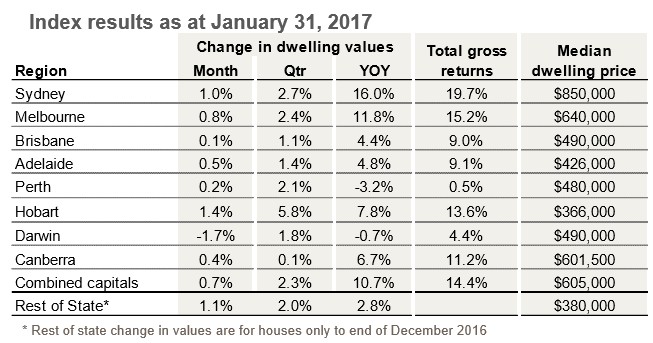

Following on from this morning’s post on CoreLogic’s daily dwelling values index results for January, CoreLogic has released its full results, which also cover the smaller capitals and regional areas (see next table).

As shown above, the smaller capitals and the regions had a mostly positive month in January, with Hobart (+1.4%), Canberra (+0.4%) and Rest of State (+1.1%) reporting value gains, partly offset by a 1.7% fall recorded in Darwin.

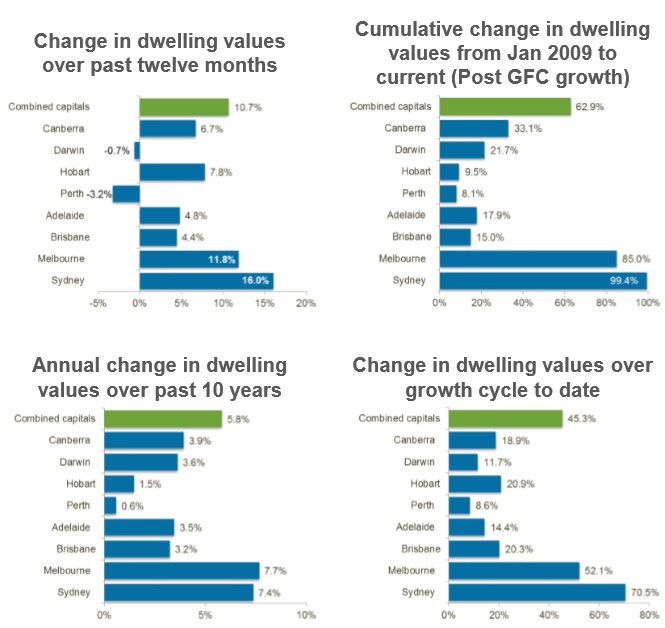

Below are the key charts summarising the situation across the markets, with Sydney and Melbourne continuing to dominate:

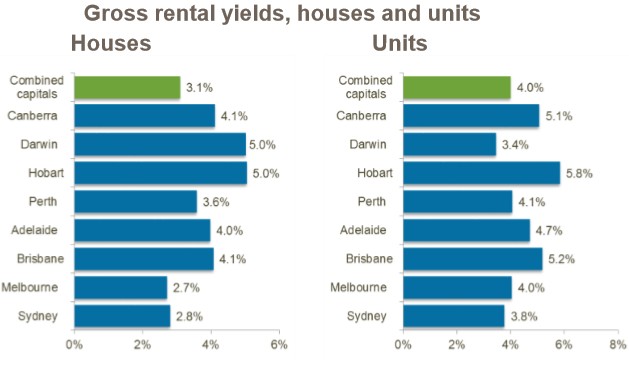

The combination of weak rents and capital appreciation continues to compress rental yields, which have fallen to another record low level:

According to CoreLogic:

Gross rental yields slipped to a new record low across the combined capitals index in January, with the gross yield on a house now recorded at 3.20%, falling from 3.50% a year ago and 4.12% five years ago. The gross yield on a unit also reached a new record low in January, recorded at 4.01% across the combined capitals; down from 4.25% a year ago and 4.86% five years ago.

Disaggregating the yield data down to the capital city level reveals that Sydney, Melbourne and Darwin are the cities driving yields to new record lows. The gross yield on both houses and units reached a new record low in January across Sydney and Melbourne, while unit yields in Darwin also reached a record low.

Mr Lawless said, “While rental yields plumb new lows, investment in the housing market has been consistently ratcheting higher which implies that investors are speculating on further capital gains in the housing market.”

The latest housing finance data from the Australian Bureau of Statistics indicates investors comprise 47% of the value of new mortgage demand (excluding refinances), with investors in New South Wales accounting for 58% of new mortgage demand and investors in Victoria comprising 45.0% of new mortgage demand.

CoreLogic also believes that the housing market is starting to see some headwinds, which should curtail price growth over 2017:

“Affordability constraints are likely to become more pressing, particularly in Sydney, where the dwelling price to income ratio was approaching 8.5 times in September 2016. The deposit hurdle is becoming a larger barrier to entry with additional costs such as stamp duty adding to the high entry costs for housing. While mortgage serviceability remains reasonably healthy, mortgage rates are already edging higher on the back of higher funding costs, which could progressively take some heat out of investment demand. In addition, with house prices continuing to increase, the supervisory focus from APRA and risk committees can only be expected to increase in 2017, suggesting a continued trends towards tighter credit policies amongst regulated institutions. ”

“Investors comprise almost 50% of new mortgage demand nationally, so a downturn in investment activity would likely reduce housing demand and remove some of the pressure on value growth. When the previous APRA speed limits came into effect we saw the rate of value growth slow throughout the second half of 2015. If we continue to see investor participation rising across the housing market, additional regulatory changes may come into play. This may occur in any event, depending on developments in the international regulatory arena in 2017”

Mr Lawless cites the large number of high-rise units currently under construction as another factor that may slow overall housing market performance. He said, “Dwelling approvals have already peaked across the high rise sector, as have construction commencements. However, the unit supply pipeline remains at unprecedented levels with a large proportion of these high rise units located within the inner city regions.”

“As these units flow through to settlement, the risk of buyers receiving a finance shock is becoming heightened.”

”Metadata flowing across CoreLogic valuation platforms is showing more than 40% of off-the-plan settlement valuations are coming in under contract price across the Melbourne, Brisbane and Perth unit sectors. While the large majority of these ‘under valuations’ are not showing a significant gap between the contract price and settlement valuation, more significant differences can be seen in some projects and precincts. Buyers who receive a valuation lower than the original contract price will generally require a larger than expected deposit in order to meet the loan to valuation ratio required by the lender.”

“While growth rates are likely to slow over the year, low mortgage rates and strong population growth are likely to keep a floor under housing demand,” Mr Lawless concluded.