New Zealand Prime Minister, Jacinda Ardern, was elected in 2017 on a platform of fixing New Zealand’s chronic housing crisis.

However, Ardern’s Labour Party failed dismally on housing in its first term, failing to deliver on key election promises.

Labour’s promised ‘KiwiBuild’ program to build 100,000 public houses descended into a farce, with the government abandoning its building target and instead announcing a bunch of demand-side measures to inflate prices.

Labour also abandoned capital gains tax reforms and back-slid on the promise to abolish Auckland’s urban growth boundary and reform infrastructure financing.

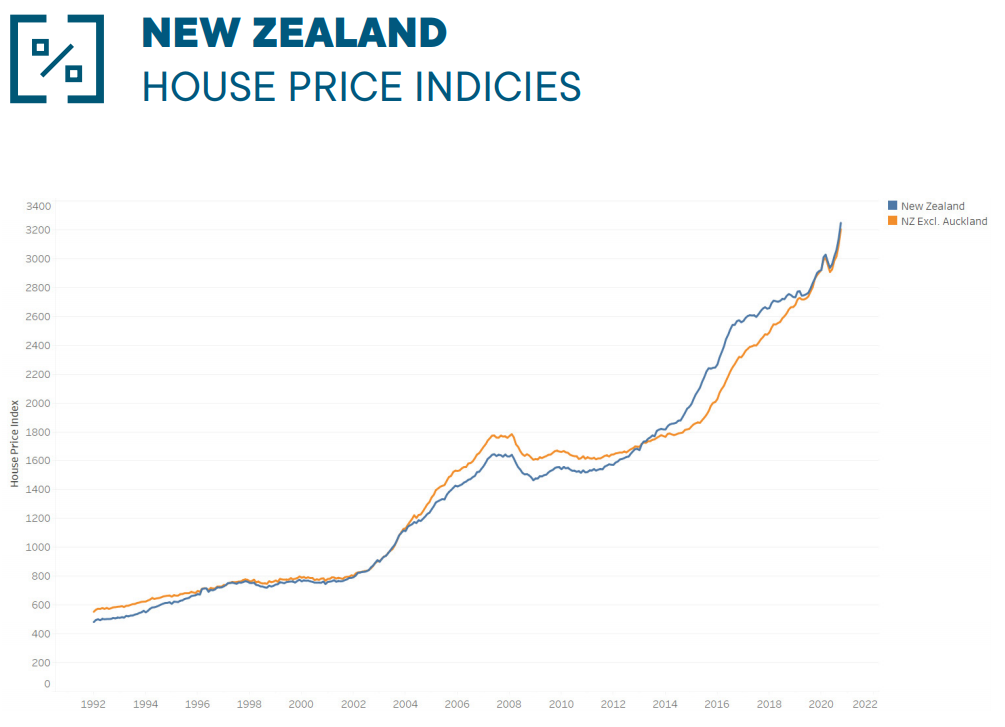

As a result, New Zealand house prices have surged to a fresh record high and home ownership has plunged to a 70-year low:

Over the weekend, a ex-Labour Party MP and cabinet member, Peter Dunne, published a scathing attack on Labour’s housing failures:

The current housing debate has a pathetic sense of déjà vu about it. Before the 2017 election Labour successfully hyped the then housing situation into a crisis and implied it had all the answers if elected to government.

But now, one term of Labour-led government later, the situation is worse than ever. Housing prices have sky-rocketed, nowhere near enough houses are being built, and waiting lists for public housing have soared. And the responsibility for this deteriorating situation apparently lies with everyone else.

Labour still keeps blaming the previous government… The government that alleged it had all the answers before it came to power now seems all at sea, with little idea what to do next. It has long since abandoned its previous flagship Kiwibuild policy as a disaster but has done nothing to replace it. Instead, the Prime Minister now promises to “take advice” which looks increasingly plaintive, and hardly inspires confidence…

The escalating sense of drift is becoming intolerable. The government must move beyond just wanting to take more advice and show some leadership on the issue…

So, it surely makes sense to bring them all together in a National Housing Summit to develop a single, comprehensive, integrated national housing strategy, to which they would all be required to commit to and take ownership of…

If the government really wants to do more than just continue to “take advice” on the issue, convening urgently a National Housing Summit of all the relevant interests to develop a plan for the future would be a very good place to start.

It’s hard to see how a National Housing Summit talk fest will achieve anything but hot air.

The reality is that nothing genuine ever happens on housing policy because “affordable housing” requires prices to fall. And nobody in the government nor home owners or the industry want this to happen. It’s exactly the same in Australia.

So instead we get “affordability” measures like first home buyer grants, which only succeed in artificially inflating demand and prices.

Heck, this morning Jacinda Ardern told The AM Show that the Government would continue “looking for ways to encourage and support first home buyers”, which is code for more demand-side subsidies.

In the lead-up to last month’s election, Jacinda Ardern once again vowed to tackle the nation’s housing crisis.

Don’t expect anything concrete to happen.