets has been troubling, as companies have increased debt on asset values that have stagnated or begun to decline.

… when considering our universe of 397 high yield issuers we find that 79 or 20% of them are unlikely to generate enough cash to service their 2016 bond and loan payments, when also taking into account a company’s cash on hand. Expanding this analysis into 2017 and 2018, we find that 27% and 38% would potentially be unable to meet all upcoming debt maturities. While it is true that roughly 62% of these companies are commodity-related, that still leaves 14% of our ex-Commodity universe that absent asset sales or new debt financing would not be able to make all debt payments between now and 2018.

Of course, companies can find alternative methods to generate liquidity such as accessing the capital markets and selling assets on their balance sheet. However, if all companies were to sell 20% of their tangible assets at 75% of book value, 6% will still have negative cash generation by the end of 2016 and 27% by the end of 2018. What’s more, given the constant need to invest and grow through capex, likely requiring investment rather than divestiture, any company that is forced to sell 20% of the assets on its balance sheet to meet debt obligations will simply be kicking the can down the road and eroding bond holder value. Though negative cash flow is in and of itself not a reason for default, and in fact many companies for a variety of reason chose to run their business negative for a period of time, in an environment where asset values are declining and access to capital markets is difficult, we think the large negative numbers could be concerning. Given the high percentage of companies continuing to burn a quickly diminishing stockpile of cash, we believe investors should be more concerned about the possibility for significantly wider spreads on new issue (and hence secondary paper) as investors allow the firm to buy time so they can realize the value of the assets, or at worst, end up in default.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.