The Sunday Age/SMH ran two articles picking-up on the looming threat to Australian coal and gas exports caused by the shale oil and gas boom currently gathering pace in the US. First, here’s David Pott’s take on the situation (my emphasis):

…our sovereign debt is low by global standards, but it’s a different picture when you add household and business borrowings as well.

That puts our debt burden at 321 per cent of GDP, far worse than basket case Greece’s 274 per cent, according to AMP Capital’s chief economist, Shane Oliver…

Australia tends to fly under the radar because a good part of the debt has gone on mining investment, considered more credit-worthy than investing in schools, hospitals and tanks.

Yet we may have managed to blow the mining boom. Two-thirds of the investment has been in energy projects, namely gas.

Trouble is, gas prices are lower than when they were commissioned. And their costs are a lot higher, in part because of the strong dollar – they’re all foreign-owned, and so count in depreciated US dollars.

The talk is that the gigantic, aptly named Gorgon project is running about 50 per cent over budget.

Worse, there’s a gas glut in the US supplied from shale, which will make it more than self-sufficient in just a few years.

If the dollar stays strong, the US will probably be able to export LNG to Asia cheaper than we can. At the same time the gas glut is tipping coal no longer needed in the US onto the market. Our LNG contracts are indexed to the oil price, so fingers crossed it holds up.

After all, higher petrol prices would be a small price to pay for keeping the boom alive.

And here’s Malcom Maiden discussing some of the implications for the global economy arising from the boom in US shale oil and gas:

The growing consensus on Wall Street is also that the US shale boom is a global economic and geopolitical game-changer…The US will certainly benefit from cheap domestic gas that will deliver cost benefits to heavy industries including petrochemical plants and power stations, but the horizontal drilling and rock-fracturing technology that is freeing up shale gas and oil will ultimately generate sweeping global changes.

Shale oil can be commercially exploited at oil prices as low as $US80 a barrel, and as shale oil volumes rise, oil price spikes in response to accelerating growth in demand that work to slow demand again will be much less frequent. Shale oil, in other words, is going to raise the maximum speed limit of the global economy.

Looking ahead, Australian LNG exports are facing increasing competition from lower cost and equally reliable US supplies, which is likely to crunch profit margins, curtailing Australia’s pipeline of gas projects.

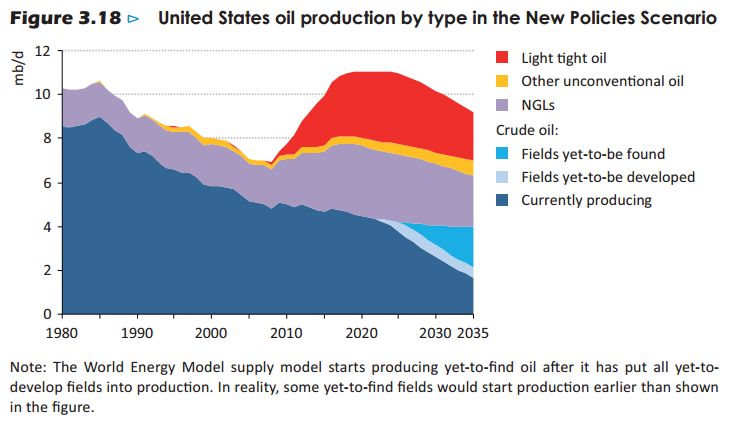

Finally, with Australian LNG export pricing linked directly to oil prices, and the production of shale oil in the US tipped to surge (see below IEA chart), there is the possibility that global oil prices could slump as the US begins exporting oil and/or imports less oil from abroad, resulting in lower prices for Australian exports of LNG.

When viewed alongside declining demand for thermal coal within China as it shifts towards alternative energy sources (e.g. renewables), Japanese moves to end oil-linked pricing on LNG imports, as well as the recent discovery of large gas deposits in Africa, it appears that the Australian LNG and thermal coal industries are facing some very stiff headwinds that could challenge previously held assumptions about profitability and project viability.

Twitter: Leith van Onselen. Leith is the Chief Economist of Macro Investor, Australia’s independent investment newsletter covering trades, stocks, property and yield. Click for a free 21 day trial.