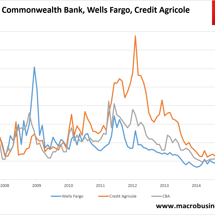

Sell side previews bank results

From Deutsche: Expecting sound UL earnings growth offset by bad debt deterioration Overall we expect a mixed 1H16 reporting season, with hoh cash NPAT growth of ~1% -4%. Underlying earnings growth is likely to be solid (3-8%), however we forecast BDD/GLA ratios to rise ~4bps on avg (due to single name exposures and resources).