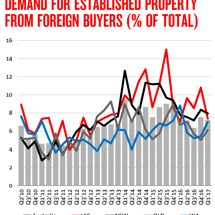

Melb/Syd auction clearances still running hot

CoreLogic released its auction report yesterday, which revealed another weekend of strong auction conditions, despite the national auction clearance rate falling to 77.6% from 78.1% last week, and remained well above the 67.1% recorded in the same weekend last year: Auction volumes nationally (3,424) were also way above the same weekend last year (1,831).