Categories

Australian interest rates

RBA and ScoMo are at loggerheads over the bubble

Via Domain: Billions of dollars of congestion-easing infrastructure projects that could boost the economy and increase safety are stuck years down the track as the Reserve Bank of Australia calls on the Morrison government to do more.

David Llewellyn-Smith

7 years ago

3

Westpac: “Very hard to see” jobs reaching RBA target

Via Westpac: An expected soft update but a robust trend in participation is making it very hard to see unemployment getting below 5% any time soon, let alone getting down the RBA’s natural rate of 4.5%.

David Llewellyn-Smith

7 years ago

7

Wayne Byers is no longer tenable

David Llewellyn-Smith

7 years ago

20

Capital Economics: RBA to cut to -50bps

David Llewellyn-Smith

7 years ago

21

APRA staff: Management is captured

At the AFR come stunning leaks from APRA staff via its internal review: “When institutions are consistently able to get a different result by appealing to GM levels and above, line supervisors become demoralised and institutions become emboldened to push the limits,” one employee said.

David Llewellyn-Smith

7 years ago

18

RBA foghorn: Lowe bullying Recessionberg, not other way around

Interesting from RBA foghorn Terry Mccrann today: Any suggestion that Reserve Bank governor Philip Lowe compromised his or the RBA’s independence with his ‘meet and quote’ with Treasurer Josh Frydenberg last week is just silly and quite simply doesn’t square with the facts.

David Llewellyn-Smith

7 years ago

1

Wayne Byers must resign immediately

Obviously enough. Via the ABC: An independent review is urging the overhaul of the Australian Prudential Regulation Authority (APRA), slamming it for a poor culture and variable leadership.

David Llewellyn-Smith

7 years ago

6

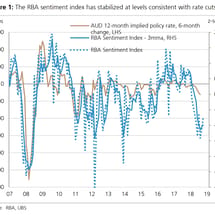

RBA sentiment index still at rock bottom

Via UBS: Implications: UBS still -25bps by Nov; but risk of earlier “if needed” The RBA cut to 1.00% ahead of our long held dovish view. We still think their GDP forecasts will be downgraded again in their Aug SOMP, raising their UR profile (falling to 4¾%).

David Llewellyn-Smith

7 years ago

5

Bill Evans: RBA to pause cuts

Via Bill Evans at Westpac: The minutes of the July monetary policy meeting of the Reserve Bank Board confirm that the Board is still open to further monetary easing, although as we had expected, prospects for a third consecutive easing in August have been dampened.

David Llewellyn-Smith

7 years ago

24

Lunatic RBA: Rate cut for spending not speculation

June rantings from the Lunatic: International Economic Conditions Members commenced their discussion by noting that growth in the global economy had remained moderate over preceding months.

David Llewellyn-Smith

7 years ago

10

RBNZ is a litmus test of Australian monetary failure

As we know, the superb RBNZ has fully integrated monetary and macroprudential policy tools, a creative leadership and national interest values.

David Llewellyn-Smith

7 years ago

4

Pascometer redlines on Lunatic RBA

Weeoo, weeoo, weeoo.

David Llewellyn-Smith

7 years ago

17

Inflation expectations continue to plummet

From Roy Morgan Research: In June, Australians expected annual inflation of 3.8% over the next two years as the RBA cut interest rates to a record low 1.25% in the first week of June.

Leith van Onselen

7 years ago

5

Mortgage stress hits records highs

Via Martin North: We have released the June 2019 mortgage stress results, based on our running 52,000 household surveys.

David Llewellyn-Smith

7 years ago

20

Is the RBA two and through?

So says Morgan Stanley: We think the RBA will continue to express the view that fiscal policy will provide more effective easing from here, and look to that to provide the next tranche of stimulus (if needed).

David Llewellyn-Smith

7 years ago

13

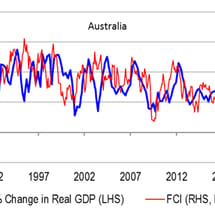

RBA back on the curve

Via the excellent Damien Boey at Credit Suisse: We have updated our proprietary financial conditions index (FCI) for Australia in the wake of the RBA’s decision to cut rates (again).

David Llewellyn-Smith

7 years ago

2

Evil Anna opposes responsible lending

And I thought “Evil” Anna Bligh had disappeared.

David Llewellyn-Smith

7 years ago

16

As RBA lunacy sweeps nation, not one mention of APRA

It’s wall-to-wall Lunatic RBA today.

David Llewellyn-Smith

7 years ago

8

Lunatic RBA still lost on why it will cut again, and again, and again…

Via Chief Lunatic, Phil Lowe, last night: A very warm welcome to this community dinner with the Reserve Bank Board and senior staff.

David Llewellyn-Smith

7 years ago

7

Bill Evans: RBA to cut again in November

Via Bill Evans at Westpac: As we expected, the Reserve Bank Board lowered the cash rate by 25bps to 1.00% at its July meeting.

David Llewellyn-Smith

7 years ago

25

ANZ cuts 25bps, CBA and NAB 19bps, WBC ponzi’s up

Via ANZ: Today we have decided we will reduce variable interest rates for our home loan customers by 0.25pc pa.

David Llewellyn-Smith

7 years ago

23

Big banks smashed on rate cut

Tipping point anybody?

David Llewellyn-Smith

7 years ago

11

RBA cuts again

The RBA is out with its July decision and it is chopity chop, chop: At its meeting today, the Board decided to lower the cash rate by 25 basis points to 1.00 per cent.

David Llewellyn-Smith

7 years ago

143

One reason the RBA may not cut today

Via the AFR comes the ubermen: But The Australian Financial Review Rich Lister and shopping centre billionaire Con Makris and the chief executive of the largest collection of convenience shopping centres in Australia Anthony Mellowes both said cutting rates would not send the right signal.

David Llewellyn-Smith

7 years ago

19

Shadow RBA says don’t cut

Might as well just put out the press release on automatic pilot: Australia’s inflation rate, at 1.3% (March quarter), remains well below the Reserve Bank of Australia’s official target range of 2-3%.

David Llewellyn-Smith

7 years ago

14

Newer Articles

Older Articles

Page

79

of

160

Newer Articles

Older Articles

Advertisement