The Australian mortgage ponzi keystone cracks

The keystone in the great Australian mortgage ponzi, Genworth LMI, reported today and it wasn’t terribly encouraging:

All of that is serious matter of perspective. Australia’s LMI sector holds the bag for the entire high LVR book of the banking system and when it goes I expect GMA to go back from whence it came, into government ownership.

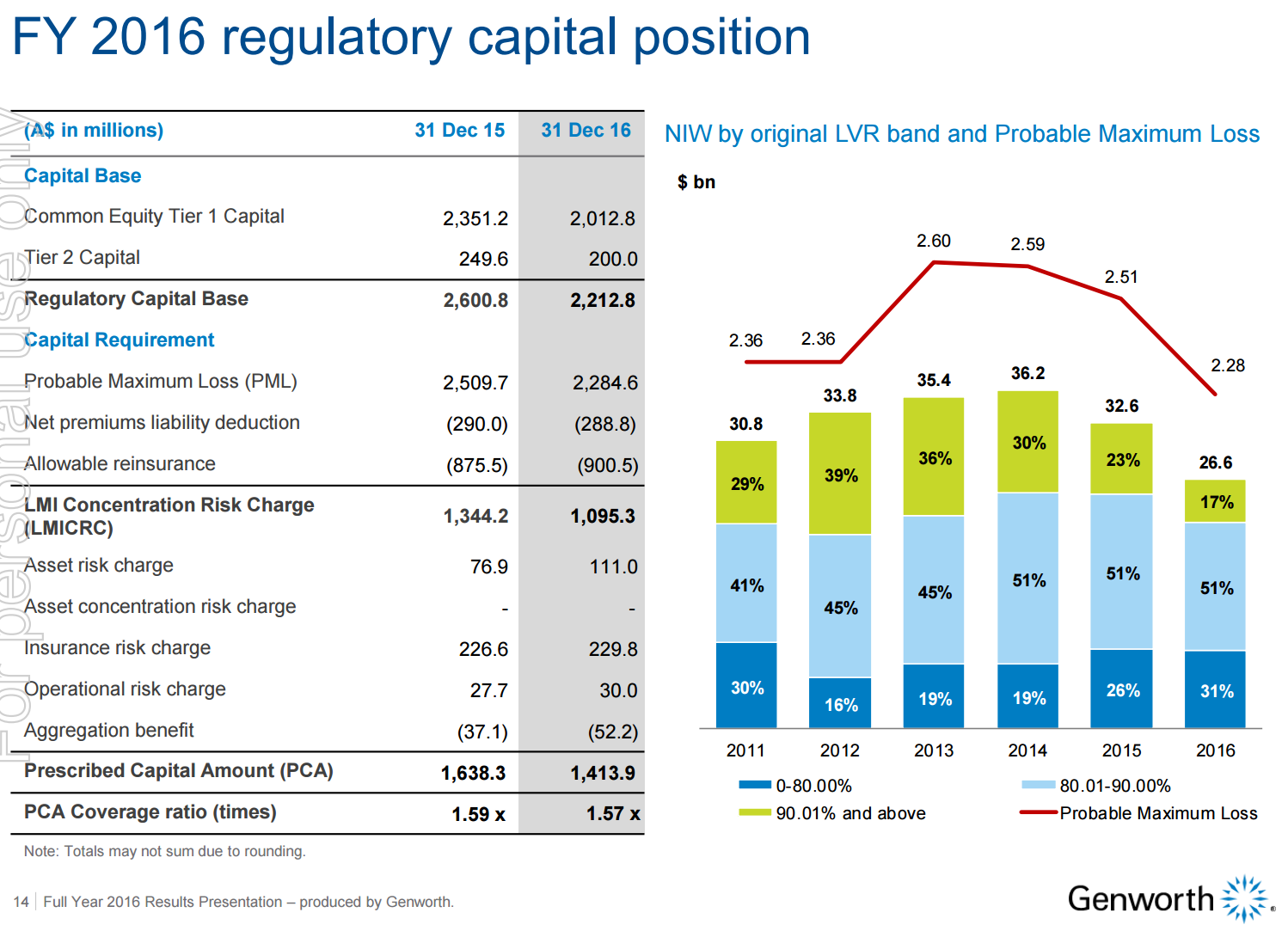

Consider, the so-called strong regulatory position with just $2.2bn of capital, down $400mn over the year

