From S&P:

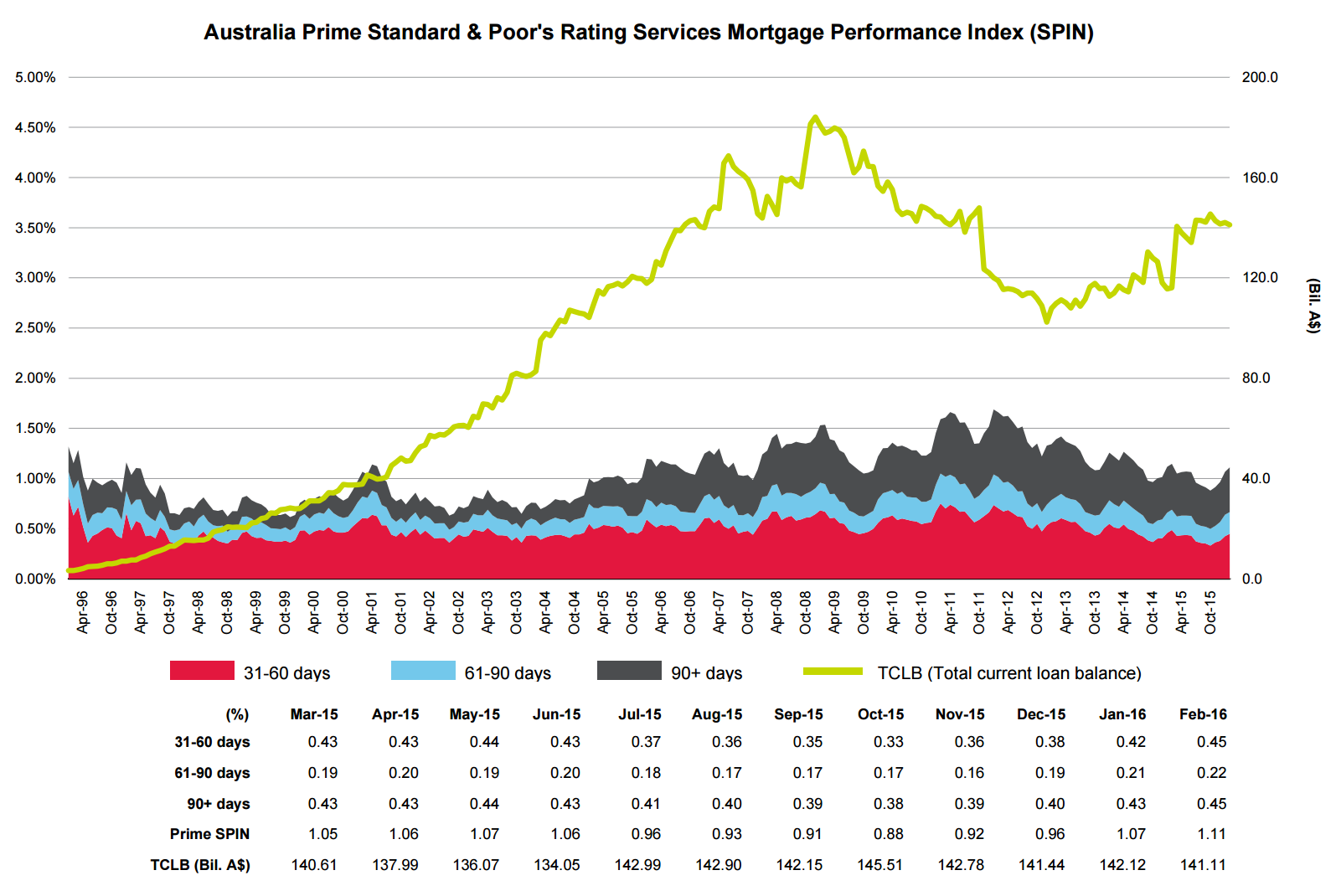

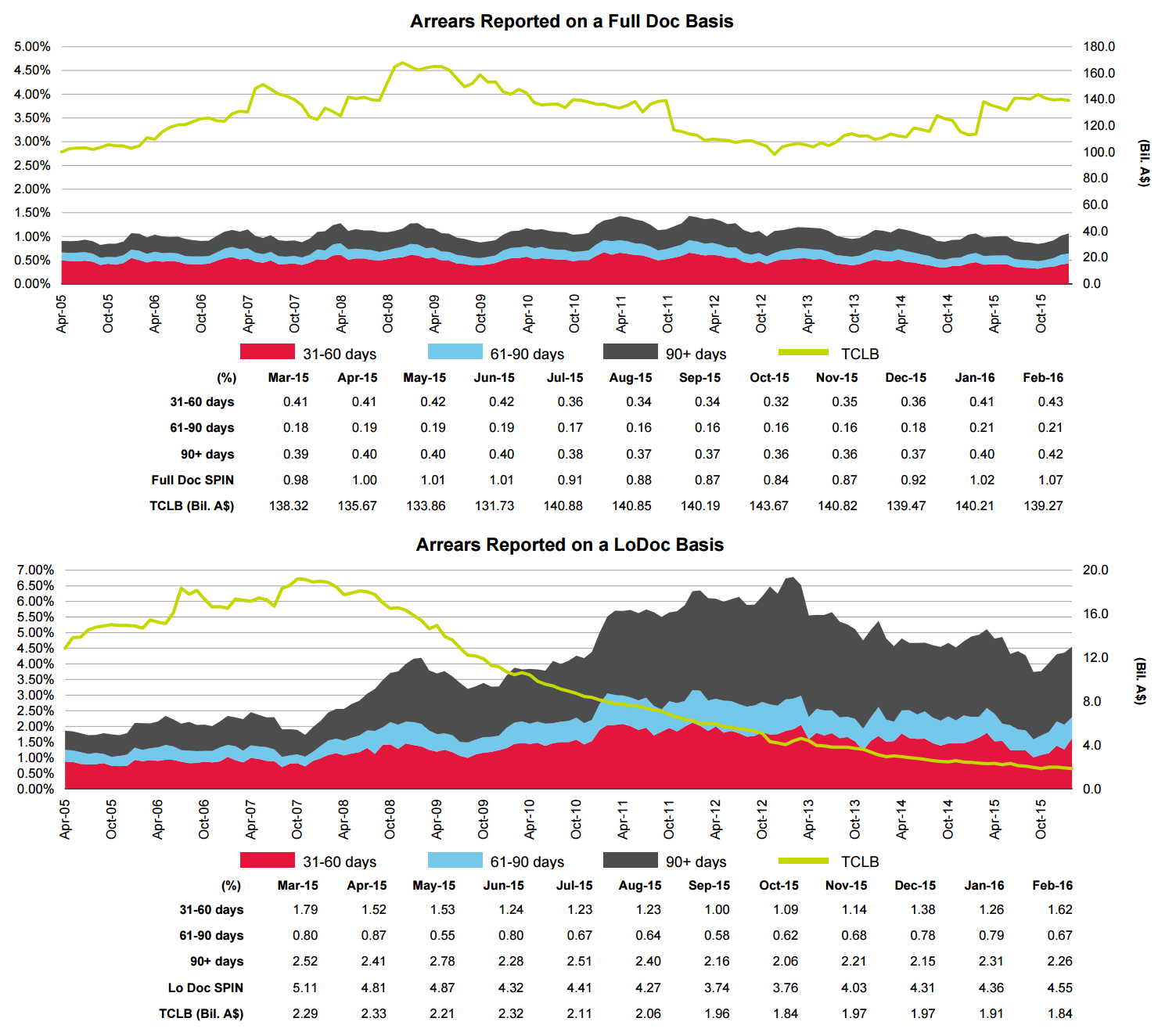

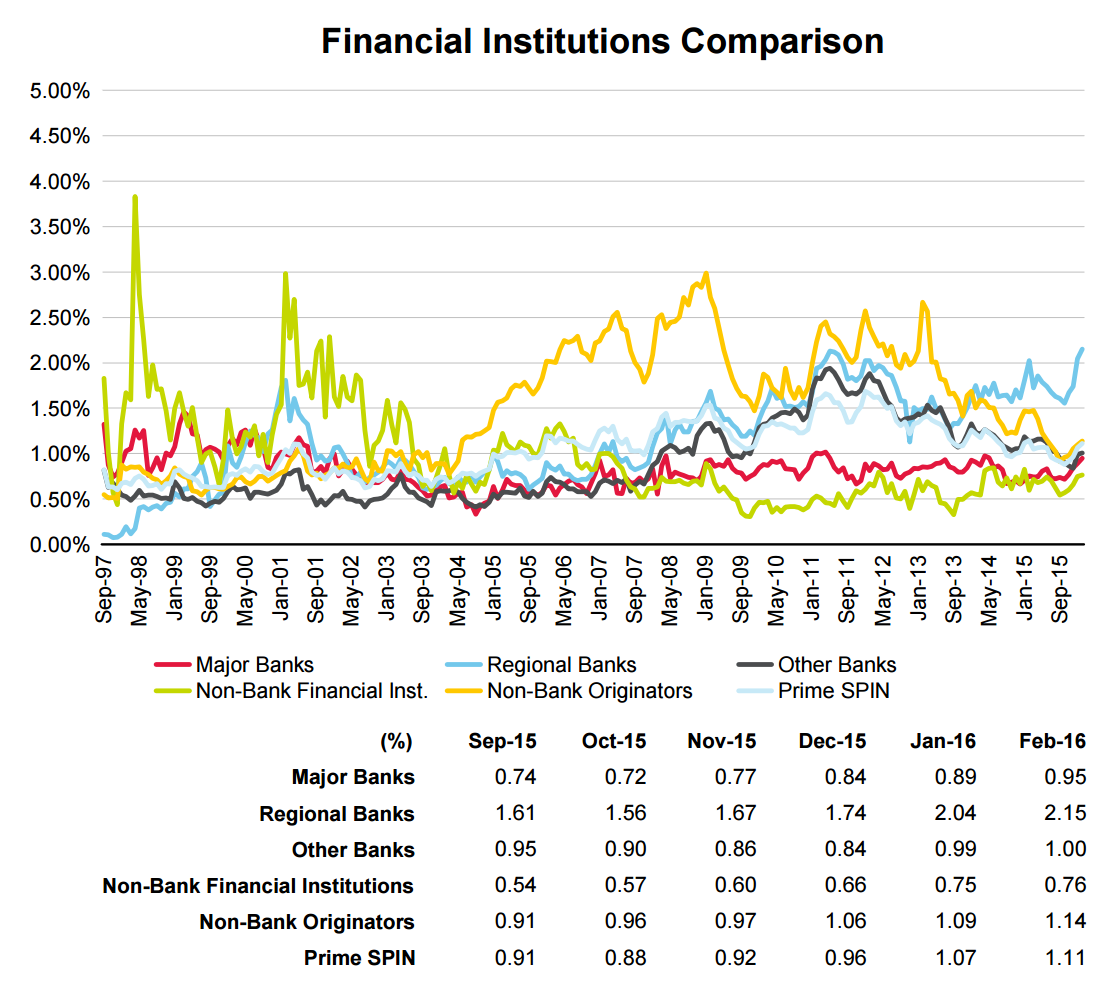

Australian housing loans in arrears rose in February for the fourth consecutive month for prime and nonconforming residential mortgage-backed securities (RMBS), as measured by Standard & Poor’s Performance Index (SPIN). About 1.11% of prime RMBS were in arrears as of Feb. 29, up from 1.07% in January, according to Standard & Poor’s Ratings Services’ recently published “RMBS Arrears Statistics: Australia” report. Full-documentation and low-documentation arrears increased to 1.07% and 4.55%, respectively. Nonconforming RMBS loans in arrears rose to 5.22% from 4.91% a month earlier. While some of the increase reflects a decline in outstanding loan balances, there is also a seasonal component at play; arrears typically increase in January and February, reflecting the effects of Christmas spending, holidays, and January sale periods. The rise in mortgage delinquencies was consistent across originator types. Regional banks recorded the highest arrears of all originator types, reaching 2.15% in February, up from 2.04% a month earlier. The nonbank financial institutions meanwhile recorded the lowest arrears of all originator types, at 0.76%, up from 0.75% in January. We expect arrears to modestly increase in the coming months, in keeping with seasonal patterns.

