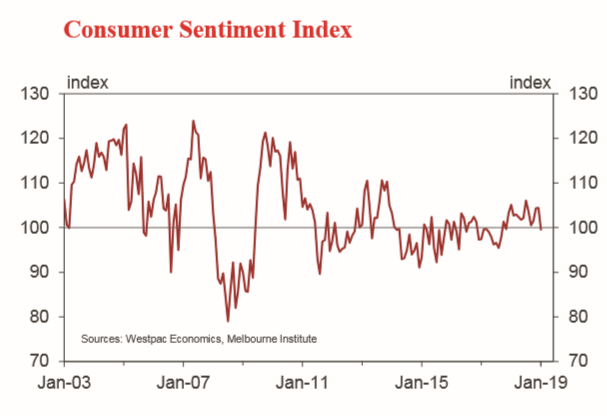

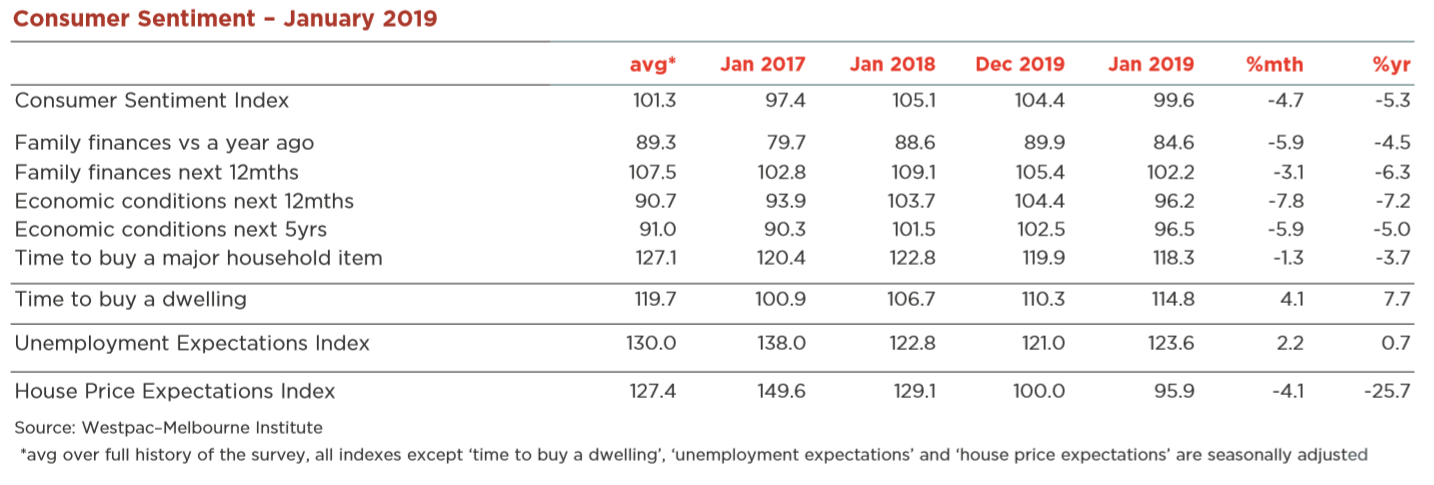

The Westpac-Melbourne Institute Index of Consumer Sentiment fell 4.7% to 99.6 in January from 104.4 in December.

The ‘cautiously optimistic’ consumer mood that prevailed through 2018 has evaporated with sentiment beginning the new year with a slightly pessimistic view. At 99.6, the Index is below the 100 level, indicating that pessimists outnumber optimists, although only by a slim margin. This is the first time sub-100 reading from the survey since November 2017.

Confidence has come under pressure from a number of fronts including a continued slide in house prices; disappointing updates on Australia’s economic growth; ongoing concerns around global trade wars; and political uncertainty. Indeed, the continued optimism late last year was something of a surprise, implying the consumer mood was still getting considerable support from low interest rates, diminished fears of rate increases, a firm labour market, and at the margin, lower petrol prices. Other factors may also have weighed negative on sentiment in January including the Australian cricket team’s first domestic test series defeat to India.