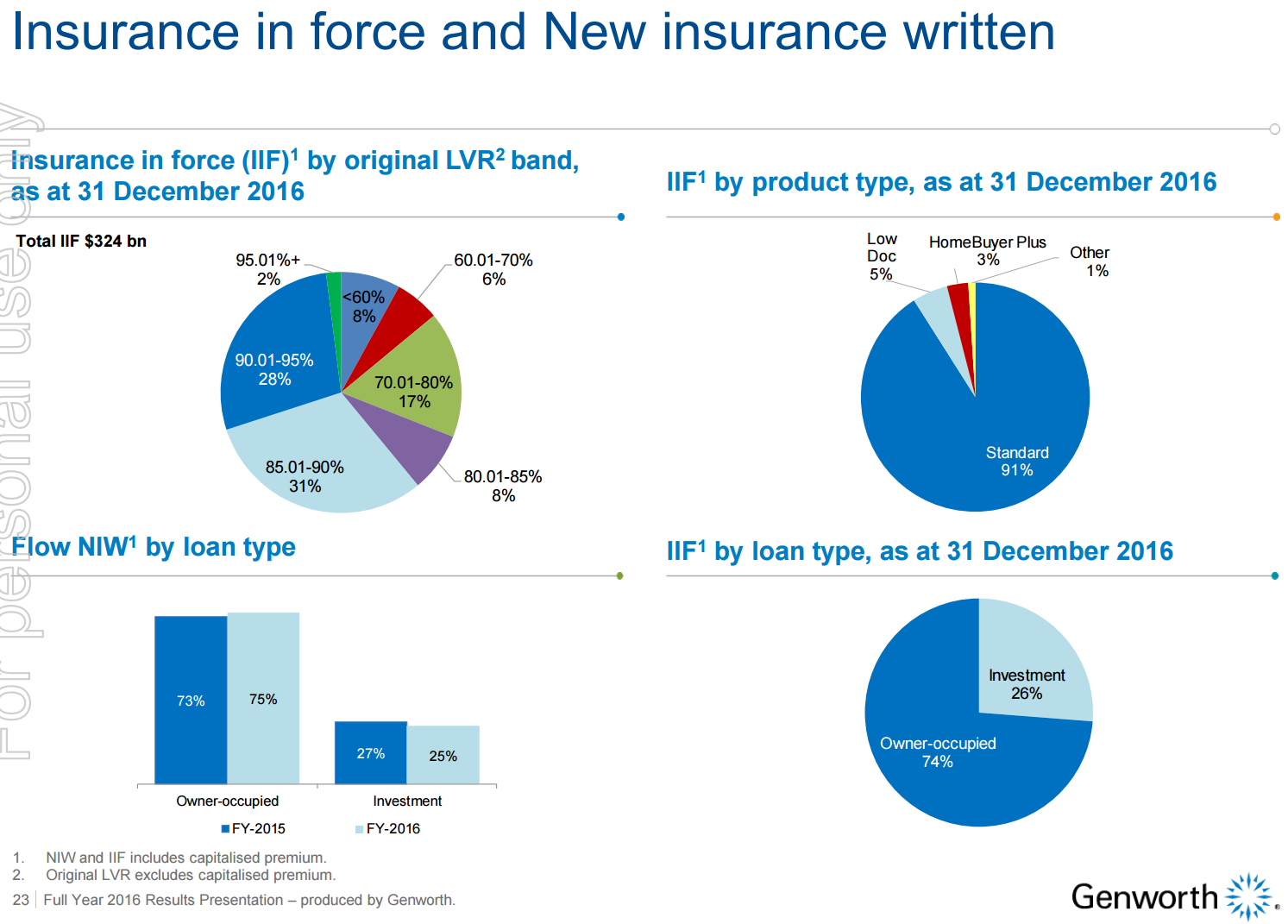

Securing a staggering $324bn in high risk mortgages:

At a leverage of…wait for it…147x…very safe a secure! There is at least $950mn of reinsurance.