It’s a bit more than seasonality. The declining trend in force for four years looks in jeopardy of reversal:

Indeed regional banks have a ripping uptrend (capturing the mining bust) and the major’s appear about to follow suit:

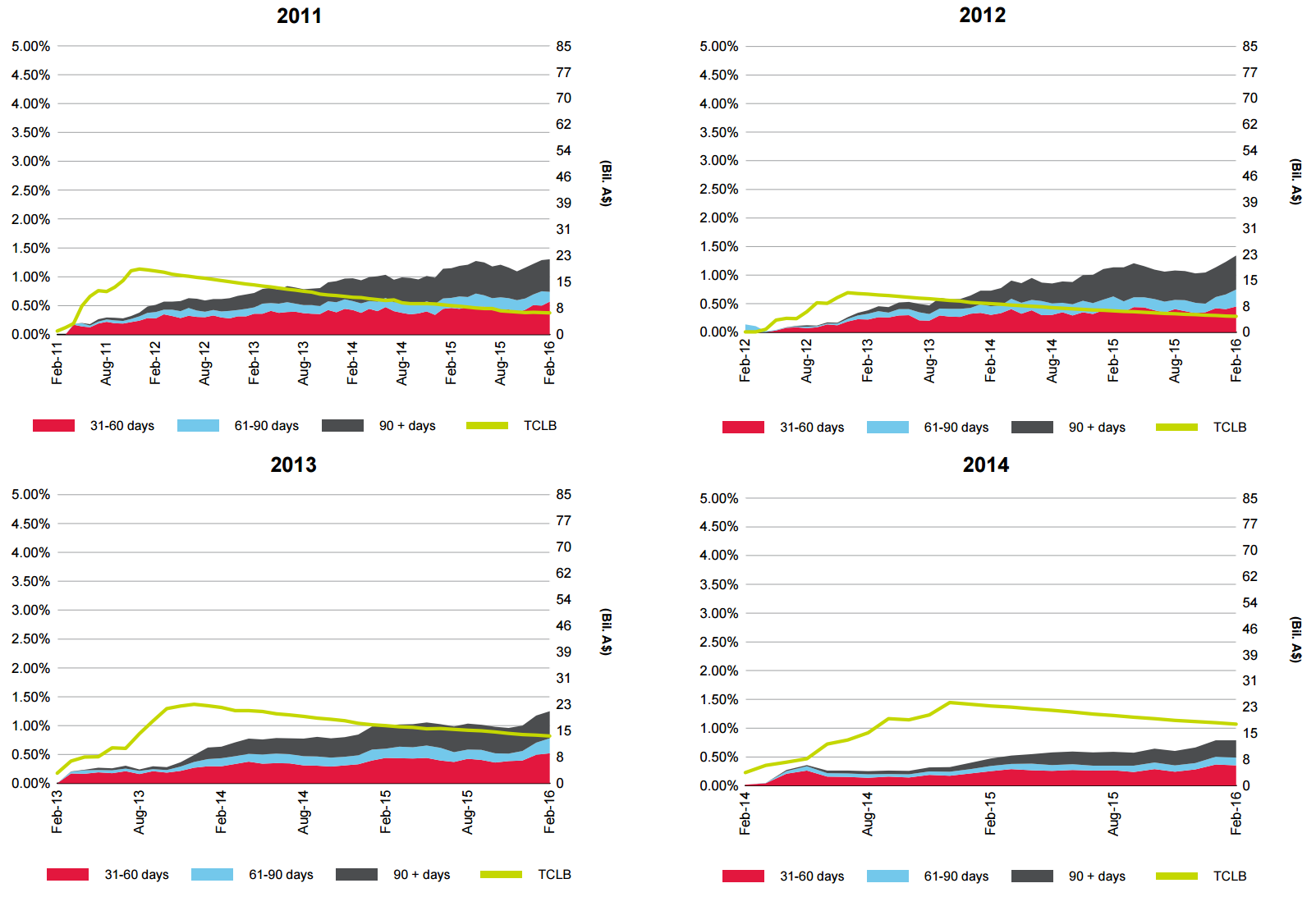

In terms of vintages, as for Moody’s, the dumb bubble is showing early signs of stress:

Yes, seasonality and loan balances are playing their part but the cycle also appears on the verge of a turn.