Just a week after The Australia Institute (TAI) released a report – funded by Industry Super Australia – backing an increase in the superannuation guarantee (compulsory superannuation) to 12%, the chief economist of TAI, Richard Denniss, has blasted Australia’s superannuation system for “stealing from the poor to give to the rich”:

Welcome to the topsy-turvy land of superannuation, in which taxpayers give the most assistance to those who need it least, and no assistance to those who need it most…

Much is made of the enormous size of Australia’s $2.9tn pool of superannuation savings, but we talk much less about the fact that the only reason it grew so big was that we literally force the vast majority of employees to spend 9.5% of their income buying superannuation every week. Let’s be clear: if we forced all Australians to get a massage every week or buy a new Australian car every year, we would have an enormous massage and car industry as well.

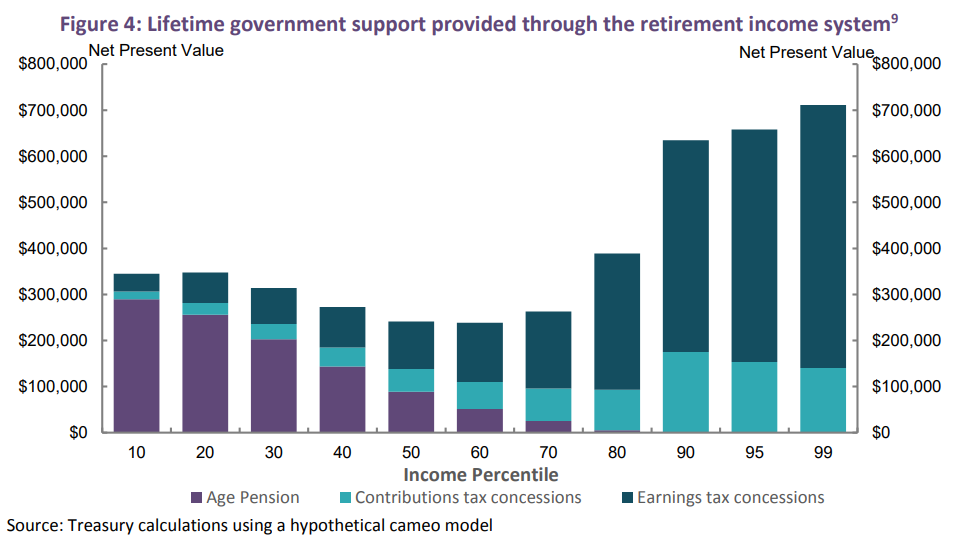

For more than 10 years, I’ve been trying to explain just how unfair, unaffordable and inefficient the Australian superannuation system has become, but you don’t just have to take my word for it any more. The commonwealth Treasury recently concluded that “modelling suggests that over a lifetime, more public support may be provided to those in higher income brackets”…

In Australia, taxpayers contribute 10 times as much money to the superannuation accounts of the people in the richest 1% than they contribute to the people in the poorest 10% of workers.

Put another way, the graph below also shows that, over the course of their lives, those Australians lucky enough to be in the top 1% of income earners will receive over $700,000 in taxpayer contributions to their personal superannuation account, while those in the bottom 10% will receive less than $50,000.

…we hand out $43bn a year in tax concessions for super. It’s obscene and it only survives because the superannuation industry is so skilful at confusing people, boring people, or both…

Put simply, when it comes to our super funds, we tax the earnings of those with millions at far less than their marginal tax rate and we tax the earnings of those with small balances at far more than their marginal tax rate. Tax concessions for superannuation literally amplify inequality in Australia…

It would be easy to cap the generosity of tax concessions to those with the most and boost support for those with the least. We do it with the age pension and we could do it with super, if we wanted to.

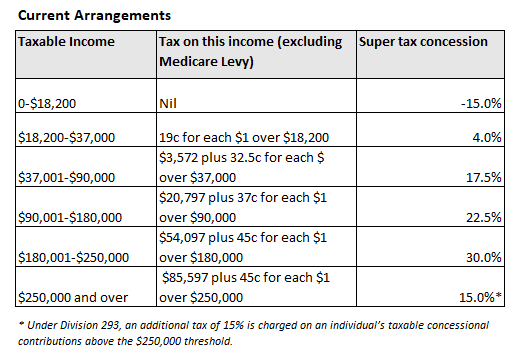

Indeed, one of the biggest knocks on Australia’s compulsory superannuation system is that because of Australia’s flat 15% tax on contributions, those on lower incomes receive minimal concessions (or are penalised), whereas those on higher incomes receive the biggest tax concessions on contributions:

Advertisement

Division 293 remedies the situation for those very high income earners above $250,000. But even then, the lion’s share of superannuation concessions still flow to the highest income earners, whereas the lower income earners continue to be disadvantaged by the system, as illustrated clearly in Figure 4 above.

An obvious solution to improve both equity and Budget sustainability would be to abandon raising the compulsory superannuation guarantee and instead replace the 15% flat tax on contributions/earnings with a flat-rate refundable tax offset (e.g. 15%). This way, everyone that contributes to superannuation would receive the same tax concession, the system would be made progressive, and lower income earners would get a better deal.

It’s a no-brainer.

Advertisement

So why did TAI last week release a report funded by Industry Super Australia arguing to lift the superannuation guarantee when there are clearly fundamental problems with the system? Lifting the superannuation guarantee would merely amplify these inequalities and inefficiencies.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.