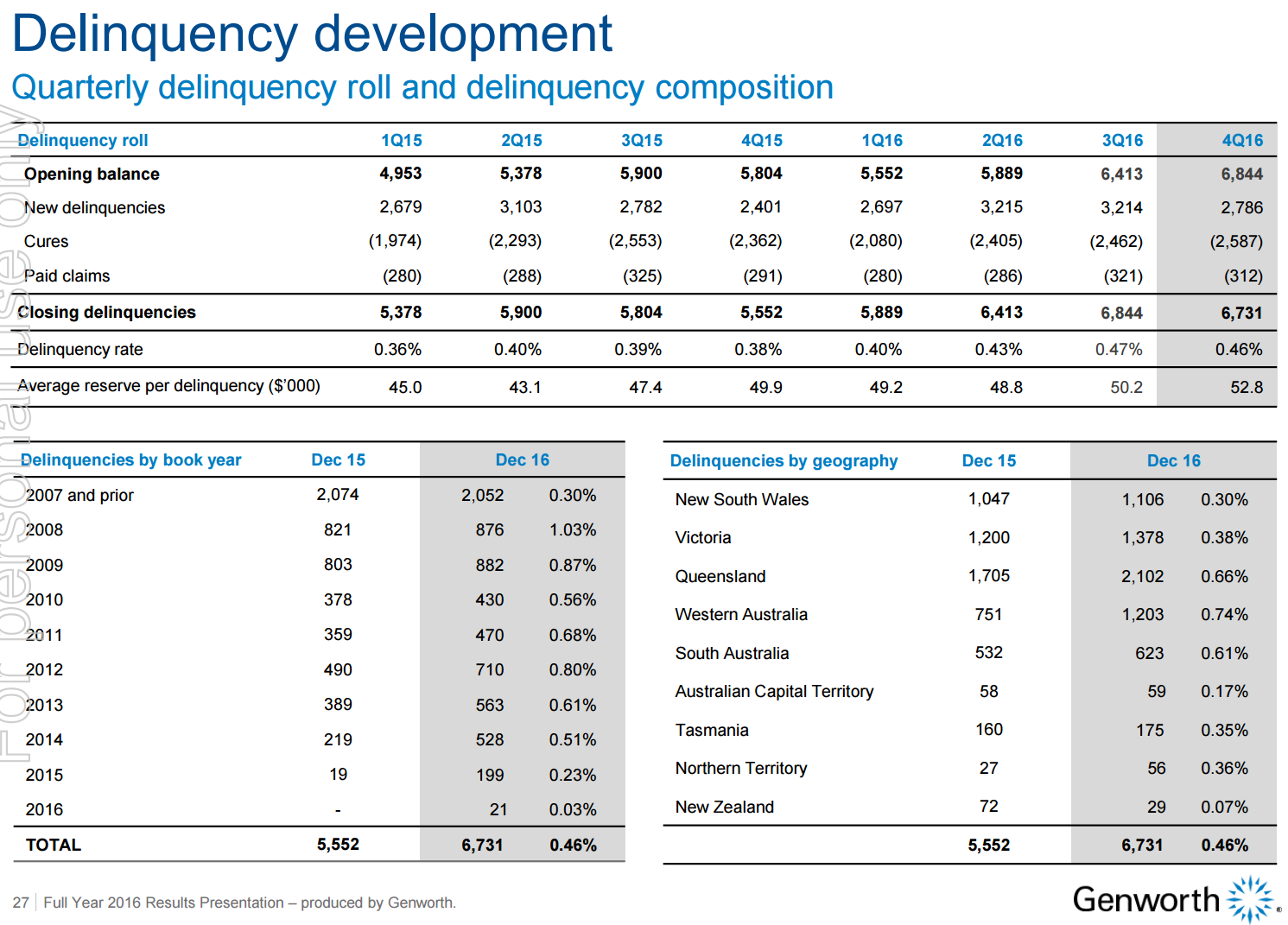

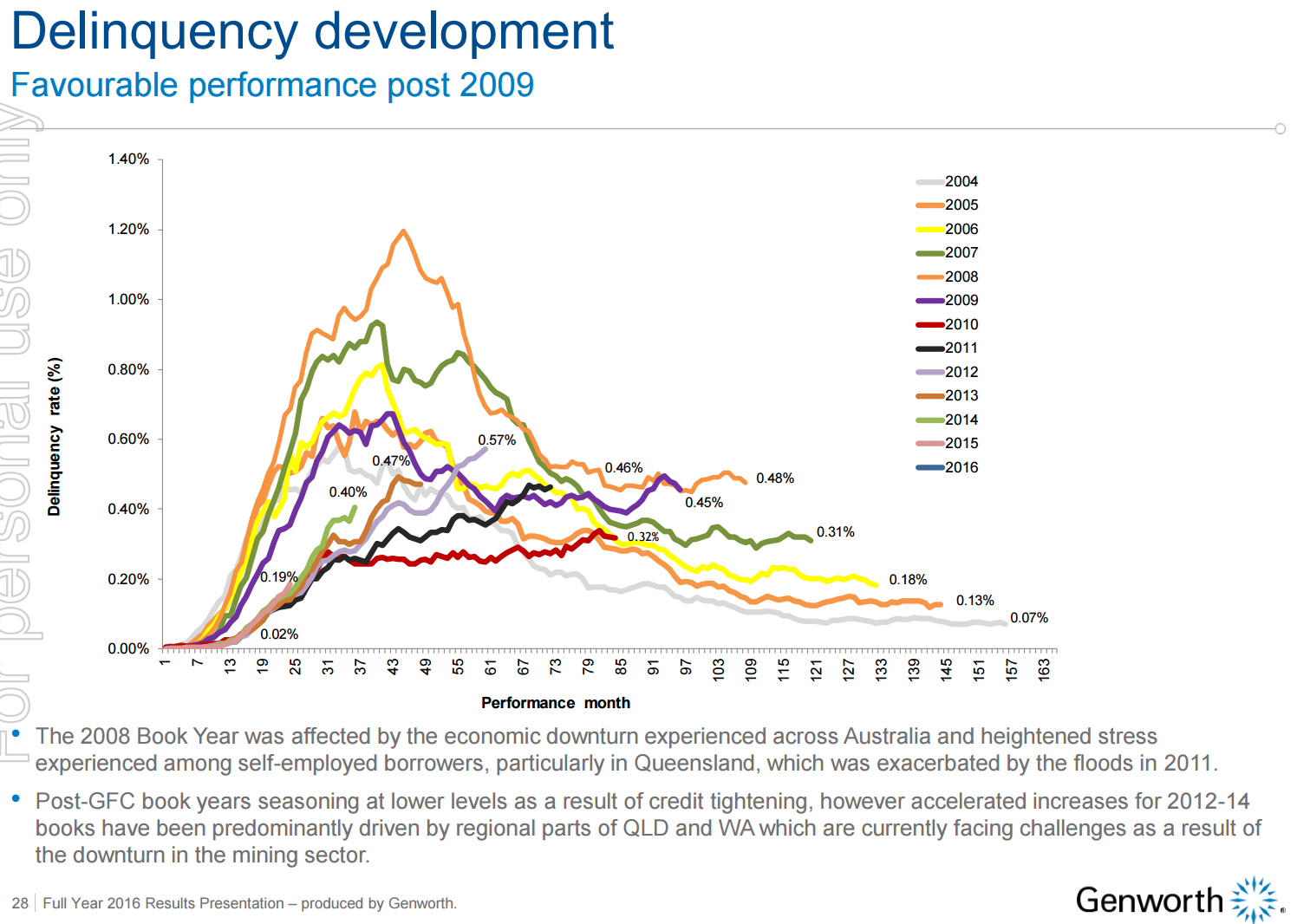

Moreover, losses are beginning to mount:

As the mining boom years of 2012-2015 sour:

