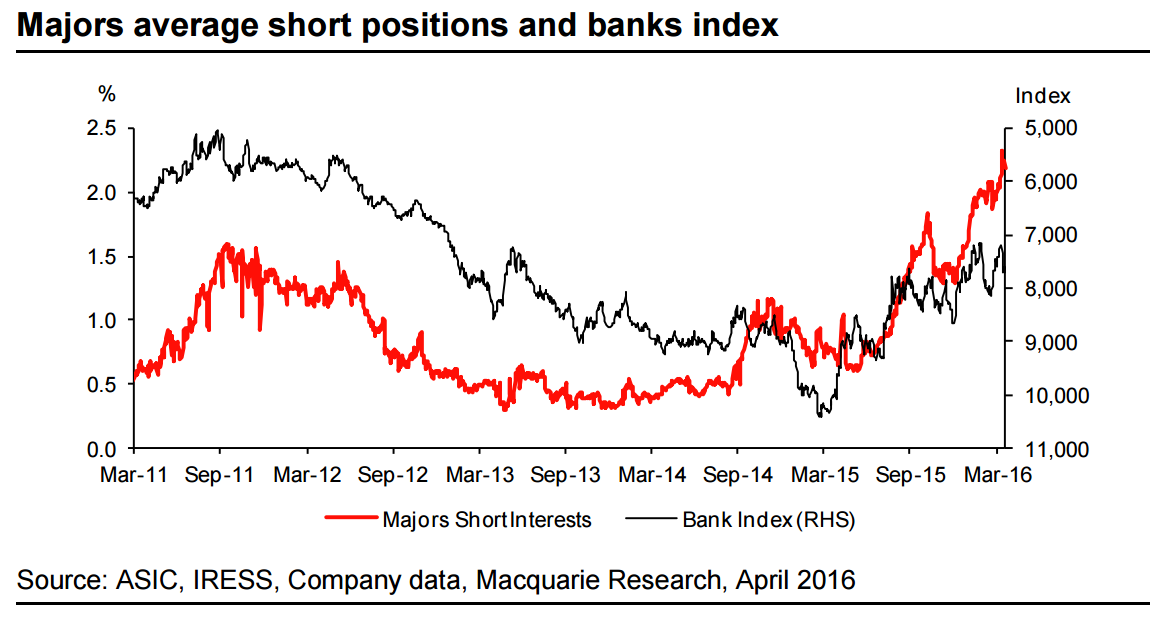

Short positions in the banks are currently at their highest levels since 2011. Broader macroeconomic and regulatory concerns coupled with rising impairment charges have resulted in a ~10% decline in bank share-prices and ~50% rise in short positions since the beginning of this year. Within the majors, ANZ and WBC have the higher level of short positions, while BEN’s short positions are the highest across the banking sector.

Should the upcoming results and outlook commentary exceed current relatively bearish expectations, bank share-prices could rebound. We see fundamental value in the sector at current levels and see upside risk in the upcoming banks results relative to perceived negative market sentiment. Further, we believe there is near-term upside risk from additional mortgage repricing after the July 2016 Federal elections. Majors average short positions and banks index Source: ASIC, IRESS, Company data, Macquarie Research, April 2016

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.