Categories

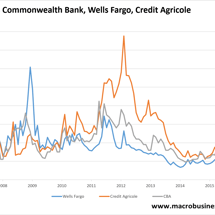

Australian banks

Big Iron firms again

Dalian is roughly flat today after overnight gains: Big Iron is modestly up too though FMG’s possible double top still lurks: Big Gas is rebounding after OPEC minister comments supported oil: Big Gold is off.

David Llewellyn-Smith

9 years ago

3

Bank Royal Commission back on political radar [Updated]

By Leith van Onselen After narrowly holding-off a banking Royal Commission in September, it is back on the political radar with Coalition MP George Christensen pledging to support Bob Katter’s banking Royal Commission bill.

Leith van Onselen

9 years ago

9

CBA sends shockwave through specufestor lending market

By Leith van Onselen A day after its subsidiary, Bankwest, slammed the brakes on property investment lending for new customers, its parent, the CBA, has done likewise.

Leith van Onselen

9 years ago

41

The Australian mortgage ponzi keystone cracks

The keystone in the great Australian mortgage ponzi, Genworth LMI, reported today and it wasn’t terribly encouraging: All of that is serious matter of perspective.

David Llewellyn-Smith

9 years ago

29

Gold goes boom!

Dalian is open and up a few points: Big Iron is still down with BHP -0.6%, RIO -02% and FMG -1.4%, it’s monster double-top firming a little: Big Gas is off again: Big Gold is going boom!

David Llewellyn-Smith

9 years ago

2

Bankwest pulls specufestor handbrake

Via the AFR: Bankwest, a subsidiary of Commonwealth Bank of Australia, has slammed the brakes on property investment lending for new customers.

David Llewellyn-Smith

9 years ago

27

Fortescue’s monster double top

Dalian is roughly flat during the day: Big Iron is too: FMG has formed what could be a monster double top though it needs to fall through $5.80 to confirm it: Big Gas is off on Macquarie’s downgrade: Big Gold is in heaven again!

David Llewellyn-Smith

9 years ago

More mortgage rate hikes

Via the AFR: Lenders are blaming rising wholesale and regulatory costs for a new round of increases in fixed and variable products by up to 60 basis points.

David Llewellyn-Smith

9 years ago

30

Is Dodd-Frank a goner?

David Llewellyn-Smith

9 years ago

3

China reopens, Dalian limit down

China is open again today and Dalian has returned limit down -6%.

David Llewellyn-Smith

9 years ago

NAB drops lending standards as APRA snores

Snooooooooooooooore: National Australia Bank is turning up the heat on rivals by making it easier for property borrowers to qualify for home loans amid concerns that red-hot property markets are beginning to boil.

David Llewellyn-Smith

9 years ago

8

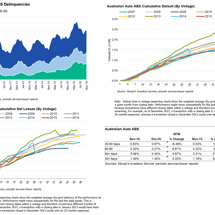

Yep, mortgage arrears are going higher

Moody’s is out today with its arrears data for November last year and we’re going higher.

David Llewellyn-Smith

9 years ago

7

Macquarie: Banks specufestor binge “unsustainable”

From Macquarie today: Elevated housing growth will become tougher to maintain Balance sheet growth continued to gain momentum at the end of 2016, largely underpinned by ongoing strength in investor housing volumes. Investor lending growth is currently tracking at ~9% (3m ann.) and approaching APRA’s 10% growth cap.

David Llewellyn-Smith

9 years ago

12

Have banks juked the stats on investor lending?

Leith van Onselen

9 years ago

8

APRA the stupid gives specufestors a sniff

David Llewellyn-Smith

9 years ago

8

Mortgage arrears continue building

From S&P: The number of delinquent housing loans underlying Australian prime residential mortgage-backed securities fell in November 2016 from the previous month, according to a recent report by S&P Global Ratings.

David Llewellyn-Smith

9 years ago

Why won’t the RBA kill the CLF?

Leith van Onselen

9 years ago

27

Fitch puts banks on negative ratings watch, APRA ignores risks

Via Forex Live: From the Fitch Outlook report for the Australian banking sector.

Leith van Onselen

9 years ago

17

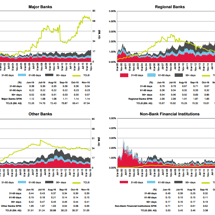

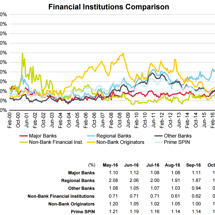

Banks to the moon?

I’ve long railed against the fact that the financials index (less property trusts), the XXJ, makes up over half the ASX200, with the big four banks holding over 30% by total weight.

Chris Becker

9 years ago

22

Iron ore shakeout gathers pace

It’s awn with Dalian grinding another 2% lower today triggering decent falls in Big Iron: FMG and WHC both looking very toppy.

David Llewellyn-Smith

9 years ago

A little EM capital flight arrives Downunder

We all know that Australia is secretly an emerging market (EM), characterised as it is by dodgy governance, a resources curse, rent-seeking, asset bubbles and weak external accounts.

David Llewellyn-Smith

9 years ago

5

Stocks dodge the building China bond syndrome

Chinese bonds are bid a little today: And Dalian is flat: Under the surface, trouble still lurks, via Bloomie: Here’s another Chinese financial practice that’s prompting high-decibel warnings.

David Llewellyn-Smith

9 years ago

2

Big Iron sees light of hope in rising Chinese bond-fire

The Chinese bond-fire is rising again today and it is clearly a mini-crisis that could develop swiftly: Dalian is working it out: But not Big Iron.

David Llewellyn-Smith

9 years ago

4

Dirt dumped, banks bought

David Llewellyn-Smith

9 years ago

Mortgage arrears up again

From the cowardly S&P: The number of delinquent housing loans underlying Australian prime residential mortgage-backed securities increased in October from the previous month, according to a recent report by S&P Global Ratings.

David Llewellyn-Smith

9 years ago

10

Newer Articles

Older Articles

Page

69

of

109

Newer Articles

Older Articles

Advertisement