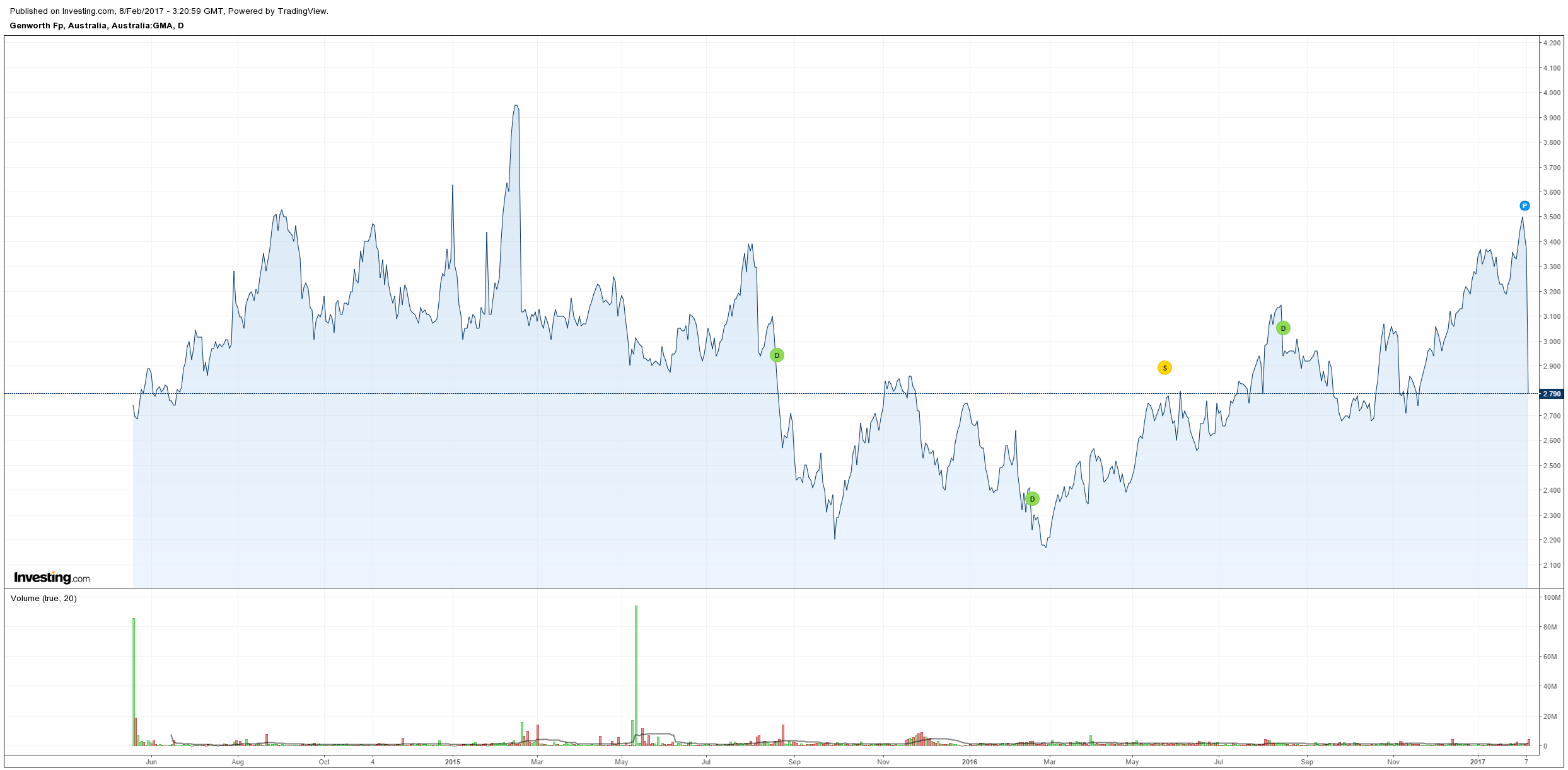

Perversely, GMA has been allowed to run down its capital since floating to support its equity. That was of course very short term thinking by APRA. Still, it has until today kept the ponzi scheme afloat, down -18% today and approaching its float price:

But with capital run down, delinquencies on the rise, and shrinkflation killing new business, where’s the investment case now? Gone.

It’ll probably be OK so long as we keep exhausting every policy arrow to prevent the natural adjustment in property prices from occurring but when that quiver is empty this thing will implode ala American Insurance Group in the GFC.