The January sentiment fall is significant, marking the biggest monthly decline in over three years. January reads should be treated with some caution as the Index is adjusted to remove a regular boost to sentiment over the holiday season. However, even allowing for this, the update clearly marks a poor start to the new year. The Index is down 5.3% compared to this time last year.

All index components recorded declines with the biggest falls around expectations for the economy and assessments of current finances.

On the economy, the ‘economic outlook, next 12mths’ sub-index dropped 7.8%, the biggest fall since September 2015 when sentiment was hit by a sharp sell-off in financial markets and a disappointing update on Australia’s growth. The ‘economic outlook, next 5yrs’ sub-index also showed a sizeable 5.9% decline. Despite the weakening, both of sub-indexes remain comfortably above their long run average levels suggesting the economy is still a support for sentiment overall.

Consumer views on family finances also recorded a poor start to the year. The ‘finances vs a year ago’ sub-index posted a sharp 5.9% decline taking it back to near 2018 lows. The sub-index tracking expectations for ‘finances, next 12 months’ recorded a milder 3.1% fall. Pressure on family finances remains a key weak spot for sentiment with both sub-indexes well below long run average levels. Slow wages growth and falling house prices remain significant headwinds.

Consumer attitudes towards major purchases were more resilient, the ‘time to buy a major household item’ subindex dipping just 1.3%. However, this sub-index remains below average with the weak reads around family finances pointing to a continuation of the sluggish consumer spending growth seen through 2018.

Note that both the headline Index and its components are seasonally adjusted to remove a regular positive impact on confidence from the holiday season. Other Indexes in the survey are not adjusted and hence should be treated with some caution.

Labour market conditions still look to be supporting consumer confidence, although unemployment expectations – a proxy for consumers’ sense of job security – softened a little in January. The Westpac-Melbourne Institute Unemployment Expectations Index rose 2.2% following a small 0.5% rise in December (recall that higher reads mean more consumers expect unemployment to rise in the year ahead). At 123.6 the index points to job loss fears well below historical averages (the long run average read is 130). The shift in recent months suggests some of the strong momentum evident in labour markets through much of last year is easing.

Sentiment around housing showed mixed moves with views on ‘time to buy’ improving but price expectations again moving lower.

The ‘time to buy a dwelling’ index rose 4.1% in January to be up 7.7%yr. At 114.8 the index nationally is at a four year high but still below its long run average of 120. The state detail continues to show a clear improvement in buyer sentiment in Sydney and Melbourne from the very weak reads in 2017. This suggests the more substantive price declines in these markets has seen some easing in what were acute affordability pressures 12-18 months ago. Ordinarily, the lift in buyer sentiment would be pointing to a lift in owner occupier demand. However, the tightening in lending standards evident over the last year may mean prospective buyers find it more difficult to secure finance.

The Westpac-Melbourne Institute Index of House Price Expectations fell 4.1% to 95.9 in January, marking a new cycle low and the weakest read since we began compiling this index in May 2009. Weakness remains heavily concentrated in NSW and Vic with state index reads of 76 and 83 respectively. Price declines are becoming firmly entrenched in expectations in these states with nearly three quarters of NSW and Vic consumers expecting prices to be unchanged or lower by this time next year. This may also delay any demand feed through from the improvement in buyer sentiment as those looking to buy will be prepared to take their time in order to get ‘better’, i.e. lower, prices.

The Reserve Bank Board next meets on February 5 with the Bank also due to release updated forecasts in its February Statement on Monetary Policy on February 8. The weakening in consumer sentiment will be unsettling for the RBA given its concerns about downside risks to the outlook for consumer spending. With the disappointing September quarter national accounts update materially lowering the starting point for growth and consumer momentum looking softer, the Bank is likely to lower both its 2018 and 2019 growth forecasts from the ‘strongly above trend’ 3.5% and 3.25% forecast it published in November. We expect this tempered view on growth to also temper the Bank’s attitude towards rates. Westpac continues to expect rates to remain on hold in 2019 and 2020.

Note that house price expectations have fallen to their lowest level on record (since May 2009), driven by particularly weak readings in NSW and VIC.

MB maintains the view that the next move in interest rates will be down, with rates possibly falling in 2019.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.