Yes, this is what monetary policy has come to, via George Theranou at UBS:

The RBA seems to be shifting from inflation targeting towards the labour market as the key policy driver. Their April minutes noted a scenario to cut “would likely be appropriate”…”where inflation did not move any higher and unemployment trended up”. Furthermore, while the RBA held in May, they still shifted in the dovish direction saying “further improvement in the labour market was likely to be needed for inflation to be consistent with the target.” This raises the prospect they could now cut with any rise in unemployment; or potentially even if unemployment fails to fall as they project.

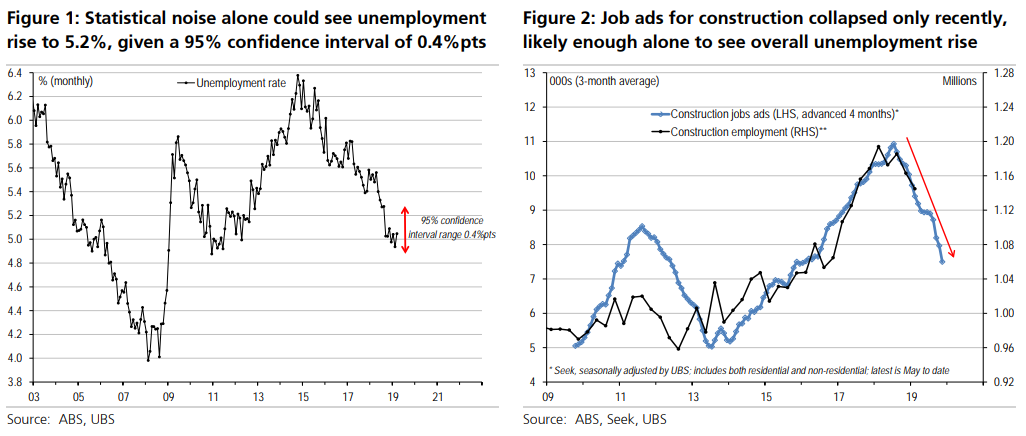

However, the labour force survey uses a tiny sample of ~26k dwellings, or 0.32% of those aged 15+, so m/m moves are incredibly uncertain. Indeed, the 95% confidence interval – bounded by 2 standard deviations – for unemployment is a massive 0.4%pts (or 0.2%pts each way); & for employment is a huge 122k (or 61k each way).

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.