Back in November, I warned about the potential threat to Australian coal and gas exports from the burgeoning shale gas boom in the US:

…the exploitation of shale gas in the US has seen significant coal to gas switching in power. As a result, surplus US coal is being redirected into the seaborne market, which is adding to supplies into Asia and depressing prices globally. According to the Energy Information Administration, the US used 18% less coal for electricity generation in the first half of 2012 than in the same period in 2011, and 27% less than in 2008, which was the year coal consumption peaked. And by March 2012, coal’s share of the US electricity-generation market had fallen 34%, from 47% just three years earlier. All over the US, coal-burning electricity plants are reportedly closing down or converting to natural gas, whose prices had fallen by -56% in the year to April 2012.The US is the world’s second biggest coal producing nation after China. With coal being displaced domestically by cheaper natural gas, the US is moving to export its excess to the rest of the world, helping to push down coal prices globally. Indeed, US coal exports reportedly rose 56% between 2009 and 2011, according to Businessweek.

Second, as noted by Houses & Holes on Friday, there are reportedly 15 large LNG projects seeking approval to export from the US. And according to the recently published International Energy Agency (IEA) annual report, the profit margin available from exporting gas to Asia is expected to remain far more attractive than prices available within the US (see below chart), suggesting that the desire to export LNG from the US will only grow.

Looking ahead, Australian LNG exports are facing increasing competition from lower cost and equally reliable US supplies, which is likely to crunch profit margins, curtailing Australia’s pipeline of gas projects.

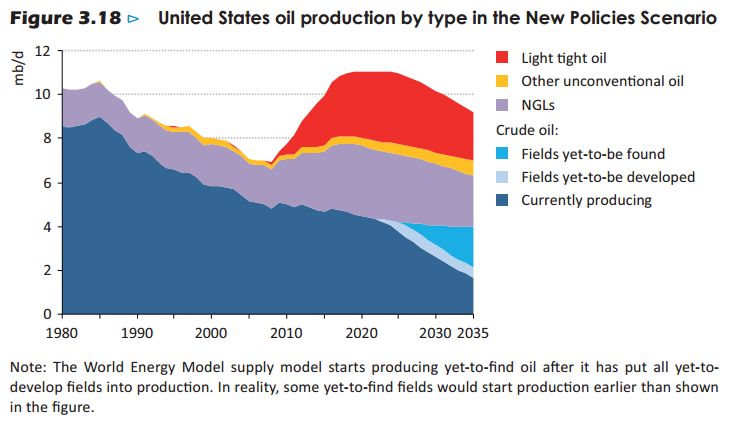

Finally, with Australian LNG export pricing linked directly to oil prices, and the production of shale oil in the US tipped to surge (see below IEA chart), there is the possibility that global oil prices could slump as the US begins exporting oil and/or imports less oil from abroad, resulting in lower prices for Australian exports of LNG.

When viewed alongside declining demand for thermal coal within China as it shifts towards alternative energy sources (e.g. renewables), Japanese moves to end oil-linked pricing on LNG imports, as well as the recent discovery of large gas deposits in Africa, it appears that the Australian LNG and thermal coal industries are facing some very stiff headwinds that could challenge previously held assumptions about profitability and project viability.

Today, The Australian has run an article summarising a recent Deloitte report arguing that Australian LNG exports would suffer the most in the event that US LNG exports take-off in a big way:

Advertisement

AUSTRALIA will be the biggest loser among liquefied natural gas exporters if US LNG production takes off in a meaningful way, with more exports displaced than any other nation because of the high costs of building new projects.

…If a substantial amount of US LNG is exported to Asia, it could displace the equivalent of one $20 billion project in Australia, the Deloitte report on the global impact of US LNG exports says.

US exports, which are being made economic by a shale gas glut, would also weigh on LNG prices…

“The largest LNG source that is displaced is Australian LNG”…

“We think the market will continue to move forward and grow for LNG projects in both the US Gulf Coast and British Columbia,” Mr Utt said…

The study and the KBR comments come after US major Chevron — the biggest spender on Australian LNG — last month took charge of a Canadian project, known as Kitimat, just after pushing back the timetable for an expansion of the Gorgon LNG project and adding $9bn to the expected cost of the now $52bn foundation project.

The Deloitte study, without making forecasts of US LNG volumes, measures the effects that 47 million tonnes a year of US LNG would have on global trade.

This is less than half the amount of export capacity on the drawing board in the US but is in line with estimates by energy giant Shell and represents exports from just four projects. If those US exports go to Asia, about 19 per cent of the volumes, or 9 million tonnes, would be made up of LNG that otherwise would have come from Australia, Deloitte says.

The 9 million tonnes a year of potentially displaced Australian LNG production would be the same amount as the $US20bn Australia Pacific LNG project at Gladstone being built by Origin Energy and Conoco Phillips is aiming to produce.

If the US exports go to Europe, that number would drop to about 4 million tonnes. The upper estimate is about 10 per cent of Australia’s projected LNG exports.

It is important to keep these competitive losses in perspective. The Deloitte report also shows just how propitious the LNG boom has been for Australia:

Even losing 20% still projects us as the largest producer in the world from next to nothing in an incredibly short time-span. That it happened when it did is perhaps the major reason your house is not worth half its current value.

Still, as H&H argued last year, this competitive pressure is choking the pipeline of further investments and there are unlikely to be any new major projects meaning Australia mining investment cliff is approaching mid this year.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.