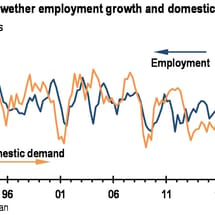

Realtors, construction workers smashed by housing bust

By Leith van Onselen Andrew Wilson of MyHousingMarket estimates that Australia’s real estate sector shed about 8,100 jobs in the year to February, while about 15,000 real estate agents have left the industry since the housing market peaked in 2017.