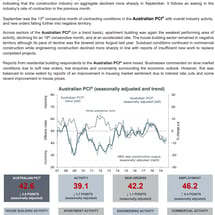

Australian Treasury: compulsory superannuation increase will lower wage growth

Treasury analysis, obtained under Freedom of Information, claims that raising Australia’s superannuation guarantee (‘compulsory superannuation) to 12% would lower wage growth and would make the gender retirement savings imbalance even worse: Though compulsory SG contributions are paid for by employers, wage settings generally takes into account all labour costs.