The Canberra Times’ Crispin Hull penned an article over the weekend defending Australia’s compulsory superannuation system and imploring the Morrison Government to maintain the scheduled increase in the superannuation guarantee to 12%:

The [superannuation] system needs some changes, but not in the way that big business, Coalition MPs and right-wing think tanks are suggesting. They want to trash the present system and either cut employer contributions or at least not increase them from the present 9.5 per cent of income to 12 per cent over the next three years as is presently legislated…

Most economists and right-wing think tanks absolutely hate the compulsory superannuation contribution from employers. But their arguments against it are dishonest. If they were honest they would say we do not like paying super to employees because we would rather stuff the money into our own pockets.

Rather, they say, employees should not be forced to have 9.5 per cent of their wages put in to super. They should have it now when they need it to help buy a house etc etc. Rubbish. If employers were not forced by law to make that contribution, it would not go into workers’ pockets. The employer would keep as much of it as they could get away with.

And even if employers were saints and if super contributions were cancelled and they paid all of it into the workers’ pay packets, we know the result. The average worker would not put anything in to superannuation. It would all be spent on consumer rubbish today. No one would save for tomorrow. That is what happened before compulsory super and that is what would happen if it were abolished.

The critical thing, though, is to make the tax arrangements on superannuation earnings fairer. With the present flat tax of 15 percent, the vast bulk of the total tax concessions goes to people on higher incomes who would otherwise have their earnings taxed at more than 40 per cent.

High-income people usually have higher balances so gain bigger benefits.

The tax on superannuation earnings should be made progressive, but not based on income, but rather based on the balance of the person’s superannuation account or accounts. Say, zero on balances up to $100,000, 15 per cent up to $750,000, 30 per cent up $1.5 million and 40 per cent thereafter. Or it could be more gradually stepped.

The importance of a progressive rate based on the balance is that it is fairer to people with low balances, especially women who have often been out of the workforce caring for children…

It would be a major injustice to slow, halt or reverse the amounts paid in the compulsory scheme. To halt it at 9 per cent would in effect give retiring workers just enough to disqualify them from the aged pension and little more – not correcting the historic wrong and not providing decent retirement income for all.

There are a number of fatal flaws with Crispin Hulls arguments.

First, his ad hominem claim that the opposition to raising the superannuation guarantee is coming from “right-wing think tanks” is ridiculous.

Advertisement

The Grattan Institute has led the arguments against raising the superannuation guarantee and is about as centrist as you could get.

Left-leaning chief economist of The Australia Institute, Richard Denniss, also last month lambasted Australia’s compulsory superannuation system, claiming it is “stealing from the poor to give to the rich” and labelled the system “unfair, unaffordable and inefficient”.

Whereas left-leaning economist and author of Game-of-Mates, Dr Cameron Murray, last month called for the entire compulsory superannuation system to be disbanded because of its extraordinary waste.

Advertisement

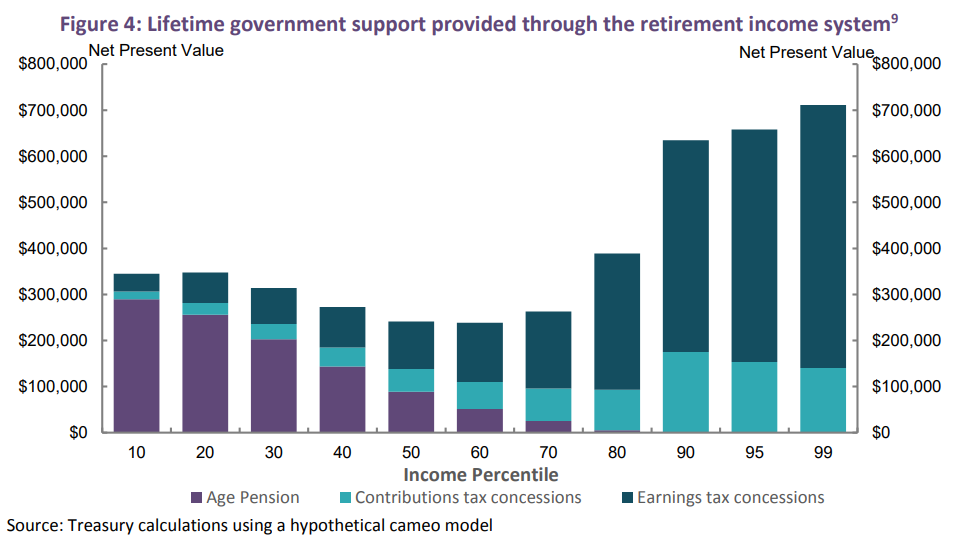

Second, Crispin Hull admits that Australia’s compulsory superannuation system is inequitable because “with the present flat tax of 15 percent, the vast bulk of the total tax concessions goes to people on higher incomes”.

This claim is unambiguously correct and confirmed last month by the Australian Treasury:

Advertisement

Hull also recommends some sensible reforms to make concessions more progressive.

But here’s the rub: reforms to make superannuation concessions progressive should be made before even considering raising the superannuation guarantee.

Because lifting the superannuation guarantee without first fixing the underlying problems would only accentuate the existing inequities, making the system even less efficient and more wasteful.

Advertisement

Australia’s superannuation concessions must first be calibrated correctly before compelling workers to contribute even more into the system. Indeed, “it would be a major injustice” to do otherwise.

Finally, Crispin Hull’s suggestion that the superannuation guarantee is paid for by employers, not workers via lower take-home wages, is unambiguously false.

Employers only care about their overall wage cost and don’t care what proportion of their wage bill is paid directly to workers or into a superannuation account. The cost to them is the same regardless.

Advertisement

Thus, freezing the superannuation guarantee at 9.5% rather than 12% necessarily means that workers would receive more in take-home wages.

This wage trade-off is non-controversial and was confirmed by the Henry Tax Review, which also recommended freezing the superannuation guarantee:

Although employers are required to make superannuation guarantee contributions, employees bear the cost of these contributions through lower wage growth. This means the increase in the employee’s retirement income is achieved by reducing their standard of living before retirement…

The retirement income report recommended that the superannuation guarantee rate remain at 9 per cent. In coming to this recommendation the Review took into the account the effect that the superannuation guarantee has on the pre-retirement income of low-income earners.

Even slower wage growth will be the result of increasing compulsory superannuation contributions from 9.5 per cent to 12 per cent…

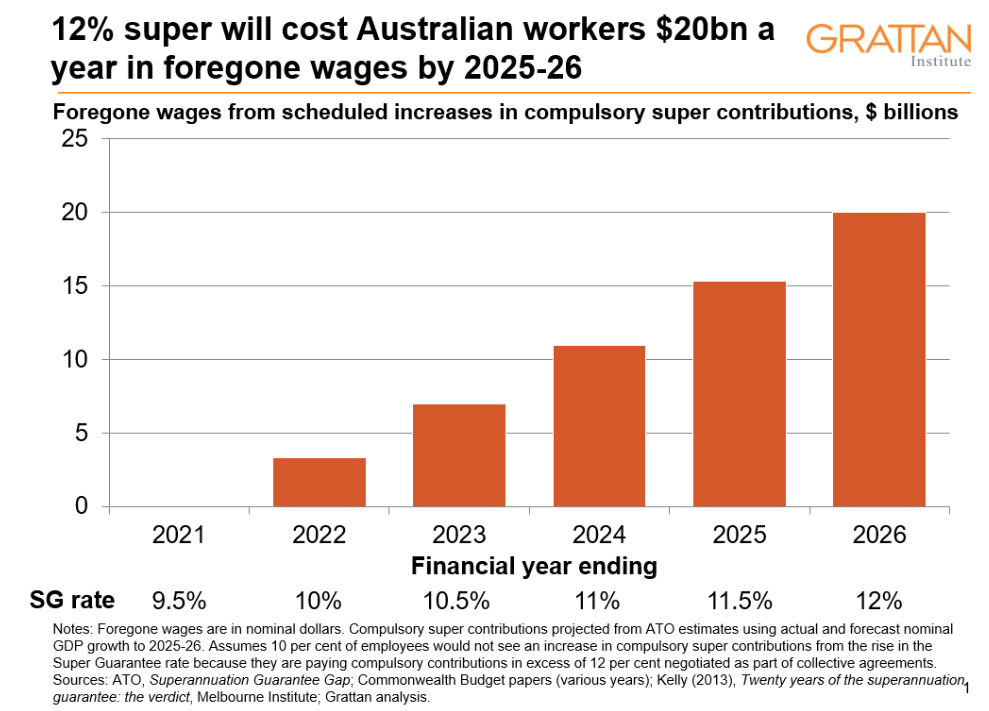

If compulsory super contributions go up, wages will be lower than they would otherwise. And the cut to wages from raising compulsory super is big. Really big. By the time it’s fully implemented in 2025-26, a 12 per cent Super Guarantee will strip up to $20 billion from workers’ wages each year, or nearly 1 per cent of GDP..

The increase in the superannuation guarantee to 12 per cent will likely lead to lower wage increases, shifting a greater proportion of earnings into the superannuation system.

A major challenge for retirement incomes policy is the need for current consumption to be deferred in favour of future income in retirement…

No loss of remuneration is involved in meeting this national challenge. What is involved, rather, is forgoing a faster increase in real take‑home pay in return for a higher standard of living in retirement.

Because it’s wages, not profits, that will fund super increases in the next few years. Wages are the seedbed of the whole operation. An increase in super is not, absolutely not, a tax on business. Essentially, both employers and employees would consider the Superannuation Guarantee increases to be a different way of receiving a wage increase.

The cost of superannuation was never borne by employers. It was absorbed into the overall wage cost. Indeed, in each year of the SGC growth between 1992 and 2002, the profit share in the economy rose…

In other words, had employers not paid nine percentage points of wages as superannuation contributions to employee superannuation accounts, they would have paid it in cash as wages…

Again, raising the superannuation guarantee without first fixing the underlying problems would heighten the system’s inequities. It would rob lower-income workers of much-needed disposable income, worsen inequality (due to the concession system favouring high-income earners), and would rob the federal budget of revenue (via forgone income tax receipts).

Raising the superannuation guarantee is unambiguously poor policy and focus should instead be placed into making sure the system works equitably and efficiently.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.